On My Radar: The Dollar: “Secretariat by 31 Lengths”

February 27, 2026

By Steve Blumenthal

“Remeber to be an advocate and a champion for the people in your life.”

- Andy McOrmond

I’m writing to you from beautiful Park City, Utah, where I’m attending the annual WallachBeth Winter Symposium. Mornings are filled with presentations and discussion; afternoons are reserved for skiing. A pretty wonderful combination.

About 160 participants are here, representing many of Wall Street’s leading firms: JPMorgan Asset Management, Goldman Sachs, NYSE, Nasdaq, VanEck, CBOE, State Street, BNY Mellon, AllianceBernstein, T. Rowe Price, Grayscale, BondBloxx, Direxion, Pacer, and others. The group includes research analysts, product specialists, wealth advisors, and family offices. A thoughtful mix of people who spend their days trying to understand markets and the world.

This marks the 15th year of the conference and my 12th attending. It is hosted by my good friend Andy McOrmond of WallachBeth, and it has become something of a reunion - many familiar faces, a few new ones, and, most importantly, many close friends. WallachBeth has built a remarkable firm. If you need help executing a trade, they are exceptional. If you need clarity on a complex investment product, industry trends, or where the world may be heading with something as complex as blockchain and tokenization, you have a lifeline to an experienced friend just a phone call away.

There is much to share from the week, but let’s begin with Goldman Sachs Chief Investment Strategist John Tousley. He offered an insight I had not previously considered, one he described as “Secretariat by 31 lengths.” I’ll do my best to highlight the key points from his presentation, and you’ll soon understand why one of the greatest racehorses of all time provides such a fitting metaphor for today’s global financial landscape.

Head up. Big heart. Lights on. Grab that coffee and let’s go!

On My Radar: The Dollar, “Secretariat by 31 Lenghts”

John Tousley, Goldman Sachs – Potential Energy Versus Kinetic Energy

Personal Note: Photo’s From Back Country

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

John Tousley, Goldman Sachs – Potential Energy Versus Kinetic Energy

Tousley framed today’s environment through a simple physics analogy: potential energy versus kinetic energy. Potential energy is stored risk - things that could happen. Kinetic energy is what is actually moving.

We live in a world overflowing with potential risks: wars, elections, debt, technological disruption, geopolitical tensions. But Tousley argues investors often treat these risks as inevitable outcomes rather than possibilities. I think he is right about that.

His preferred image is not a roller coaster about to plunge, but a shelf filled with books. Any one of them could fall. Most won’t, unless something pushes them.

Markets, he says, do not trade on fear. They trade on motion.

And right now, the forces in motion remain constructive.

Goldman expects U.S. growth near 2.9%, inflation moderating from the current 2.8% down to roughly 2%, a Federal Reserve moving from restrictive toward neutral with two to three rate cuts more likely that one to two cuts, and corporate earnings growth around 12%. That combination: an expanding economy, easing policy, cooling inflation, and rising profits has historically supported equities even in turbulent times.

Valuations, while elevated, are not viewed as an imminent danger. Today’s market consists of higher-margin, less cyclical companies than in past decades, allowing valuations to remain higher without necessarily implying a bubble. My view on valuations differs but it’s important to listen to Tousley’s point. He adds, expensive markets can stay expensive and still produce strong returns -as long as growth and earnings persist. True.

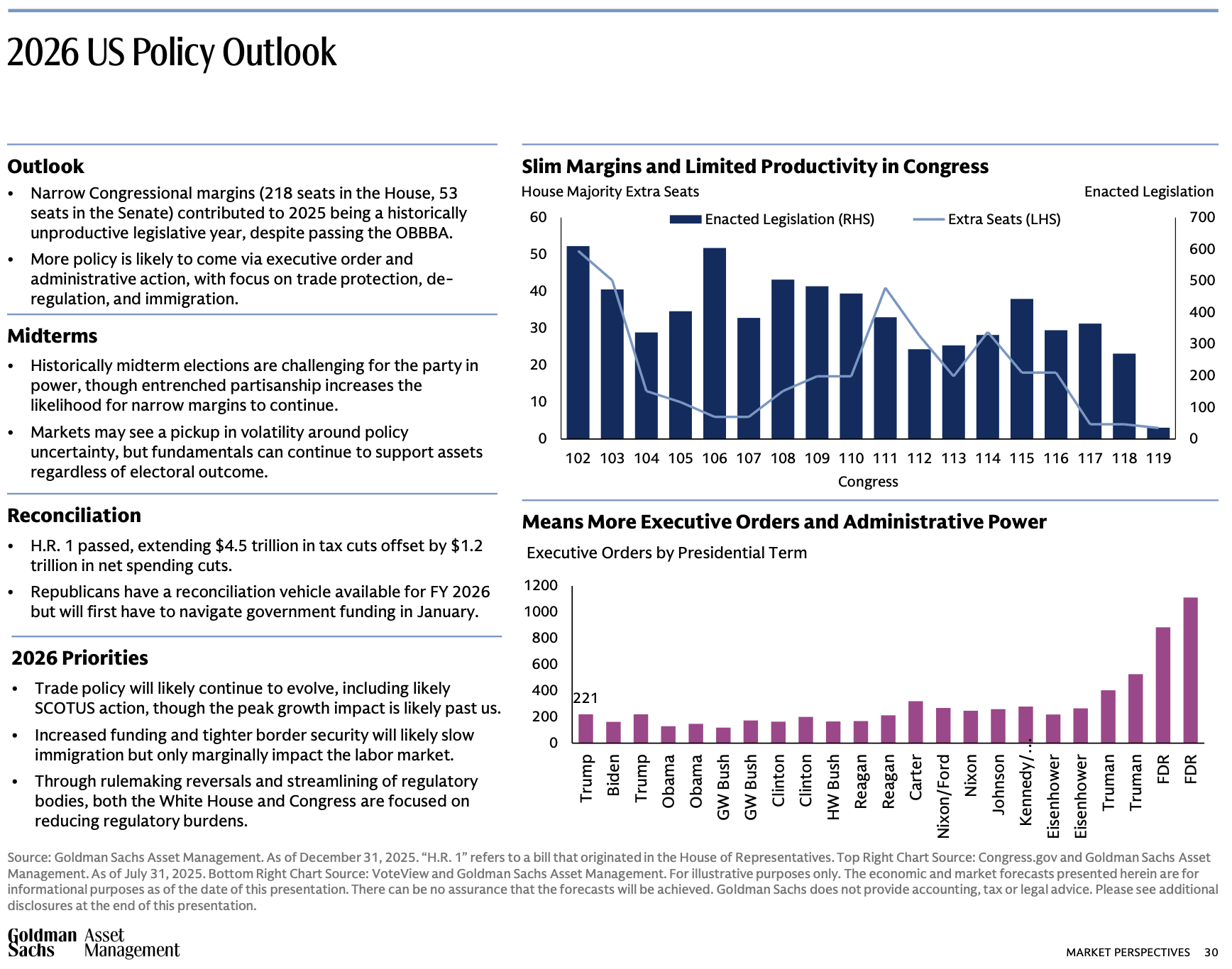

Tousley also downplayed the market impact of next November’s midterm elections. He believes the democrats take the house and sees 13 seats up for grabs. Quoting John,

“The President currently controls both the Senate and the House with basically three seats each. What does he get done in Congress with that three-seat advantage? Nothing, because you always lose three senators and three members of the House representatives on any legislation. And so thin margins make it really difficult to pass legislation because there's so much ideology within the parties. I've got Elizabeth Warren way the hell over here (on the far left) and she's got to find a piece of legislation that Mark Kelly, a kind of a moderate (democrat) from Arizona likes. That's the hard part of legislating when you control the chamber, just getting your own party in line.

So, here's where we're going to end up. We're probably going to end up with everybody declaring victory. Democrats will probably take the House and they'll claim they were given a certain mandate. The Republicans will say, well, you should clobber us but you only got 13 seats. Clearly, you don't have a mandate. You underperformed history.

What I’m saying is that everyone's going to be able to declare victory. But here's what you end up on the top chart is the light blue line, extend margins of leadership. The dark blue bar is what Congress got done? And if you look, the 119th Congress got 41 pieces of legislation done. That is the least amount of legislation done since the Congress in World War II.

So chances are in December, we're looking at a world that feels pretty dysfunctional. No different then today. And the bottom chart shows that means if the President doesn't have a functional Congress, they will operate in the world of executive order and executive action.

So, President Trump in his first year has executed, I think, 221 executive orders. These are not laws. These are enforcements or lack of enforcement policies for existing laws. They all end up in court. Half of them get thrown out.”

Here is the chart Tousley referenced:

Source: X, @RayDalio

The great Abraham Lincoln! On gold, he sees a compelling multi-year case driven by central bank diversification, persistent deficits, and diminished confidence in bonds as volatility hedges. Though he cautions the asset remains inherently volatile.

Where he becomes far less sanguine is government debt. I raised my hand and asked directly about government budget deficits of $1.9 trillion, debt exceeding $38 trillion, Social Security running out of money in 2032, and the prospect of forever money printing. And what does this all mean in terms of inflation and the long end of the yield curve?

He answered bluntly: “Bad, bad, bad, bad and bad.”

Adding:

“So, all right, this chart is brutal to look at, and I just need you to give me a minute because of what we worry about. So, if I was to say the books on the shelf that we worry about, I worry about the labor market because the labor market is absolute. And we could stay right where we are. I would use the analogy with the edge of the cliff and we can see where we are and enjoy the view and be just fine. But the next leg lower, if we see a material drop in the demand for labor, whether that's AI or just uncertainty or a global event, the next leg lower in the labor market, there's no more cushion in the economy to absorb it. I start to see the unemployment rate really go up.”

“So we're precarious.

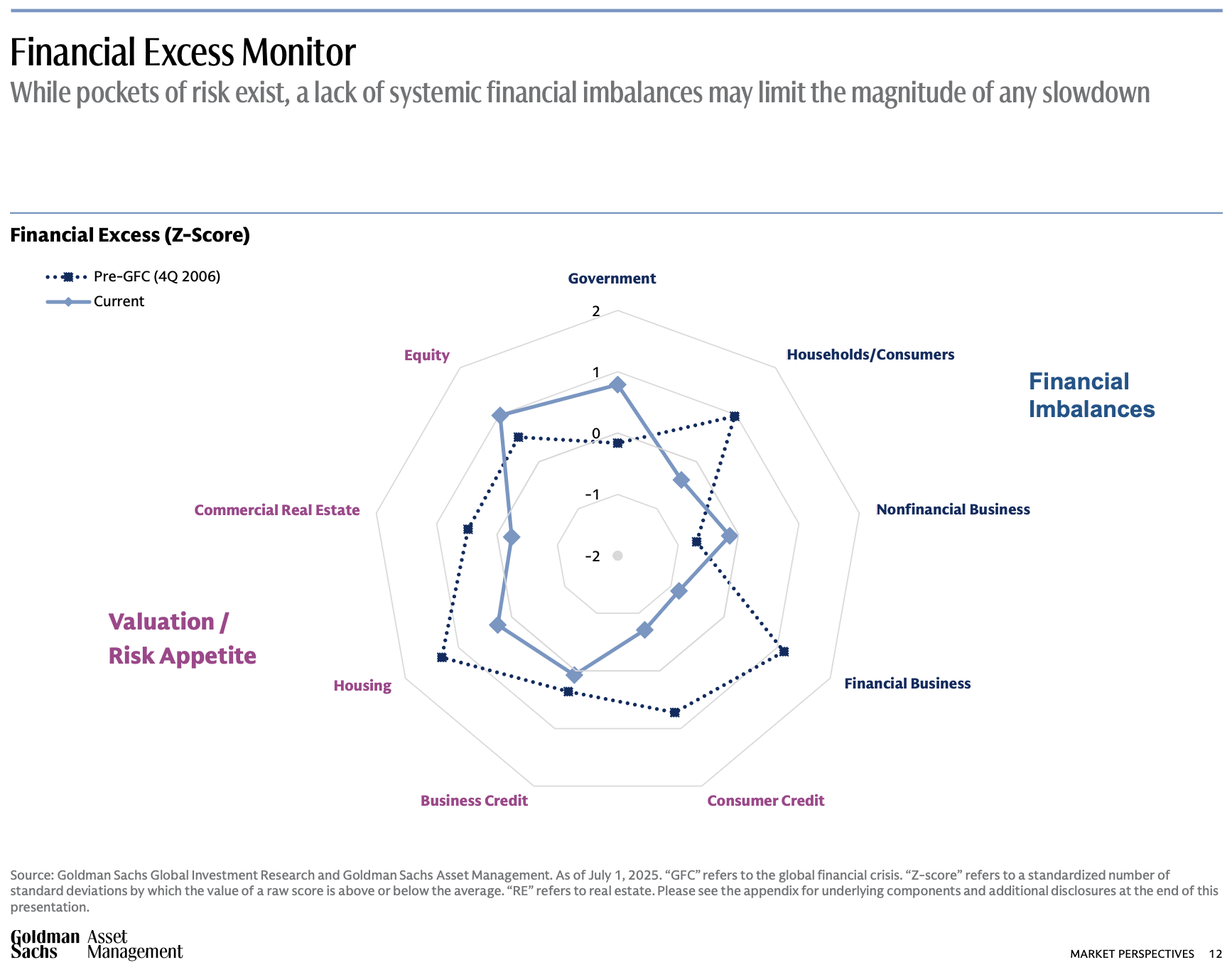

The other area we worry about is things: recessions, financial events, and financial bubbles. So, the second book on the shelf is: Do we have a financial bubble? And this next chart measures financial bubbles. The further out your dot, the more risk you have from 12 o'clock at the top, where it's government, to 4 o'clock, which is the amount of leverage in the system.”

SB here: The light blue boxes (lines) are our current conditions. The problem areas are government debt and equity valuations.

Rising interest costs crowd out productive investment and represent a long-term drag on growth. Yet he does not foresee an imminent crisis. And this is where he made me think deeply about my own forward thesis. He does not see an imminent crisis because of the unique position of the U.S. dollar.

The Dollar: “Secretariat by 31 Lengths”

Tousley compared the dollar’s dominance to Secretariat’s legendary Belmont Stakes victory, winning by 31 lengths with no rival even visible down the stretch. When crossing the finish line, Secretariat’s jockey, Ron Turcotte, looked back and saw no other horse in sight.

Despite frequent discussions of “de-dollarization,” global reserve allocations have shifted only modestly:

Central bank balance sheets’ dollar reserves have fallen from ~58% to 56% over 3+ years.

The Euro is just ~16%, and

The Renminbi is ~2%

In other words, the world may want alternatives, but there is no other horse in sight.

Reserve currencies require not just economic size but deep, liquid capital markets and fully convertible financial systems. No other country currently offers a bond market capable of absorbing global savings at scale. As Tousley put it, it’s an interesting conversation but not a practical transition anytime soon.

Tousley said,

“The dollar is the reserve currency because we are, it doesn't feel like it, but we are the most politically stable country on the planet. We are the largest economy. We are the best growing economy. So not only are we the largest, but we’re also more dynamic, we're more diversified, we are strong. We're less cyclical. It's harder to put our economy in recessions. But here's the stem of sauce to the dollar. There are few challenges. If you want to be the reserve currency. President Xi of China two weeks ago said, hey, we want to become more plus the dollar, and we'll become a reserve currency. Oh, will you? Well, you better be fully convertible. You better let everybody on the planet come in and out of your currency without any cost or regulation whatsoever. You want to do that in China. Xi will say, whoa, we don't want that. And if you were fully convertible, the remedy goes to $11, not $7. And their manufacturing competitiveness completely disappears.”

He added,

“This structural reality allows the U.S. to sustain deficits far longer than other nations without triggering a funding crisis.”

My view has been and remains that we are on a path towards more money printing and the by product is inflation. On paper, very good for certain asset holders. The wealthy will get wealthier. An awful result for the majority of the population. The very large BUT in the equation is AI. As AI may likely prove to be a massively deflationary force.

As an aside: If you missed the movie, it’s fantastic. It was about Secretariat’s legendary 31-length Belmont Stakes victory in 1973 was ridden by jockey Ron Turcotte, whose calm, hands-low style allowed the great horse to run freely in what remains one of the most dominant performances in sports history.

Debt: Tousley vs. Dalio Stage 6 vs. Blumenthal

The divergence in macro thinking is striking.

Tousley: Sees a Long-Term Problem, Not an Immediate Crisis. The system bends but does not break, at least not yet.

Debt trajectory is unsustainable but manageable for now

Dollar dominance provides extraordinary funding capacity

Lack of credible alternatives limits risk of sudden crisis

Productivity gains (especially AI) may offset fiscal drag

Systemic financial imbalances are currently limited

Dalio: Stage 6, Late-Cycle Warning

I wrote about Ray Dalio last week in OMR: Big Cycle Stage 6

sees the debt problem as central to the transition into Stage 6 of the Big Cycle:

Debt levels approaching limits of sustainability

Rising interest burdens constrain policy flexibility

Increasing reliance on monetary financing

Risk of currency debasement, internal and geopolitical conflict

Potential restructuring of the global monetary order

Core view: Debt dynamics ultimately drive regime change.

Blumenthal View: Fiscal Dominance & Structural Risk

My framework tends to bridge the two:

Debt service costs increasingly crowd out productive spending

Persistent deficits risk entrenching higher inflation and rates

Fiscal dominance limits central bank independence

Long-term real returns may suffer even without crisis

Market stability today does not negate future instability

I see irresponsible legislators, future interest rate controls, continued money printing, and waves of inflation

What struck a light in me about Tousley’s presentation was the dollar’s dominance. Secretariat by 31 lengths. I think he is right. We’ll have events but no collaspe and we are more likely to see a prolonged era of fiscal dominance, financial repression for the masses, higher volatility, and lower real growth. The wild card is AI - a legitimate game changer.

Bottom Line

Tousley offers a compelling counterweight to the dominant doom narrative. The global system faces serious long-term challenges, particularly around debt, demographics, and geopolitics. But in the near term, the forces actually driving markets like growth, earnings, Fed policy, and seemingly unending liquidity, remain positive. Buy good businesses with low debt, high free cash flow, and high and growing dividends. Gold, copper, commodities, infrastructure, and energy look attractive to me.

Ray Dalio warns the world order is fracturing. Tousley argues the engine has a few kinks, but it is still running smoothly. For now, both can be true at the same time.

The lesson for investors is not to ignore risks but to distinguish between what is possible and what is already unfolding.

For now, the books remain on the shelf. Keep your eye on the 10-year Treasury. If the bond vigilantes revolt, this is a book pusher.

You can find John Tousley’s presentation deck here. Worth your review.

Follow me on X @SBlumenthalCMG

The views are Steve Blumenthal’s and subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. See important CMG disclosures below.

If you like what you are reading, click on the following link.

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: February 26, 2026 Update

Trade Signals Sections:

Market Commentary

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

Why Trend Following Matters

Not a recommendation for you to buy or sell any security. For information purposes only. Outlook and viewpoints are subject to change at a moment's notice. This material is for discussion purposes and does not give you specific advice. Please discuss needs, goals, time horizons, and risk tolerances with your advisor. Important disclosures.Not a recommendation for you to buy or sell any security. For information purposes only. Outlook and viewpoints are subject to change at a moment's notice. This material is for discussion purposes and does not give you specific advice. Please discuss needs, goals, time horizons, and risk tolerances with your advisor.

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Photo’s From the Back Country

“A pair of skis are the ultimate transportation to freedom.” The late great, Warren Miller

Andy began the conference with a Ted Talk presentation about life, giving, and enjoying the path. If you are reading this missive, you are likely successful and driven. His message is to make sure you stop, reflect, and spend time with your loved ones and friends. His bigger advice is, “remeber to be an advocate and a champion for the people in your life.”

The following are a few pictures from the back country.

What a playground!

Snow cat, powder skiing team, Andy… great friends.

Steve and Andy

Max C and Steve

Brian S on left

Will and Clayton

Park City Snow Cats - also Retts Cabin from Yellowstone. Team on steps with cold beer!

Learned a lot, had great fun - checking in filled up and happy. Hope you are doing something that lifts you as well!

Thank you for spending time with me each week.

Warm regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.