On My Radar: I Hear The Train A-Coming

April 24, 2026

By Steve Blumenthal

“I hear the train a-comin', it's rolling 'round the bend, And I ain't seen the sunshine since I don't know when…”

— Johnny Cash, Folsom Prison Blues

Cash wrote that song in the early 1950s. “Stuck in Folsom city,” the train wasn’t something you could see; it was something you hear, it was something you feel. A distant rumble. A warning.

Motivated by a note this week from a friend/client in the agriculture business (think real-time boots on the ground):

“We’re seeing supply chain stress in real time, and it’s getting worse.

Fertilizer deliveries are running weeks behind. We’re about 140 truckloads short and receiving only a fraction of what we need each day. Farmers are being forced to adjust planting plans on the fly.

To give you a sense of how tight things are, we rented a truck and drove across four states to pick up product ordered months ago. Days later, the supplier asked to buy it back at a premium. That’s how scarce supply has become.

Prices are moving fast: fertilizer up roughly 60% since last fall, fuel up nearly 50% in just a few weeks, with chemicals, packaging, and materials all rising together.

At the same time, farmers are running up against credit limits, and we’re having to tighten payment terms.

The result: farmers are planting more soybeans to avoid high fertilizer costs, and those still planting corn are cutting back on nutrient use, which likely means lower yields.

Bottom line: supply chains are strained, costs are rising across the board, and the setup for higher food prices is already in motion.”

This is how it starts, not with headlines, but with small cracks in supply chains, rising input costs, and quiet changes in behavior on the ground.

The result: more soybeans, less corn, reduced fertilizer use and likely lower crop yields.

Bottom line: supply chains are strained, input costs are rising, and the setup for higher food prices is already in motion.” Planting decisions shift. Yields fall.

And then… it compounds.

My friend Dan concluded his note to me, “I hear the train a comin’, it’s a rolling round the bend, and we’re not going to see sunshine since (a long time), I don’t know when. We’re stuck in food inflation, and time keeps dragging on. But that train keeps rollin' on down...... (hat tip to Dan G.)

We may not feel it all yet, but it’s coming.

Grab that coffee and find your favorite chair. Nothing is more economically important than the Strait of Hormuz impasse. You’ll find my summary notes from an excellent conversation I had yesterday with another good friend/client and former CEO of a major oil company. Lights on, coffee hot, let’s go!

On My Radar:

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

Insights From a Former Oil Industry CEO

Steve M is the former Chairman, President, and CEO of a major oil company and an expert in chaos theory. His leadership approach was what I’d call heart-centered/human-centric. He was known for implementing the "Grassroots Leadership" program, a culture-shift initiative designed to empower lower-level employees to drive innovation and efficiency.

Beyond running a major oil company, Steve’s background includes teaching and lecturing, including a European lecture tour on chaos theory in management and internal business‑model training. He also served on the Council on Foreign Relations. What strikes me most is his ability to understand human behavior, teach in a simple, clear way… inspire others.

One of the stories I enjoyed was about a friendly wager with a senior executive. The executive wanted to fire the underperforming middle-level managers. Steve said, "Let’s do something. I’ll take the underperforming managers, and you take the top-performing managers. Let’s work with them, then measure their performance.” Not surprisingly, the underperformers beat the top managers. Leadership at its best. We need more Steve M’s.

Back to the problem in the Middle East:

Steve knows the major players in the Middle East and around the world. Through his lens of chaos theory and his keen read on people, he shared his outlook on the US-Iran war and discussed the immediate risks. This is challenging stuff. Nod along or disagree, I simply encourage you to take in the data.

With Steve’s permission, I share my notes with you. Let’s take a look - bullet point format:

I asked Steve M (“Steve”) to share his macro- and strategic read on the Strait of Hormuz and the US-Iran war as he has a depth of knowledge of the oil industry and its major players (countries / producers / upstream logistics, customers, etc.).

My bullet point summary notes:

Steve believes the US is in a “very difficult position” in Iran: clerical leadership is effectively decapitated, and the Revolutionary Guard is now in control.

Described the Iranian Revolutionary Guard as highly disciplined, decentralized, and structured on a “chaos theory” model (independent operating nodes without central command), analogous to how he ran global operations at his oil company.

They see themselves as “guardians of the revolution.” They will not back down.

They are more extreme than the clerical leadership. This regime change is not for the better!

Steve sees the current situation as more like “Vietnam than Venezuela” on a conflict spectrum: Like the war with Vietnam, the adversary can absorb punishment and just keeps coming.

Venezuela was done quickly. The “revolutionary guard” means their mission is to defend the revolution. They are more extreme than the mullahs. They are not going away.

How do you knock out the Revolutionary Guard? They are splintered teams with preexisting orders.

“There is no clear off‑ramp.”

Steve believes Iran has now learned that controlling the Strait may be more valuable than having nuclear capability.

There is no quick energy fix. Bypassing this via building new pipelines will take years.

He believes Iran’s nuclear threat is likely constrained by China: as the primary patron to Iran, China “would never let them get the bomb” and is more fearful of a nuclear Iran than the US.

China doesn’t trust Iran; Russia doesn’t trust Iran; China doesn’t trust Russia; and Russia doesn’t trust China. None of these countries are buddies.

Steve believes hopes for a popular uprising/regime change likely peaked, and the opportunity was missed in the January protests; economic sanctions alone rarely topple regimes absent sustained popular revolt.

He said Putin is in a “huge winning hand” due to higher oil prices: more income, the US depleting munitions, the US alienating allies…

Russia has an incentive to stay quiet while the US makes “strategic mistakes.” “Never get in the way of an enemy when they are making a strategic mistake.”

Steve stresses NATO’s critical importance and laments the underdeveloped US axis with Canada/Mexico. He expects Gulf allies (UAE, Saudi Arabia) to reassess US reliability and seek new alignments.

The US needs Europe, and Europe needs the US.

With both ends of the Strait of Hormuz closed, and likely to remain closed:

The US will be sitting ducks if it takes Kharg Island.

The Iranian Revolutionary Guard will fight to its death.

Concludes US will ultimately need to “climb down” and spin some form of face‑saving outcome.

That concludes my discussion with Steve.

Grab another cup of coffee and put your geek glasses on. I take in a great deal of research and have some good friends. One of my frequent reads is from Renè Javier Aninao at CORBU. It takes a bit of time to get used to his cadence, but it has some good information, and it is also worth putting on your radar.

Renè Javier Aninao | Managing Partner, CORBŪ

Some background color: Renè Javier Aninao is the Managing Partner of CORBŪ, a macro-intelligence and advisory firm that sits at the intersection of financial markets, public policy, and national security. He is a global macro strategist focused on how geopolitics, trade, and monetary policy shape markets and capital flows.

Prior to founding CORBŪ, Renè spent nearly a decade at Evercore ISI as a senior macro specialist advising institutional investors and policymakers. He also held roles at Eurasia Group, Citigroup, Shell, and Macroeconomic Advisers, building a career that blends markets, energy, and geopolitical analysis.

He is a frequent speaker and widely followed for his work on the evolving global order, particularly the intersection of economic policy, national security, and financial markets. Source: FinNotes

Email post: 4-22-26

Quick note, I spoke with Steve M just after reading Renè’s geopolitical update. It was timely.

From the April 22 email:

“First, from the top, a few things are clear:

The post-Islamabad negotiations momentum has totally stalled -- and that is not a near-term positive for the US-led Coalition

The extension of the ceasefire demonstrates the White House’s deep commitment to the “Ghalibaf delegation” -- he is quickly becoming a sort of “new Shah” -- to provide him with the 11th hour space to build and demonstrate credible leadership, and then deliver a durable consensus

However, there is no urgency on the part of the Iranian security establishment -- who is clearly testing the President’s resolve -- to resume negotiations, mostly because stuff like the threats of the blockade etc have still not disabused the hardline leadership of the notion that it can survive an attritional economic conflict vs the United States

Which means there is highly unlikely to be any Iranian capitulation on the “Witkoff 15 Points” until and unless the President follows through with decisive -- and arguably “escalatory” -- actions

Rene shared a tweet showing US rewards for information leading to the locations and successful elimination of six Iranians.

And which means there is no durable conflict resolution until we see the following three catalysts:

#1: The targeted assassinations of the recalcitrant IRGC factional leadership, particularly KCHQ Commander Ali Abdollahi and IRGC Commander Ahmad Vahidi and also [at this point] SNSC Secretary Mohammad Bagher Zolghadr

#2: The announcement from the US Navy of new transit pathway coordinates for secure passage through the Hormuz Strait

#3: The PRC [China] participation in the non-proliferation format and regional consortium to secure the stockpile of Iranian fissile materiel

Having boiled down the conflict resolution trajectory to these 3 outstanding catalysts, let’s add some detail on each of these, in turn.

RE (reference) the post-Khamenei Iranian political system and IRGC factional jockeying:

The Iranian political system is undergoing an historic shock -- one where the clerics have been totally euthanized from power -- and the different centers of influence across the security establishment are competing for decision making primacy in the post-Khamenei governance structure

So it is not just IRGC Commander Vahidi who, eg as Fred Kagan stated, is “running the country” -- but a broader set of stakeholders [see Middle East Forum here and here], each with their own often unaligned interests, and not so dissimilar to eg how Congress and the “Establishment” and the “Deep State” all, by design, have a say on the US President

In hindsight, the presence of Ali Jafari in the Islamabad delegation was a very bad sign -- he was there to impose a constraint on Ghalibaf, and not play a constructive role -- and the same goes for last week’s meeting between KCHQ Commander Abdollahi and Pakistani General Munir

In any case, given these sorts of nascent political system dynamics, there must be a third wave of US targeted decapitation strikes against all the Iranian military leadership simultaneously to break the logjam -- and that is an admittedly complex, time-consuming operation [hence, the delays]

And what we will write in this format is that there is immense pressure on Ghalibaf et al -- if he indeed wants state-to-state recognition from the United States -- to deliver and eliminate the factional hardline leadership that’s an obstacle to conflict resolution

RE the still-impaired freedom of navigation in the Hormuz Strait:

Will first reaffirm in the strongest possible terms that the President has made a grave strategic error -- mostly borne out of an effort to raise burden sharing amongst the Allies, given the USA’s fiscal constraints -- in the cognitive warfare domain by “ceding the argument” to Iran that it retains leverage and control of the Hormuz Strait

The present situation in the Gulf maritime domain is very far from the status quo exante -- and the President, if he indeed seeks to credibly claim a strategic victory, will have to fully deliver on his declaratory policy statements that the United States is “PERMANENTLY” opening the Strait and that this “WORLD EXTORTION” will “never happen again” [his words, not ours]

On that note, the USCENTCOM Task Force 59 [see here] a regional, multilateral effort of networked [undersea, surface, and space] autonomous capabilities is purportedly working on clearing the sealanes of any mines and establishing coordinates for a new transit pathway

However, we have no additional fidelity on “what’s taking so long” -- and, in the meantime, there are deeply concerning leaks out of the US Congress of the Pentagon’s classified assessments that it will take +6 months [?!] to confidently clear the Hormuz Strait of mines

We do know that the +850 vessels that remain stranded in the Hormuz Strait present real risks and challenges to any active maritime military activity -- with de facto NATO+ member Ukraine to soon provide some urgently needed capabilities and operational expertise in the Gulf

And the recent blockade-related interdictions have yet to restore market or industry confidence -- because they are, in any case, mostly intended to demonstrate US military competence and build deterrence vs Beijing-Putin and prove that US Joint Forces can still project power simultaneously across multiple geographic AORs [Areas of Responsibility]

RE (reference) the PRC principal guarantor for conflict resolution:

It remains highly uncertain whether Beijing has the capacity and willingness -- or if it’s even in the PRC’s long-term strategic interest -- to establish a more permanent, non-economic footprint in the region, eg encompassing activities such as the verification and monitoring process of the nonproliferation regime across the Gulf

More tactically, there is indeed tremendous PRC backfilling of Iran -- eg the precursor chemicals in the solid fuel needed to regenerate ballistic missiles -- a development that even surprised the President

That said, we do not assess at this point -- though this is an issue to be agreed upon at the principal-level during the state visit to Beijing on 15MAY -- that it either “violates” the President’s “agreement” with Xi Jinping or will derail the fragile economic trade truce between the USA-PRC

But to be clear, the redlines -- for now -- on backfilling from the PRC to Iran are the following:

NO weapons systems or weapons platforms from the stockpiles of the PLA or Party-State

However, things like hard USD funding [via goods imports] and component parts and intelligence targeting and any dual-use items from private companies like Poly Group and Norinco and AVIC are “allowed”

Because quite frankly, these are rather proportional responses in strategic competition vs Great Powers -- particularly when the United States does similar [in fact, much more] in its proxy conflicts against the PRC’s allies in the Russia-Ukraine war

Lastly here, will note that it’s highly questionable whether it’s in the long-term interest of PRC energy security to eg, provide the IRGC with targeting coordinates inside Arab Gulf countries -- though maybe much like Beijing forsook the economic relationship with Europe in favor of Putin, they might be forsaking the Gulf in favor of Tehran [TBD ?]

Putting it all together:

We remain in the “3rd quarter” of the conflict, and while the worst of the left tail outcomes have, for now, been truncated -- it is still premature for any side to declare a strategic victory

And while the USA can point to some great achievements -- eg, decimating the military of its 3rd largest adversary and decapitating the head of the world’s largest state sponsor of terrorism and demonstrating a military competence capable of quickly integrating the latest AI technologies into combined arms maneuvers

All that said, there are a slew of unassailable facts on the ground that remain -- where, despite hitting +13,000 static military targets and eliminating the Ayatollah, we still have:

The “Strait of Iran” -- where both markets and industry respond to Tehran’s pronouncements of whether the sealane is open, and not the USA’s or the President’s

No credible method of physically controlling the oil exports and associated revenues of the new Iranian junta -- as the blockade, while a very smart tactical move, is neither sustainable over the long-run nor does it achieve this objective [in fact, it adds to the geopolitical risk premia across the commodities complex]

+$70 forwards in the oil price -- an at least +$20-25 geopolitical risk premium -- that, in the absence of decisive US actions, is likely to be sustained and over time will have material pass-through effects on goods inflation and global supply chains and the reaction functions of central banks

USA policy decisions on escalation management and risk tolerance that have resulted in the transfer of Iranian strategic deterrence from the non-proliferation domain to global capital markets -- a far more powerful coercive tool than the antebellum “nuclear threshold status”

And if this status quo is allowed to normalize, it will grant the secular terrorist regime in Tehran a seat at the global economic decision-making table -- as now every asset allocator and corporate planner etc will be forced to take Hormuz risk into account -- an outcome that was unthinkable pre-conflict

And, where much like the pandemic shock, it will also further entrench the mindset of stockpiling and resiliency over efficiency and integration -- an outcome that, ceteris paribus, speaks to a lower valuation multiple for US firms with a large global footprint

And maybe most importantly for market participants, it would represent a doctrinal failure of the Treasury Secretary’s Operation Economic Fury -- where countermeasures were deployed “right of boom” as cost imposition, rather than “left of boom” as deterrence -- an approach with little difference from the Biden Admin’s logic vs Putin in 2021-2022 [sidebar: and rest assured, if this sequencing is deployed against the PRC, it would meet far more disastrous consequences]”

Renè Javier Aninao | Managing Partner CORBŪ

One World Trade Center

New York, NY 10007

You can email Rene here: rja@corbu.co

Views are those of CORBU research and are subject to change.

Interest Rates and Treasury Auctions

The 10-year Treasury Note yield continues to bounce around 4.30%. My guess is that Trump and Bessent’s line in the sand is 4.50%. I believe a gap above that will rattle markets. Remember that nearly $10 trillion in Treasury debt needs to be refunded, in addition to ongoing borrowing required to finance the nearly $2 trillion annual deficit.

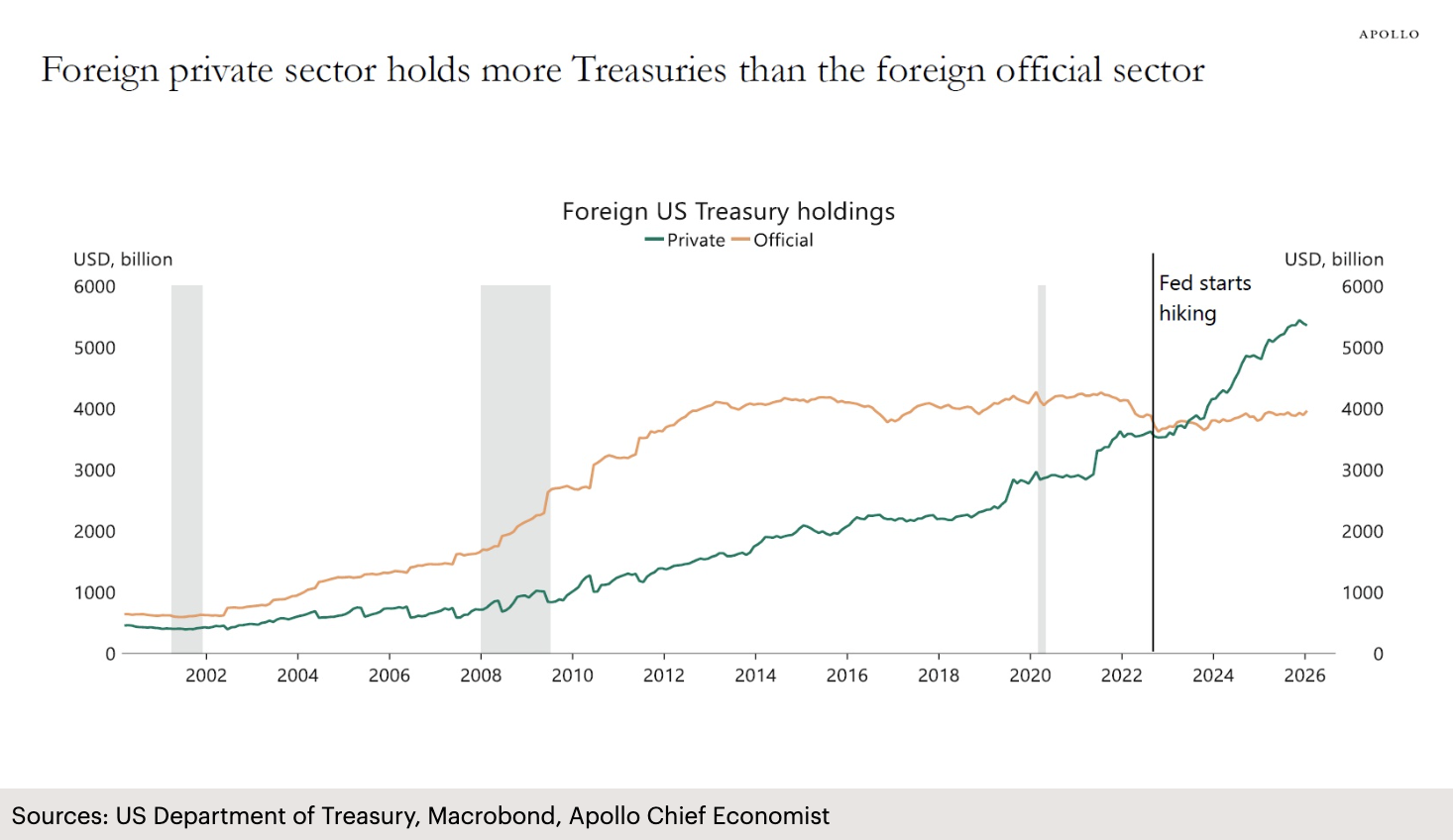

For the first time, foreign private investors hold more US Treasuries than foreign central banks, see the chart below. This is a structural shift that makes the Treasury market increasingly sensitive to the return expectations of price-sensitive private capital.

Source: Torsten Slok, Apollo

According to the most recent U.S. Treasury data released in April 2026, approximately $10.37 trillion of marketable debt is set to mature and require refinancing within the next 12 months.

The sheer volume of debt maturing in 2026 creates a significant fiscal feedback loop:

Average Interest Rate Rise: As of March 2026, the average interest rate on total marketable debt is 3.365%. However, new 10-year Treasuries are currently being issued at 4.30% and 30-year bonds at 4.90%. Source

The Refinancing "Tax": Every dollar of the $10.37 trillion being rolled over this year is moving from older, lower-rate coupons (some as low as 1.5% from five years ago) to these 4%+ current rates.

Net Interest Outlays: Currently, ~20% of the $5 trillion in annual tax receipts goes toward paying the interest on the debt. That is more than the entire national defense budget.

The Key Takeaway: The "Maturity Wall" of 2026 is a significant reason why yields are staying "higher for longer." The Treasury cannot afford a failed auction when it has $10 trillion to roll over, so it must keep yields attractive enough to entice the "yield-sensitive" domestic buyers.

Behaviorally, it seems that Bessent and Trump’s ceiling on the 10-year Treasury yield is 4.4-4.5% and no higher. If we get food inflation, we move through 4.5% quickly. This is an important level to watch.

As I noted last week, hedge funds own a record-high 8% of US Treasuries, and with combined repo and prime-brokerage borrowing exceeding $6 trillion, any forced unwind of these leveraged positions could send shockwaves through global fixed-income markets. Source: here.

The biggest buyers, other than hedge funds, have been the Fed itself and other US banks.

The "Hidden" Demand Problem

I keep an eye on the Treasury’s bond auctions, and they appear to be okay for now.

The bid-to-cover ratio is the "canary in the coal mine" for Treasury demand. It measures the total value of bids received versus the amount of debt sold.

As of late April 2026, the data shows a market that is "hanging in there," but the cracks identified in the Jacobs-Sengupta Fed paper, “The Changing Investor Composition of U.S. Treasuries, Part 2: Who’s Buying U.S. Treasuries?” are becoming visible in the auction results. Here is a look at “Recent Auction Results (April 2026):”

Security Auction Date Bid-to-Cover Ratio Yield Status

20-Year Bond

Auction date: April 22, 2026

Bid-to-cover: 2.68x

Yield: 4.88%

*Strong enough to avoid a "failed" auction, but required a higher yield to attract buyers.

10-Year Note

Auction date: April 15, 2026

Bid-to-cover: 2.54x

Yield: 4.28%

*Slightly above the 6-month average (2.49x), showing institutional buyers still value the 10-year benchmark.

30-Year Bond

Auction date: April 15, 2026

Bid-to-cover: 2.37x

Yield: 4.88%

* Lower demand for long-duration debt as inflation risks (Hormuz/Ag-Inputs) remain elevated.

2-Year Note

Auction Date: March 31, 2026

Bid-to-cover: 2.59x

Yield: 3.94%

*A strong result

While a ratio above 2.0x is generally considered "healthy," the quality of the bidders is changing.

The "Tail" Risk: The 30-year auction on April 15 "tailed" by 1.5 basis points. In trader speak, a "tail" means the final price was lower (yield was higher) than what the market expected just before the auction. This indicates that the Treasury is having to "sweeten the deal" at the last second to clear the $10 trillion refinancing wall.

Indirect Bidders (Foreign Demand): Foreign participation has dipped to 64% in recent long-bond auctions, down from a 2025 peak of 72%. This confirms the Fed's warning that we are increasingly reliant on yield-sensitive domestic hedge funds rather than stable foreign central banks.

The "Basis Trade" Dependency: A large portion of the 2.5x+ coverage in the 2-year and 5-year notes is coming from hedge funds executing the "basis trade" (leveraging the difference between cash Treasuries and futures). If volatility in the Strait of Hormuz causes a "margin call" in these trades, that 2.5x bid-to-cover could evaporate overnight.

The Bottom Line:

The auctions are currently finding a clearing price, but that price is painfully high (4.8%+ for long bonds). The "Bid-to-Cover" isn't signaling a collapse yet, but it is signaling exhaustion.

Watch for any 10-year or 30-year auction where the bid-to-cover drops below 2.30x. That is the "danger zone" where the market effectively tells the government: "We aren't buying any more unless you pay us significantly higher interest."

Watch the 4.50% yield level on the 10-year. A break higher will be concerning.

Keep your eyes on global government bond yields. They are likely heading higher.

Valuations remain high, equity ownership levels remain high, margin debt is high, and government debts remain the greatest risk. Yes -invest, but invest in the assets most likely to benefit in the periods ahead. If you must own the S&P 500 Index, find a way to risk hedge your exposure.

See important disclosures below.

* No guarantees; all investing involves risk. Views are subject to change. TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

As always, this is not investment advice. For discussion purposes only. Reach out to us if you have any questions.

Views are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. See important CMG disclosures below.

If you like what you are reading, click on the link and share it with a friend (it’s free).

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not intended to recommend buying or selling any security and is for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: April 23, 2026 Update

Trade Signals - subscribers only

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Peace

Steve M is happily retired with a golf game I envy. He tracks his stats closely; the last update had him sitting about five over after something like sixty holes. Not bad. Distance off the tee isn’t what it used to be, but that just tells you everything you need to know about the short game. Deft touch and precision.

He’s also a die-hard Astros fan. We bonded over baseball years ago, and lately, both our cities have had a few good runs. We keep an annual wager - his Astros vs. my Phillies. Winner hosts: golf at his club or mine at Stonewall.

Both teams are off to a rough start this season. The invite stands either way… but I’ll admit, it’ll feel a whole lot better seeing him in a Phillies cap. A warm hat tip to my friend.

US–Iran: Stuck in Folsom Prison

“I hear that train a-comin’, rolling ’round the bend…”

Feels about right.

As I’ve been writing these past few weeks, keeping the Strait closed is a ticking time bomb for the global economy. Imagine the jockeying for power that is going on in Iran. Steve added, “The Iranian Guard in a an structure and mode (splintered teams with preexisitng orders) is difficiult to break.” We’re running short on time, and the margin for error is thin. There are no obvious off-ramps.

I’m praying for a workable resolution. Praying for peace - for the Iranian people, for the region, and frankly, for all of us.

People everywhere feel the strain right now.

So maybe we take a page from Steve M’s steady way, calm approach, and let’s focus on what we can control. Pick up someone’s spirits. Every small act of kindness goes a long way.

Wishing you and your family a fun-filled, peaceful weekend.

Glasses high - “peace!”

With kind regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.