On My Radar: Oil, Food, and Fertilizer

April 17, 2026

By Steve Blumenthal

“There is nothing more inflationary in the long run than a government that needs to print money to pay its bills.”

— Luke Gromen, FFTT-LLC (Macro Voices Podcast)

The markets are higher today. Iran declared the Strait of Hormuz is open; however, Trump said the U.S. blockade is still active.

I listened to an excellent podcast on my flight home from Utah yesterday. The topic was the economic implications of the war with Iran. Luke Gromen was interviewed by Erik Townsend on the Marco Voices podcast. You’ll find my summary notes in bullet point format, and I think, like me, you’ll more broadly grasp the enormity of the economic risks. But first, let’s take a look at the epic stock market run.

If you are a Trade Signals subscriber, it’s been a big week in the markets. I want to wait for today’s closing data before I send you the report. Stay tuned.

Grab that coffee and dig in. There are many charts, but you’ll find the post reads quickly.

On My Radar:

Personal Note: Snowbird, Home, and Austin

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

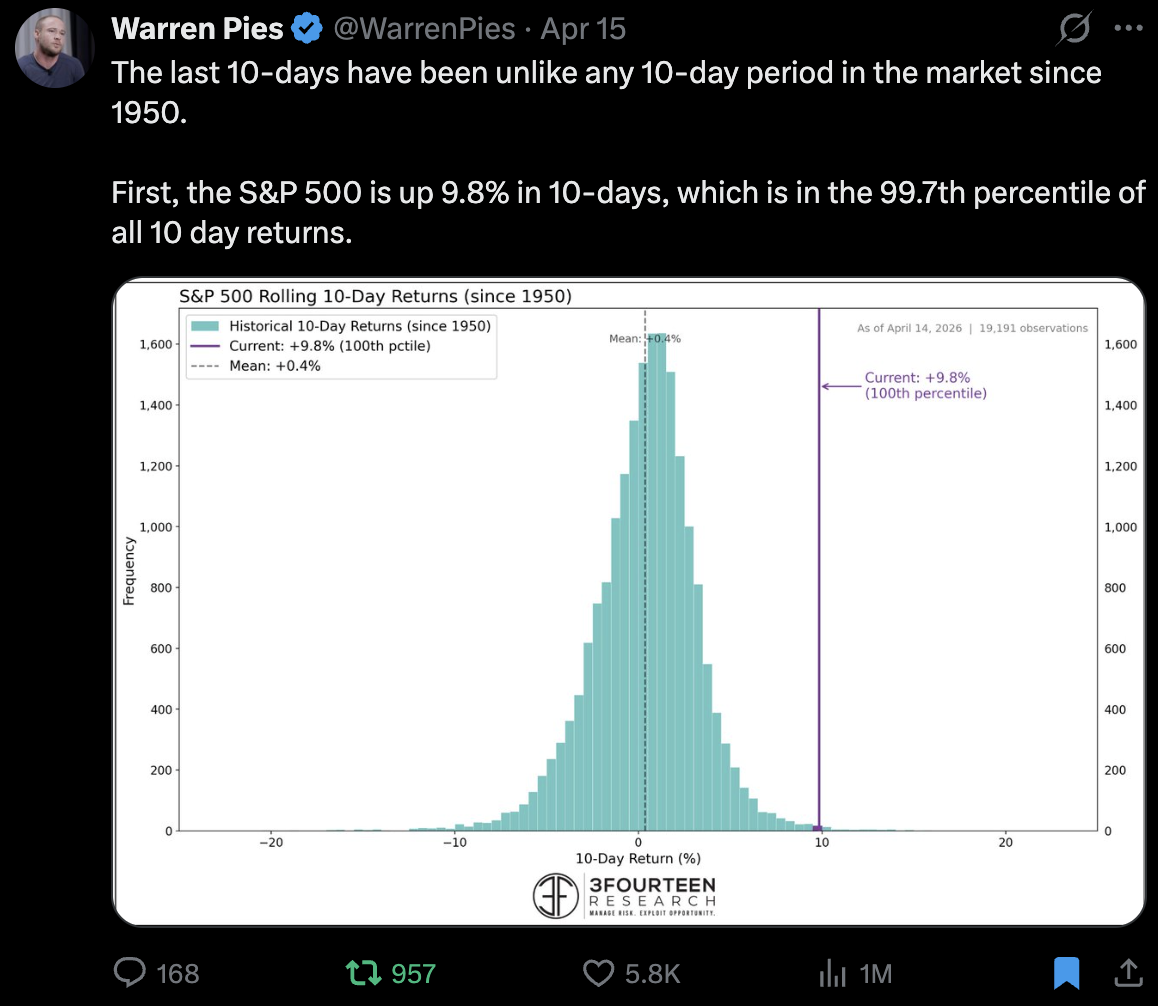

Record Run

Source: @WarrenPies, 3Fourteen Research

Not the time to turn bullish. We went from extreme fear in investor sentiment to neutral investor optimism. This chart shows just how pessimistic investors were just a few days ago, with near-record put option buying (betting on a market decline) relative to call option buying. Thus, the explosive unwind of investors shorting the market.

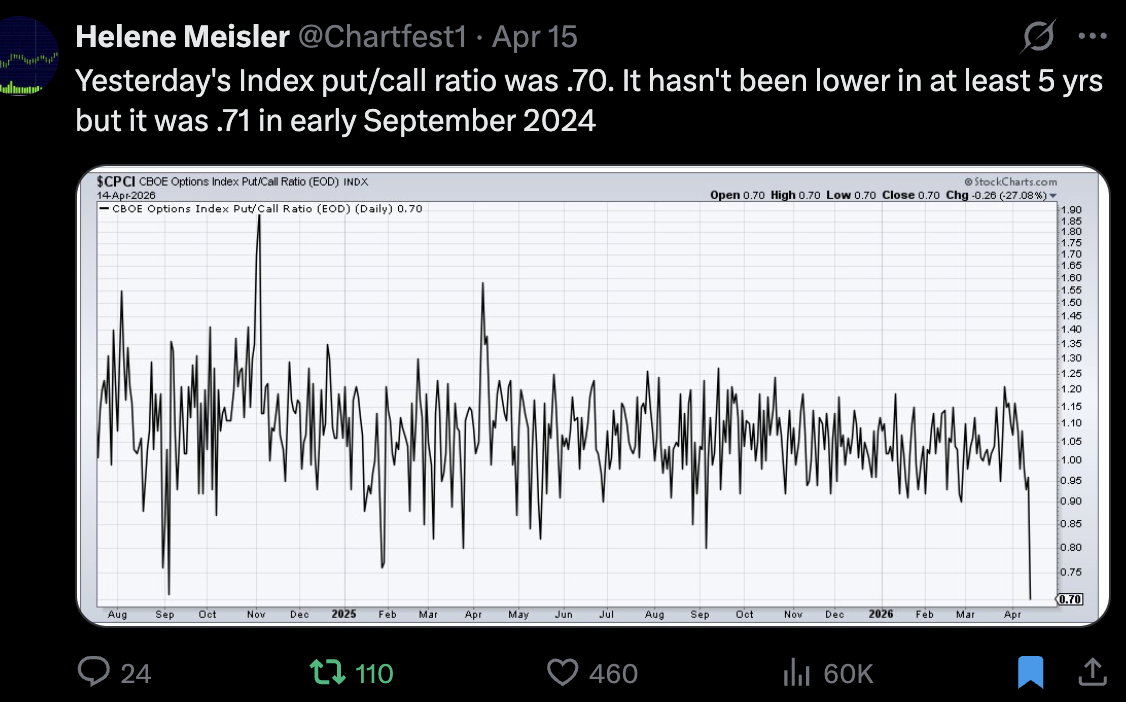

Source: @chartfest1, Stockcharts.com

But just how healthy is the buying?

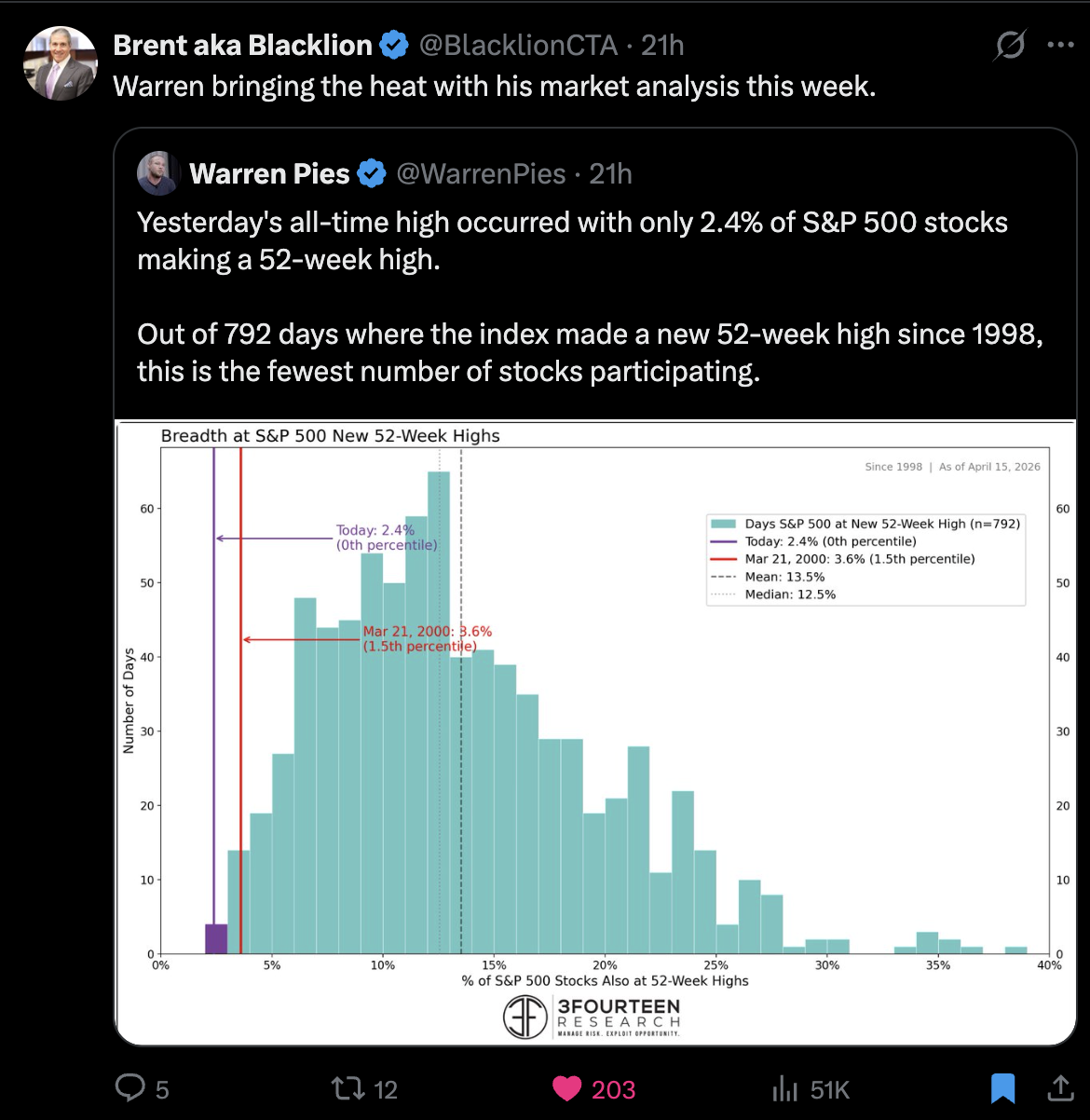

Source: @WarrenPies, X

Oil, Food, and Fertilizer

Here is the link to the Macro Voices discussion with Luke Gromen. Following are my summary notes in bullet point format (my comments italicized):

Luke Gromen, April 13, 2026, Macro Voices

As long as Hormuz is closed, we are accelerating toward a bad economic outcome.

We are now 7 weeks in, still closed; supply-side issues are starting to stack up.

Base case until it reopens, supply chains get worse from here.

Most people are not factoring this in.

This is existential for China and for Russia. However, there is a lot they can do.

SB side bar to give you a sense (see source links at the bottom of this section):

Beijing has begun using physical obstructions to regulate access to disputed but strategically vital areas:

Scarborough Shoal Barrier: This month, China deployed a floating barrier at the entrance to the Scarborough Shoal. While localized, this tactic serves as a "proof of concept" for blocking entrance to lagoon-based ports or narrow straits that serve as secondary trade routes.

Spratly Islands Sabotage: The Philippines has formally accused Chinese "fishermen" of using cyanide to poison waters around vital shipping lanes in the Spratly chain this month. This is viewed as an effort to "clear" the area of local civilian activity to allow for total Chinese maritime control. China denies this took place.

China appears to be moving to turn its 2022 security pacts into a permanent logistical "Island Chain" that could act as a gateway to block U.S.-Australia trade:

The Solomon Islands Hub: Recent reports confirm the development of a "fishery base" and "operations center" in the Solomon Islands, including an oil and gas terminal.

This allows Chinese ships to "replenish and stopover" deep in the South Pacific. In a crisis, this infrastructure would enable China to monitor or harass the trans-Pacific shipping lanes that Australia and New Zealand rely on for 90% of their trade.

Game of Thrones-like activity is playing out before us.

Back to Luke Gromen interview:

Will the U.S. be forced to pull back or print and let rates rise?

Luke noted that the only other times when the economy was rapidly declining, and investors were complacent, were the 4th quarter of 2007 and the 1st quarter of 2020.

Individual names are getting crushed by supply chain challenges. The more this becomes apparent, the market will respond.

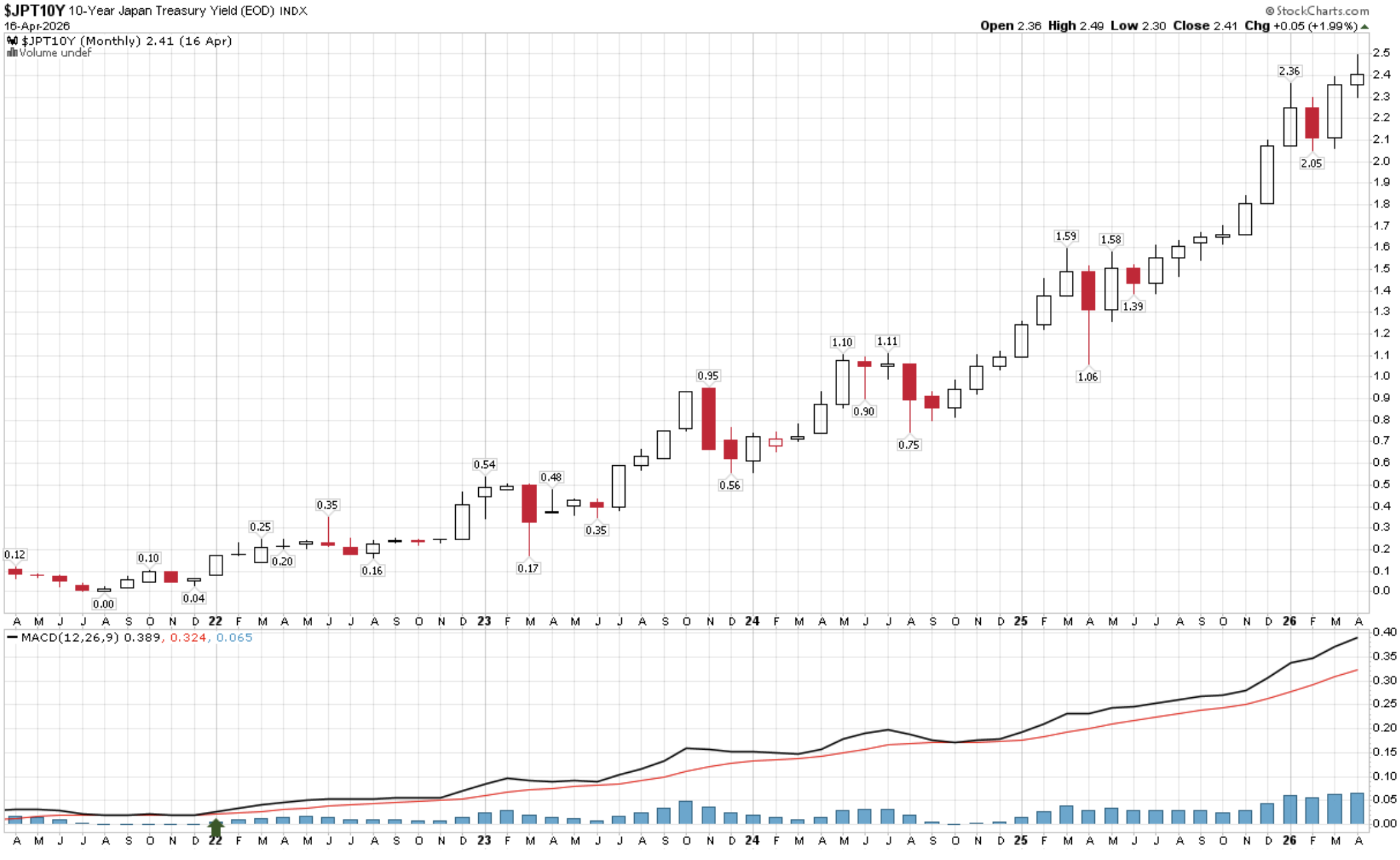

Japanese yields are spiking higher.

The last tanker to transit was Feb 28. It will arrive at its destination next week. Nothing else has gotten out… actual disruption to supply hasn’t had its impact yet. There is a six-week lag of crude into the rest of the world. Takes more than a month and a half to get to the destination.

The Strait of Hormuz could be closed by mid-May or mid-June. Hundreds of millions could be impacted. Crop outputs impacted… Food inflation higher…

Expect to last much longer than we expect… His base case: Hormuz is closed for another month.

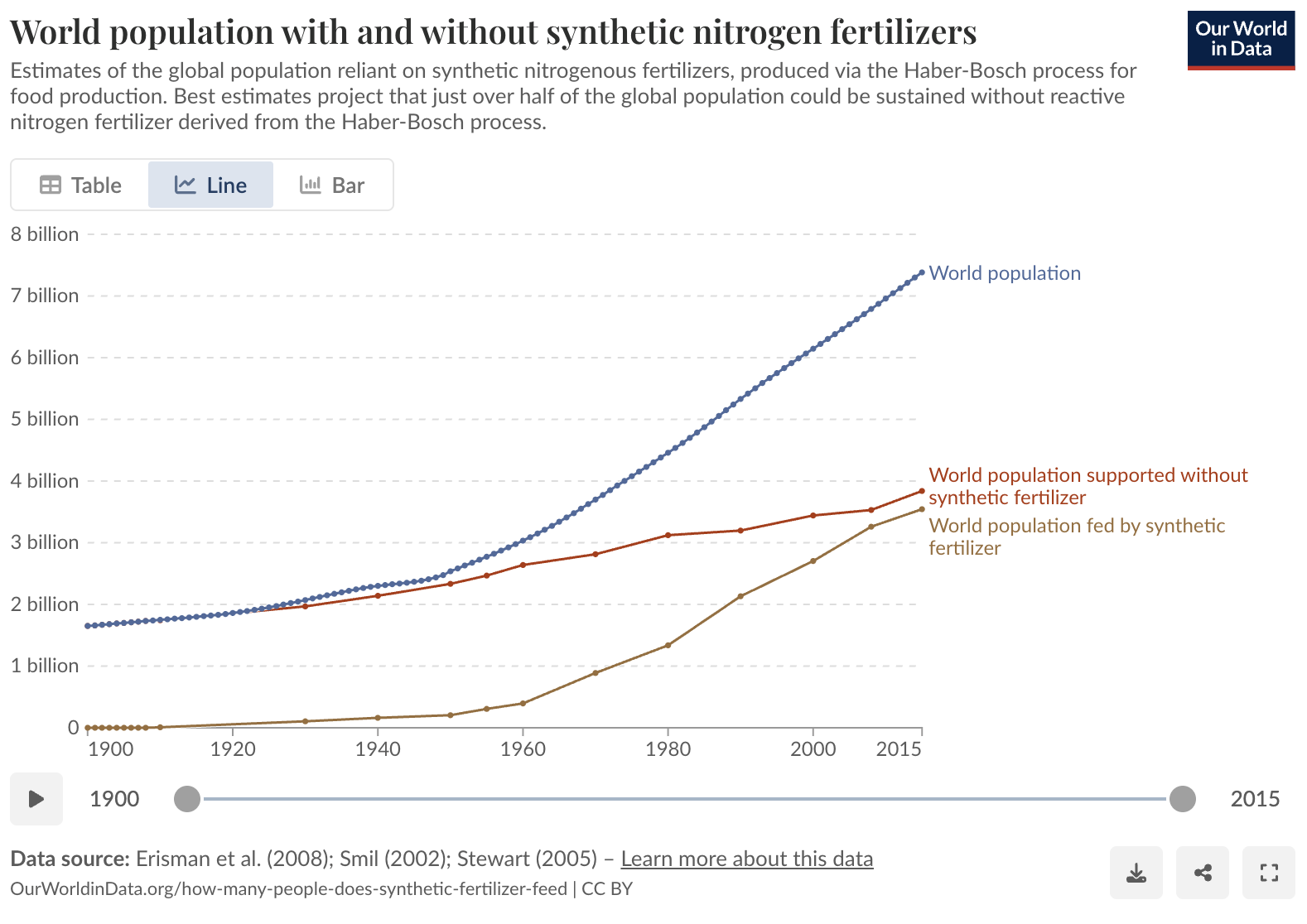

One of the most famous visualizations comes from the research site Our World in Data. Their analysis in 2015 on the impact on the global population without synthetic fertilizer:

Total Population in 2015: Roughly 7.5 billion people.

Population supported without synthetic fertilizer: They estimated that there would be 3.9 billion people.

The "Gap": This means approximately 3.6 billion people (nearly half the world) are alive today because of the Haber-Bosch process, which creates synthetic nitrogen fertilizer.

The Scale of Dependence

The Strait of Hormuz is responsible for transiting a massive portion of the world's fertilizer supply:

Final Product: Approximately 30% to 33% of all fertilizer traded by sea passes through the strait.

Urea (Nitrogen): The dependence is even higher for Urea, the world’s most used fertilizer. Nearly half (46%) of all global urea flows originate from the Persian Gulf and pass through the strait.

Feedstock (LNG): About 20% of global Liquefied Natural Gas (LNG), the "fuel" used to create synthetic nitrogen, transits the strait.

We won’t see the impact of this until 6-12 months down the road when crops are harvested. Food inflation impact. Crop yields fall, need for food constant, prices move higher.

Asia and Australia, who need diesel fuel may be hit hardest. Risk of starvation in poorest parts of the southern counties.

This will cause a spike in inflation with bond yields at 4.3%.

Behaviorally, it seems that Bessent and Trump’s ceiling on the 10-year Treasury yield is 4.4-4.5% and no higher. If we get food inflation, we move through 4.5% quickly.

Do they come in and print like crazy to support markets, which may help in the short term, but will hurt in the long term with higher rates and higher inflation?

This entire situation could trigger an inflation shock wave.

Hormuz staying closed for another 30 days is likely.

It could stay closed until the Fourth of July, which turns this into an economic and humanitarian crisis not seen in our lifetime.

We have not even seen the shortfalls yet, and this may last much longer than anyone expects. It is possible the Strait is still closed by the Fourth of July. Nobody is thinking about that.

Think: Food riots across the global south, political instability, bond problems, not a good environment for risk-taking.

If closed for another month, which is probable, it will be a supply chain disaster.

Government Debt crisis cliff:

Governments will likely come in and support like crazy. Luke emphasized, “We are starting at an already near crisis high debt level.”

Japan is close to a bond market crisis. Their government bond yield is rising, and normally, you’d see the Yen rise with it. That is not happening. It is weakening against the dollar. We haven’t seen this before.

(SB again) Here is a look. First, the 10-year Japanese Yield

Source: StockCharts.com, CMG Investment Research

Next, the Yen:

Source: StockCharts.com, CMG Investment Research

Back to Luke

The market is saying higher yields won’t strengthen your currency; they are going to weaken it because we know you can’t afford higher yields. They are going to have to print.

Japan owns a lot of US bonds and stocks (think of it as Japan’s piggy bank, with trillions of dollars). They could sell them and bring the money home. If you can’t get food or energy, if you can’t feed your family, you’ll sell everything you own to do so.

The world owns 70 trillion in dollar-denominated assets, gross, and 27 trillion net. The selling of U.S. bond and equity assets will have a bearish impact on the U.S. investment markets.

His point: Countries that have run surpluses for a long time have some room to finance themselves before having to print money. Japan, Korea, and Germany to some extent.

30 days takes us to mid-May; 90 days takes us to mid-July. Think about the impact on markets.

Countries will have to print money to buy food. Highly inflationary.

If Hormuz stays closed, the world economy will collapse.

Not a guess.

We can debate timing, but 100% it will collapse.

If so, that will be deflationary.

Iran’s plan is to keep it closed.

The U.S. fiscal year is 6 months in (as of the end of March). U.S. true interest expense, which includes entitlements, veterans’ affairs, and interest-like expenses, is 102% of revenue receipts. We are in very bad financial shape. (SB here: An end of the long-term debt cycle problem).

Inflationary and deflationary implications:

Inflationary impulses of higher commodities and higher oil prices,

deflationary impulses from those same things - costs up, rates up, dollar up, economy slows down.

Then the question is: will the U.S. government print to cover, or will it default on bonds and entitlements?

Bottom line: No chance they default. They will print.

“There is nothing more inflationary in the long run than a government that needs to print money to pay its bills.”

From an investor’s perspective, the easy part is determining whether the Strait of Hormuz is open or closed. The hard part is timing when it is inflationary, or when it is not inflationary.

How long before the governments print to cover interest and entitlements?

How much will they print to subsidize food?

This timing is too hard to know, which makes it anyone’s guess to trade the markets short-term.

Luke is confident that an oil spike and a food spike will cause a slowdown and a recession. Particularly when married with higher interest rates and disruption to supply chains.

He expects an ongoing “yin and yang” between inflation and deflation. (SB - my waves of inflation until the “grand restructuring” theory.)

Governments will likely have to print more money amid a spike in commodity prices.

Are we headed toward a fiscal crisis?

In a word, yes.

Luke on investment positioning:

In the short run, Luke Groman is sitting on cash and gold.

“Government deficits don’t matter until they do, and then they matter a whole lot.”

Where are the buyers of U.S. debt going to come from?

Foreign central banks have not bought Treasuries since 2016.

Japan has bought a little more, the UK has bought a little more (mostly investors and hedge funds),

The largest 37% of buying has come from the Cayman Islands, specifically U.S. hedge funds (Source: Fed white paper from the October 2025 study). The hedge fund trade is known as the “treasury basis trade.” We’ve gone from stable buyers to a dependency on highly leveraged hedge funds.

(SB here) The Treasury basis trade is an arbitrage strategy popular among hedge funds.

The "basis" refers to the small price difference between the cash Treasury and the futures. When the futures trade at a premium to the cash bond (net of carry/financing costs), the trade profits as the prices converge by futures expiration, when the bond can be delivered against the contract. It is largely market-neutral to interest-rate moves but relies on high leverage (often 10-20x) to achieve meaningful returns and carries risks from repo financing costs and liquidity squeezes. In short, it exploits temporary mispricings between the two highly related instruments while providing liquidity to the Treasury market. Source: en.wikipedia.org

Hedge funds own a record-high 8% of US Treasuries, and with combined repo and prime-brokerage borrowing exceeding $6 trillion, any forced unwind of these leveraged positions could send shockwaves through global fixed-income markets. Source: here.

The biggest buyers, other than hedge funds, have been the Fed itself and other US banks.

When global central banks stopped buying treasuries and started buying gold, long-term treasury bond futures priced in gold are down 90% since 2014. It’s been a one-way, beautiful trade.

When does it go critical? Luke says, " This is the part that investors are completely complacent about.

China can slow the supply chain, causing more inflation, and the bond market will do the rest (higher yields).

The U.S. government can cap interest rates or release false inflation figures, but politically, everyone will see and feel inflation.

He added that if the Republicans lose the midterm elections in both the House and the Senate, the next two years will be spent with us watching impeachment proceedings.

One way or another, China can force this dynamic on the bond market. They can block our supplies and limit trade. There is nothing more inflationary than war.

The big macro risks:

Japan and other surplus countries are selling dollar assets for food and energy.

The net supply of treasuries may rise dramatically. U.S. deficits (especially if we have a recession), foreigners selling, causing higher interest rates, the biggest marginal buyers (leveraged U.S. hedge funds basis trade), reduce exposure as vol spikes (more selling, not buying). An additional accelerant to the Wylie Coyote moment.

Luke is bullish on: Energy, uranium, domestic electrical infrastructure, reshoring beneficiaries, nuclear, oil e&p, gold, and he’s generally bullish on Bitcoin. He added that it is good to look for the opportunity that presents itself on the other side of this crisis.

FFTT-LLC.com's goal is to identify more and less attractive sectors, as well as global macro research…

Our view here at CMG is similar, but we also like robotics, aerospace and defense, natural gas, and quantum computing. Not a recommendation for you to buy or sell anything. Speak with your advisor or us.

This chart caught my eye:

Macro Voices is hosted by Erik Townsend and Patrick Cresena

Just a bit more on the situation in Iran. In the same podcast, they next interviewed energy expert, Rory Johnson. Following are my bullet point notes:

No uptick in tankers getting through Hormuz.

Normally, 140 ships travel each day; 7 are on the Bloomberg tracker today (April 16, 2026).

13 million bpd of oil is not getting through (via Very Large Cruise Ships or VLCCs). Basically, seeing only 50k bpd via small ships.

No VLCCs are getting through.

Two empty VLCCs were let through back into Hormuz.

Trump is going for maximum economic pressure.

If this lasts another week or two, it will accelerate pressure on Iran and bring them to the table for a peace deal. This pressure is just starting on Iran.

Who will bear the economic pressure longer? It is just a matter of time before the largest supply shock in the history of the oil market bears down on prices, pushing them higher.

Iran is threatening to close the Red Sea southern strait by activating the Houthis. Could get oil out going through the Suez, but it takes way, way longer to deliver. We are in a far more painful market state, so this would be late… (it takes an extra 2 weeks to reroute around the Horn of Africa).

Supply disruption has not yet started – it will start next week.

It is coming, and it cannot be stopped. There is an air pocket after the last tanker delivered.

East Africa felt after ~3 weeks, East Asia after ~4 weeks, Europe after ~5 weeks, and now North America after ~6 weeks.

North America is generally the least exposed.

What we’ve seen in each of the early markets, East Africa, East Asia, and Europe, is that conditions tightened up almost immediately.

The US Gulf Coast is now the world’s supplier of energy. Tankers are coming to the US because other people are willing to pay more than US buyers.

Rory Johnson – CommodityContext.com, Twitter, and Oil Roundup Podcast

The following is from Mauldin Economics:

Geopolitical Analyst George Friedman summed the situation up this way:

“Key Points:

The stated US goal in initiating war against Iran was to prevent Iran from acquiring nuclear weapons and using that capacity to dominate a key region.

So far, neither side has been able to defeat the other militarily. Both need to reach a conclusion that doesn’t threaten national or regime survival.

Iran’s weakness is that the US is inherently more powerful in terms of weapons production and capability. The US weakness is its leadership's vulnerability to American public opinion.

The Iranian regime appears to have subdued its internal enemies, giving it a stronger negotiating position. Meanwhile, political reality makes it difficult for the US to credibly threaten extended war.

Iran’s leadership believes that extending constraints on the world’s oil supply will weaken the US government at home and also cause other nations to pressure the US to end the fighting.

Paradoxically, Iran has far more to lose in this war, yet the longer it lasts, the more favorable its end will be for Iran.

The American dilemma is similar to the Vietnam War, where the communists could win by imposing a stalemate. It took over a decade, but domestic opposition eventually led the US to withdraw.

Bottom Line: The difference between this war and Vietnam is in the economic stakes, which are vastly higher and affect the entire world.”

By the way, the Mauldin Economics conference is just a few weeks away. George will be speaking. You can click here to learn more.

Recession and equity bear-market risk remain high. Keep the next chart in mind regarding economic shocks from oil price fluctuations. It plots the month-by-month rate of change of the price of Light Crude Oil. The bottom section indicates that every major stock market correction has one thing in common: a price rate of change of 100% or more.

Click on the image for more details.

Source: X, Ted @TedPillows, @marketmike

Keep your eyes on global government bond yields. They are likely heading higher. If correct, bearish for most traditional assets. See important disclosures below.

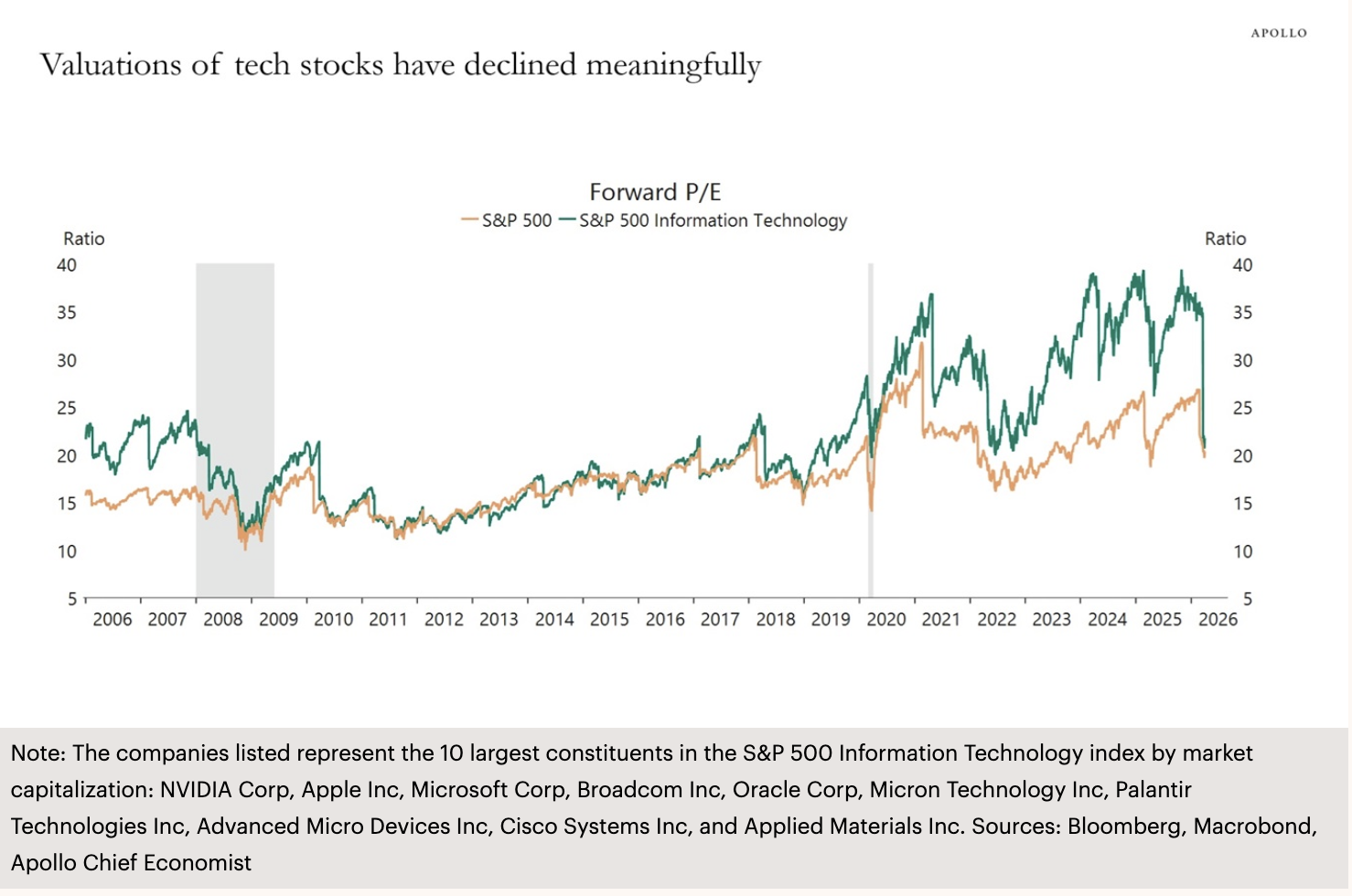

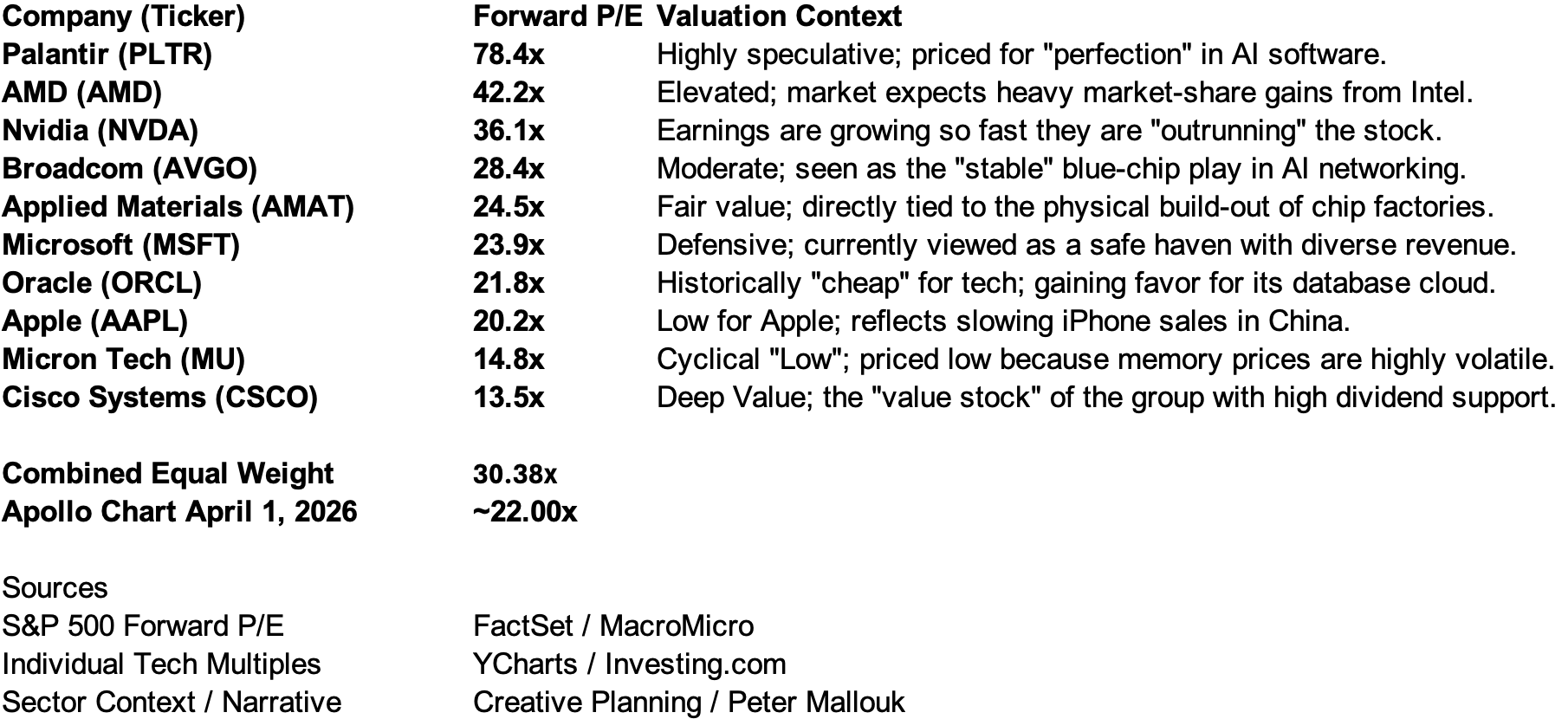

Tech Stock Valuations

The next chart below compares the forward P/E ratios for the S&P 500 and the S&P 500 Information Technology sector.

I set this chart aside a few weeks ago, just prior to the historic two-week stock market run. But it is still informative.

Tech valuations had compressed from 40x to 20x, and we were back at levels last seen before the AI boom began. Source Apollo

However, the recent rally has put the Forward PE at ~30.38x.

Bottom line: That would have been a good pitch to swing at, but you’ll see further below, not such a good idea today. Though we can gain some insight into the next opportunity.

Source: Apollo, Torsten Slok 4-11-26

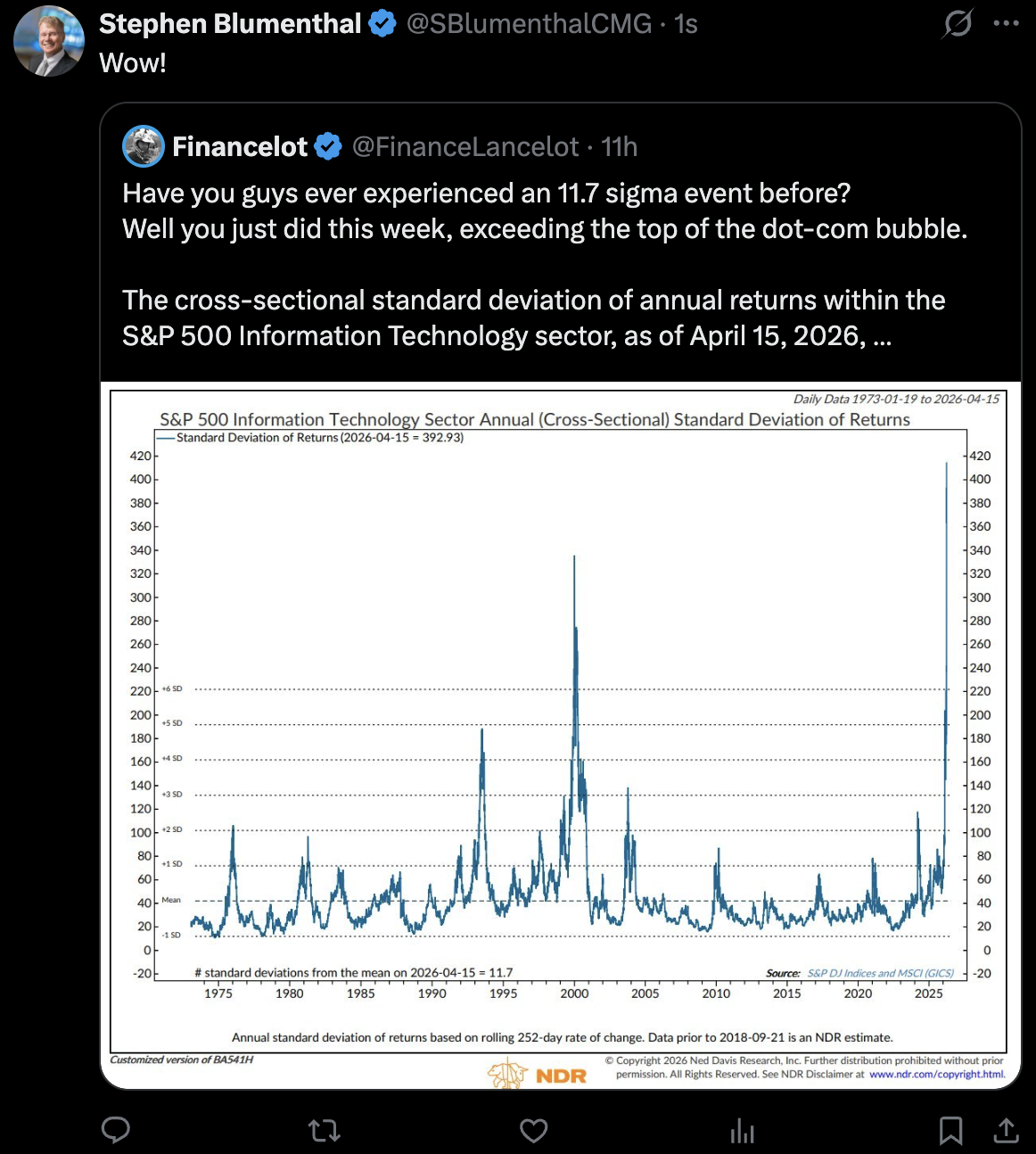

To get a sense for the massive move, take a look at this next chart.

Just how historic - one standard deviation moves happen fairly frequently.

Three standard deviation moves are infrequent.

The current 11.7 event is off the charts.

Bottom line: Expect some retracement.

Source: X, @FinanceLancelot

Here is the data today, April 17, 2026.

Source: CMG Investment Research, Fact Set, YCharts, Creative Planning

The combined (Weighted) Forward P/E, on an equal-weighted basis of these 10 stocks, is 30.38x as of today, April 17, 2026. A sharp increase from the ~22.00x data Apollo provided in its April 1, 2026, chart.

On My Radar Analysis:

Vs. S&P 500: The broader market (S&P 500) currently trades at a 20.4x forward P/E. The "Mag 10" basket carries a 50% premium to the market.

Notice that the "old guard" (Cisco, Apple, Microsoft) is now significantly cheaper than the "new guard" (Palantir, AMD).

The "Nvidia Paradox": Despite the hype, Nvidia's Forward P/E (36x) is now actually "cheaper" than AMD's (42x). This suggests Nvidia is effectively "earning its way" out of its prior bubble status.

My two cents: A 30.38x forward P/E for the leaders of the global economy is high, but not "dot-com bubble" high (which exceeded 60x). A better entry is below a forward PE of 25x.

I previously saved the Apollo chart to share with you this week, simply to point out that the Mag 10 stocks were back to a good forward PE level.

It has been an unprecedented two-week run in the stock market. I don’t believe the market volatility is over. Keep the 22x level in mind as a reasonable value buy point.

Stay nimble. Stay thoughtful. I’ll keep watching the signals closely and share them with you as they evolve.

Ever forward… let’s go.

* No guarantees; all investing involves risk. Views are subject to change. TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

As always, this is not investment advice. For discussion purposes only. Reach out to us if you have any questions.

Views are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. See important CMG disclosures below.

If you like what you are reading, click on the link and share it with a friend (it’s free).

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not intended to recommend buying or selling any security and is for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: April 16, 2026 Update

Trade Signals - subscribers only

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Snowbird, Home, and Austin

It is warm and sunny here in Philadelphia, and I’m hoping to take a little money out of my good friend Wade’s pocket tomorrow afternoon. The trees have turned green, early spring colors are popping, and lunch and golf at Stonewall with a dear friend is just about as good as it gets.

Speaking of spring, we were treated to some fine conditions out at Snowbird, Utah. The groomers were fast, the edges held, and we even found a bit of “corn snow”—which, for those who ski, is about as fun as it sounds.

If you read last week’s note about my father and his spiritual resting place behind the 12th tee at Augusta National, you’ll appreciate this. My children, cousin Tommy, and I also laid some of Pop’s ashes at 11,000 feet atop Snowbird. A quiet moment, a simple salute… and then off we went, racing down our favorite run—now affectionately known as Pop’s Path.

Snowbird: Lower left - Brie, Tyler, Matt, Steve / Thaxter upper right and Dan lower right

A big hat tip to Dan. He’s been the first to greet me and thousands of others every year at Stonebird. We’ve grown to be friends. When he told me he was retiring at the end of the season, my heart dropped. I have known him for 30-years. The good news is that he retires with a lifetime ski pass. Dan, next year we'll ski together. Congratulations and enjoy your retirement!

And what a Master’s it was. Rory’s final drive on 18 - way right, it was the kind of miss you, and I know well, but it was so far right that it left the door open. Up two strokes, he pulled off a remarkable second shot on 10, launching it over the trees and even the 18th scoreboard. From a tough lie in the bunker, he put his third on the green and calmly two-putted for the win. A special moment.

Hard not to feel for Justin Rose - so close once again. And Cam Young just couldn’t buy a putt. Both seem like class acts. Rory was all grace - his words afterward spoke volumes about his love for family and the journey it took to get there. “Process over outcome, process over outcome,” he’d remind himself. I need to heed that advice.

I’ll be heading to Austin later this month for a few family office meetings - always good energy down there.

Wishing you and your family a wonderful week.

Head up, glasses high! Let’s toast to peace.

Kind regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.