On My Radar: 1999?

July 10, 2026

By Steve Blumenthal

“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.”

- Sir John Templeton

I spoke with my dear friend, John Mauldin, this morning. I've been reading John's weekly letter every Saturday for more than twenty-five years. That's where my familiar phrase, "Grab your coffee and find your favorite chair," came from. It's exactly what I do each weekend. Up early, soft music, a hot cup of coffee, and John's latest thoughts. One of several research letters to start the day.

John and I had business to discuss, but since today is writing day, we spent most of our time talking about the week's events instead. We laughed about how unforgiving Fridays can be for those of us who write, especially on the days when the words simply refuse to cooperate.

One development stood out above others this week. Fed Chairman Kevin Warsh announced the leaders of his five new task forces, and the names tell us a great deal about the direction of the Fed. Game theory hats on! There aren't many softies on the list. My takeaway is that this looks less like a return to the Powell era of stepping in quickly to support markets and more like a Fed that is willing to tolerate greater market pain if it believes doing so serves its longer-term objectives. Time will tell, but I think it's an important signal.

So grab your coffee, find your favorite chair, and let’s go. I asked John to share his thoughts on the appointments, and with his permission, I'm sharing them with you below.

And please don't miss this week's personal section. We'll take a short walk through Old City Philadelphia, where our nation was born. I hope you enjoy the shared photos and the history.

On My Radar:

Personal Note: Independence Hall, Betsy Ross, and Ben Franklin

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

People As Policy

From John,

“Next month I will begin my 27th year of writing this letter. The way I write, how I come up with topics, when I write have all changed over time. But one thing is consistent: when I sit down to write there is a blank screen. Some weeks topics are obvious. Some weeks I scramble as the fear of a blank screen forces me to just start writing. On a few occasions those are my better pieces. Often, well let’s just say that those letters will make the top of the list.

This week a number of articles caught my attention. The only thing that ties them together is the impact of the US and global economy. Economic anomalies: things we were not looking for but show up and forces to pay attention. Today in the summer heat, let’s take a look at a few of them.”

Some quick background on where John is going. At the beginning of his term, the new Federal Reserve Chairman, Kevin Warsh, said he would create 5 task forces to address various topics. Yesterday, this: Federal Reserve Board - Federal Reserve announces the leadership and objectives of its task forces to advance the conduct of monetary policy:

The following are the five task forces with appointed leaders:

Communications: Review how the Federal Reserve conveys policy deliberations and decisions amid uncertainty.

Peter R. Fisher, professor of practice, Foster School of Business, University of Washington

Arminio Fraga, founder and chairman, Gávea Investimentos; former president, Central Bank of Brazil

Mervyn King, former governor, Bank of England

Balance Sheet Policy: Examine the costs, benefits, and institutional implications of the Federal Reserve's current balance sheet regime.

Karen Dynan, professor of economics, Harvard University

Raghuram Rajan, professor of finance, University of Chicago Booth School of Business; former governor, Reserve Bank of India

Jeremy Stein, professor of economics, Harvard University; former governor, Federal Reserve Board

Data: Improve the quality and timeliness of real economic signals that inform the Federal Reserve's policy judgments.

Raj Chetty, professor of economics, Harvard University

Doug McMillon, former president and CEO, Walmart Inc.

Kevin Murphy, professor of economics, University of Chicago

Productivity and Jobs: Assess the economic impact of new general-purpose technologies, including artificial intelligence, to inform the Federal Reserve's policy judgments.

Marc Andreessen, cofounder and general partner, Andreessen Horowitz

Charles I. Jones, professor of economics, Stanford University, currently on leave at Anthropic

Asha Sharma, executive vice president and XBOX CEO, Microsoft Corp.

Inflation Frameworks: Revisit how the Federal Reserve understands and responds to the drivers of inflation.

Greg Mankiw, professor of economics, Harvard University; former chairman, Council of Economic Advisers

Thomas Sargent, professor of economics, New York University; Nobel laureate

William White, senior fellow, C.D. Howe Institute; former economic adviser, Bank for International Settlements

Again from John,

“The new Federal Reserve Chairman, Kevin Warsh, announced at the beginning of his term that he would create 5 taskforces to deal with various topics:

Communications: Warsh is clearly on record as not being in favor of the forward guidance to the extent that it developed under Bernanke, Yellen and Powell. He did not offer a dot plot in his first meeting. He wants a complete rethink.

Balance sheet policy: Warsh would like to reduce the balance sheet and shorten the duration of his portfolio.

Improving data: we all know that the data the Federal Reserve gets from the BLS and other government agencies is outdated, and the methodologies are suspect in a modern era. Should the Fed collect its own data or work with the government agencies to improve their methodology? I have talked about this in the past and there are ways to do this but it is not simply tinkering around the edges of data collection. There needs to be wholesale changes and modernization.

Productivity and jobs: arguably, this (employment) is one of the assignments that Congress has given to the Fed, but the linkage between monetary policy and jobs is not clear.

The most important task force? In my mind it is the one on inflation. Warsh wants to revisit how the Federal Reserve understands and responds to the drivers of inflation.

When I first read about the Task Forces, I was admittedly a little skeptical. Another blue-ribbon committee making suggestions that will be thrown into the mind-numbing bureaucratic maw, chewed up and “processed” and passed through the system ending up as the same old… stuff.

Please note: I am a huge fan of Kevin Warsh. He is clearly changing the culture at the Federal Reserve. This is the regime change that not many people are talking about. But as we have found, regime changes are more difficult than simply saying the words.

Then, on Thursday, I looked at the people that he appointed to the task forces. The one that stood out to me immediately was his task force on inflation:

Greg Mankiw, professor of economics, Harvard University; former chairman, Council of Economic Advisers

Thomas Sargent, professor of economics, New York University; Nobel laureate

William White, senior fellow, C.D. Howe Institute; former economic adviser, Bank for International Settlements

Thomas Sargent and Bill White (who is no stranger to my readers and to attendees at the Strategic Investment Conference) are hell on inflation. Bill White, when he was the Chief Economist at the Bank of International Settlements, consistently fought with central banks and governments over inflation. Nobel laureate Tom Sargent is one of the true conservative Nobel laureates and whose research reinforces the points about inflation and fiscal policy, along with a number of other topics. I know both of these gentlemen. Greg Mankiw is a well-known conservative economist at Harvard.

His task force on productivity and jobs? Marc Andreessen (Andreessen Horowitz) and Asha Sharma, executive vice president and XBOX CEO, Microsoft Corp. The one academic, Charles I. Jones, professor of economics, Stanford University, is currently on leave at Anthropic. Three very serious thinkers to understand the impact of AI on jobs and productivity as well as normal business practice. All-Star team.

I do not want to go into the weeds on each task force, but they are all of the same cloth. People with deep understanding of their topics and aware of the need for dramatic change in directions. Clearly, Warsh has been planning this for a very long time.

Warsh, in his speeches and publications, has been very clear that he expects things to change at the Federal Reserve. The people he has appointed to these task forces simply double down on that expectation.

This is a potential major sea change in central bank policy. It is coming at us at the same time as the Japanese central bank is also making changes. The yen is continuing to weaken (finally). The Japanese central bank could raise rates more, which would give strength to the yen but that also has consequences. If the BOJ buys bonds, that will be seen by the market as quantitative easing and inflationary.

What they have elected to do this week is to “encourage” Japanese pension funds to sell foreign government bonds (read US) and buy Japanese bonds. That would both support their bond market, increase the value of the yen and not be a shock to their stock market. Just one fund alone has almost $2 trillion in assets. It is conveniently controlled by the Bank of Japan. What do you do when the boss encourages you to do something? And if you’re an independent Japanese pension fund, when your central bank comes to you making suggestions, what do you do?

This will complicate Chairman Warsh’s life as he needs more buying of US treasuries, not less. This will not happen overnight, but it will be a direction that will work its way through US yields, even if on the margin.

People are policy and the people that Kevin Warsh has put on the committees should send a big signal to the markets. It should also send the same signal to Congress, but they will ignore it until there is a fiscal crisis. Hopefully by the time we have a crisis, Warsh has his team and policies in place to be able to force Congress to deal with their own fiscal dysfunction. It will take a great deal of fortitude and courage, but I believe he is the man for the job.”

SB here - let’s next turn to Jim Grant.

You can subscribe to Thoughts From the Frontline for free here.

Share this letter on X by clicking here.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

If you like what you are reading, click on the link and share it with a friend (it’s free).

CLICK HERE TO SUBSCRIBE TO ON MY RADAR

Jim Grant - Meb Faber

I’ve followed Jim Grant for years and I’m a big fan. I came across Meb Faber’s post about his discussion with Jim, I bookmarked it and later listened to it while driving to and from the office.

Jim shared his views about AI, inflation, private credit, gold, and where he believes the biggest risks lie today. You can find the full YouTube interview here.

Jim Grant has published Grant's Interest Rate Observer since 1983. Few market observers have witnessed as many boom-and-bust cycles or have been as consistent in their views on debt, money, and the Federal Reserve.

Jim is always on my radar. Key takeaways from the podcast:

AI: a Revolutionary Technology... and a Historic Bubble?

Grant believes artificial intelligence will change the world. His concern isn't the technology itself. It's the price investors are paying for it.

He argues today's enthusiasm around AI is even greater than the dot-com bubble of the late 1990s. More dollars are being invested, more leverage is involved, and today's financial system is far more dependent on Federal Reserve support than it was 25 years ago.

To explain his thinking, Grant points to America's railroad boom in the 1870s. Railroads transformed the economy, but investors built far more capacity than was immediately needed. Years of excess investment eventually led to falling prices and disappointing returns.

His concern is that AI could follow a similar path. Tremendous amounts of money are flowing into data centers, chips, and infrastructure. The technology may succeed, but investors may be building far more capacity than demand ultimately requires.

His conclusion is straightforward:

"I think today is one of the greatest bubbles of all time."

Inflation Isn't Just Rising Prices

Grant defines inflation differently from most economists.

Rather than viewing inflation as "too much money chasing too few goods," he sees it simply as too much money being created. (SB here - we’ve been writing about this for some time. Frankly, it is the ‘too much money being created’ part that creates the ‘too much money chasing too few goods.’)

Where that money eventually shows up is impossible to predict. It may drive up the cost of coffee, stocks, Manhattan real estate, farmland, or almost any other asset.

He also reminds investors that not all falling prices are bad.

When technology improves productivity, prices often decline naturally. That happened during the railroad and telegraph expansion of the late 1800s. Consumers benefited enormously.

The dangerous form of deflation occurs when excessive debt begins to unwind. Falling asset prices, combined with excessive leverage, create financial crises because borrowers can no longer service their debts.

Why the Fed Can't Fight Inflation Aggressively

One of Grant's central arguments is that today's financial system simply carries too much debt.

Private equity firms, private credit funds, corporations, homeowners, and many other borrowers built their balance sheets during years when interest rates were close to zero.

Those same borrowers now face refinancing at much higher interest rates.

Grant believes this leaves the Federal Reserve with a difficult choice. It can raise rates enough to fight inflation, but doing so risks creating significant financial stress.

In his view, the Fed has an unofficial fourth mandate beyond inflation, employment, and financial conditions: don't break the financial system.

(SB here: I believe Jim is spot on. Individuals’ ownership of equities has grown so large that the stock market has come to dominate the economy. Confidence and consumer spending are tethered to a stable stock market. Rising interest rates raise the cost of money and reduce profits. That’s the pickle Warsh’s Fed is in. The key to the economy is the stock market. The key to the stock market is the bond market. The key to the bond market is the level of interest rates. The Fed determines the short end; the market determines the long end. What’s different this time is that we sit at the end of an 80-year debt accumulation cycle. Stay laser-focused on the 10-year Treasury yield.)

That reality limits how aggressively policymakers can respond if inflation begins accelerating again.

Private Credit Deserves More Attention

Grant also expressed concern about the rapid growth of private credit.

He notes that roughly one-third of the approximately $6 trillion held by life insurance companies is now invested in private credit strategies.

His concern isn't necessarily that private credit itself is dangerous. Rather, he believes it receives far less scrutiny than traditional bank lending or public bond markets.

He compares today's environment to the years leading up to the 2008 financial crisis, when increasingly complex credit products grew rapidly without investors fully understanding the risks.

Banks have stepped back because of tighter regulation, and private lenders have eagerly filled the gap.

(SB here: we talk to specialty lenders all the time. The managers we know are savvy and diligent in their underwriting. For borrowers, money has been easy to find. There are problem loans and aggressive lenders for sure. The key is the collateral, loan structure, and standing in the capital stack. Yes, there will be problems. But the fear of private credit is way overblown, in my view. And I’ll add that there currently remains an abundance of liquidity. Something we monitor closely. The key to the equation is the cost of money, and that is determined by the level of interest rates.)

His View of the Federal Reserve

Grant has long favored a much smaller role for the Federal Reserve.

He believes Chairman Jerome Powell began his career with a healthy appreciation for leverage and financial risk but gradually adopted the institution's prevailing mindset.

Grant is particularly critical of the Fed's long-standing 2% inflation target, arguing that persistent inflation steadily erodes the purchasing power of savings.

His preferred framework would be a Federal Reserve focused almost exclusively on price stability, with less intervention in financial markets and greater respect for sound money principles.

Why He Continues to Own Gold

Grant has owned gold since 1980.

He doesn't buy gold to generate income. He owns gold as insurance against the gradual loss of purchasing power in paper currencies.

As he puts it, gold is a "conceptual investment in the managed decline of the dollar."

He notes correctly that central banks, particularly in Asia, have become among the largest buyers in this cycle.

While he clearly prefers gold to Bitcoin, he says neither produces income, and both depend largely on what someone else is willing to pay in the future.

Areas That Interest Him

Grant is careful to point out that he is not providing investment advice.

Still, he mentioned several areas his research team finds attractive today:

European banks are trading at low valuations.

A UK-based used car platform that he believes has been unfairly punished by AI fears.

Oil, where he believes the long-term supply-and-demand fundamentals remain favorable.

Markets Have a Way of Humbling Everyone

Grant closed with an important reminder.

He pointed to 1984, when 30-year Treasury bonds briefly yielded nearly 14% while inflation was only around 4%. In hindsight, those bonds became one of the greatest buying opportunities of the past half-century. Almost no one wanted them at the time. What is the equivalent of that today? It is not the bond market.

His favorite lesson comes from the late Richard Russell:

"Markets can do anything."

Grant says both his biggest investing mistake and one of his greatest successes taught him exactly the same lesson: conviction is important, but humility is essential.

Bottom Line

The thread running through Grant's entire interview is debt.

He believes today's economy and financial markets were built during an era of exceptionally low interest rates and abundant liquidity. At the same time, investors are pouring enormous sums into AI infrastructure based on expectations that may prove too optimistic.

If inflation were to reaccelerate, Grant believes the Federal Reserve would have far less flexibility than many investors assume because raising rates aggressively could expose just how dependent the financial system has become on cheap money.

Whether or not you agree with his conclusions, his message is worth considering.

History reminds us that periods of excessive optimism, abundant leverage, and easy money rarely end exactly the way investors expect.

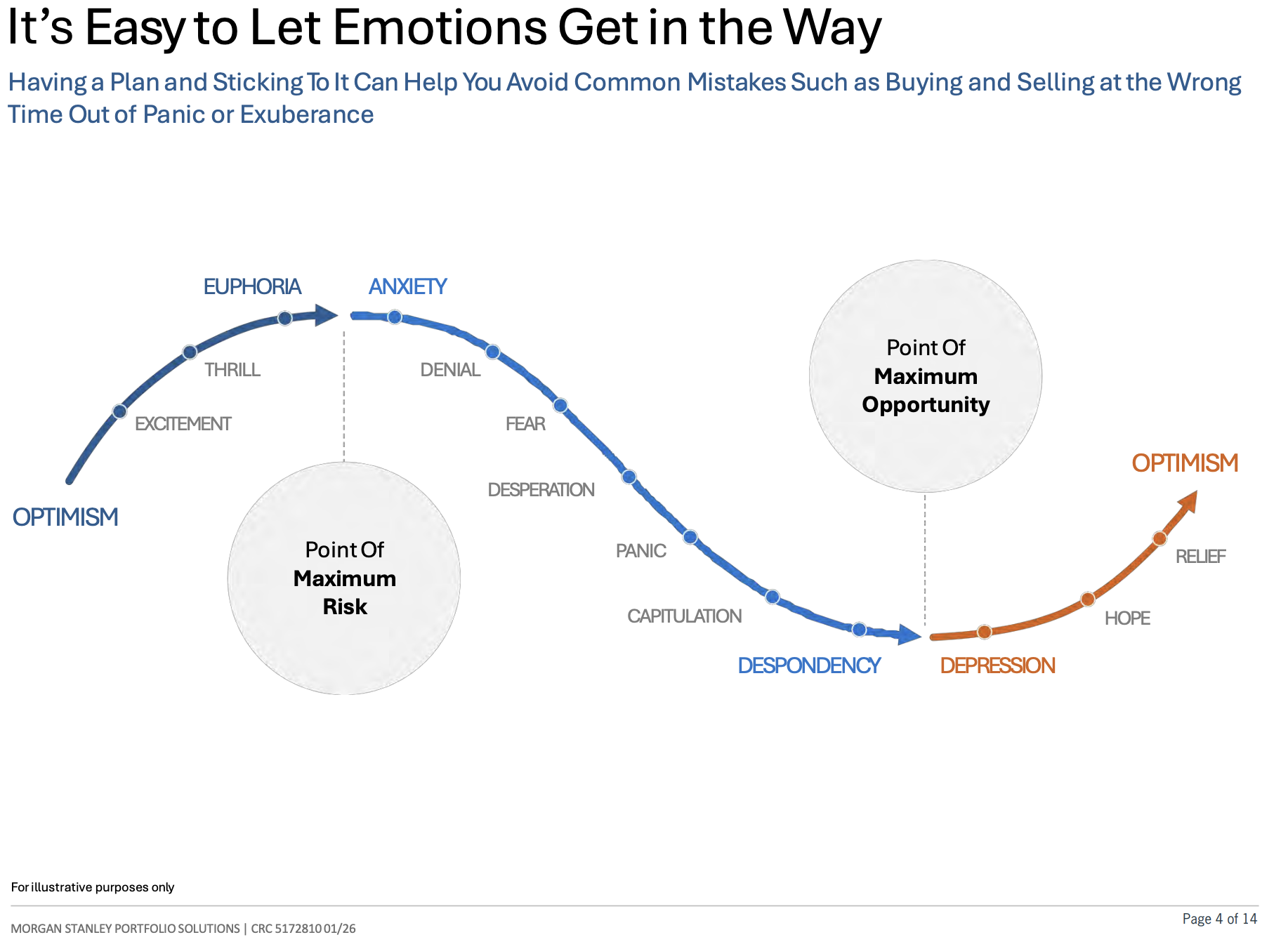

You’ll find several of my consistent themes throughout this interview: debt, overconcentration, leverage, etc. Bubble, yes, and in my view, we have reached a state of euphoria.

The investor's emotional cycle looks like this. 1999? It sure feels like euphoria to me. Buckle up:

Source: Morgan Stanley

The following, adds a little more color:

Source: CMG

You can share this letter on X by clicking here.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: July 10, 2026 Update

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.”

– Charlie Munger

Trade Signals

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

About Trade Signals - Trade Signals is a paid subscription service that posts daily, weekly, and monthly market trends (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Independence Hall, Betsy Ross, and Ben Franklin

Last weekend, Susan and I made the 35-minute commute to the City of Brotherly Love for a Double-Header: America’s 250th Independence Day and the World Cup France vs Paraguay game. The two events came together beautifully, with a renewed love of our country and an appreciation for other countries and their deep patriotism.

It began on Saturday with a delicious lunch at the Spiced Finch, then we jumped on the Broadway subway line to head to the Eagles stadium - correction: The Philadelphia FIFA World Cup Stadium. After a stressful entry with tickets not working, we finally made our way to bask in the mix of fans: USA, Paraguay, France, and many Germans. The 100-degree temps didn’t thwart us from witnessing France try to unlock a deep-lying, physical Paraguayan team. And yes - Mybappe is that great indeed! The fans remind us that love of country is real, it's palpable, and it’s contagious to see their pride.

Back on the subway to Del Friscos and an overnight stay. The next morning, we found a French cafe, a great coffee, and shared an almond croissant. Without a perfect plan for the day, we headed to Old City to be a part of our nation’s birthplace. Having been there many times before, this time just felt different. Amid much turmoil in the world, we were brought back to the incredible history of our country with the bravest of men and women fighting for their own Independence and vision for the future.

We toured Independence Hall, listened to historians tell special stories, and visited the Betsy Ross House. Go if you haven’t. She was a modern woman of her time. Brave, intelligent, resourceful, and an entrepreneur in her own right.

Betsey Ross was personally asked by Washington, in secret, to sew the nation’s first flag. She does this knowing treason is punishable by death if discovered. She was a fierce woman who died at the age of 84, blind from sewing.

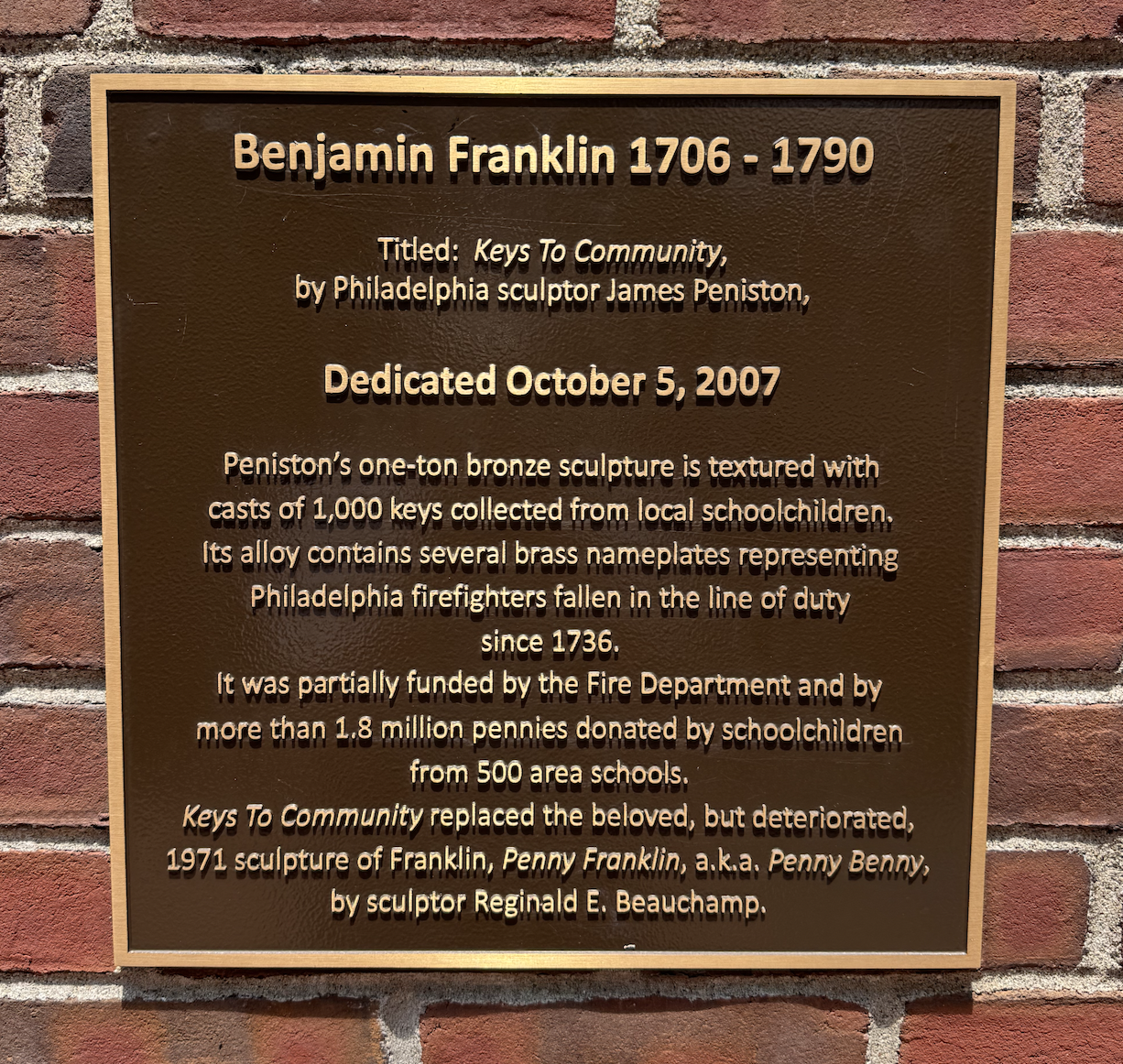

Right next door to the Betsy Ross House, we stumbled upon Ben Franklin’s gravesite and a modern statue of him. See the picture below and be sure to zoom in to see the keys!

Following are a few photos:

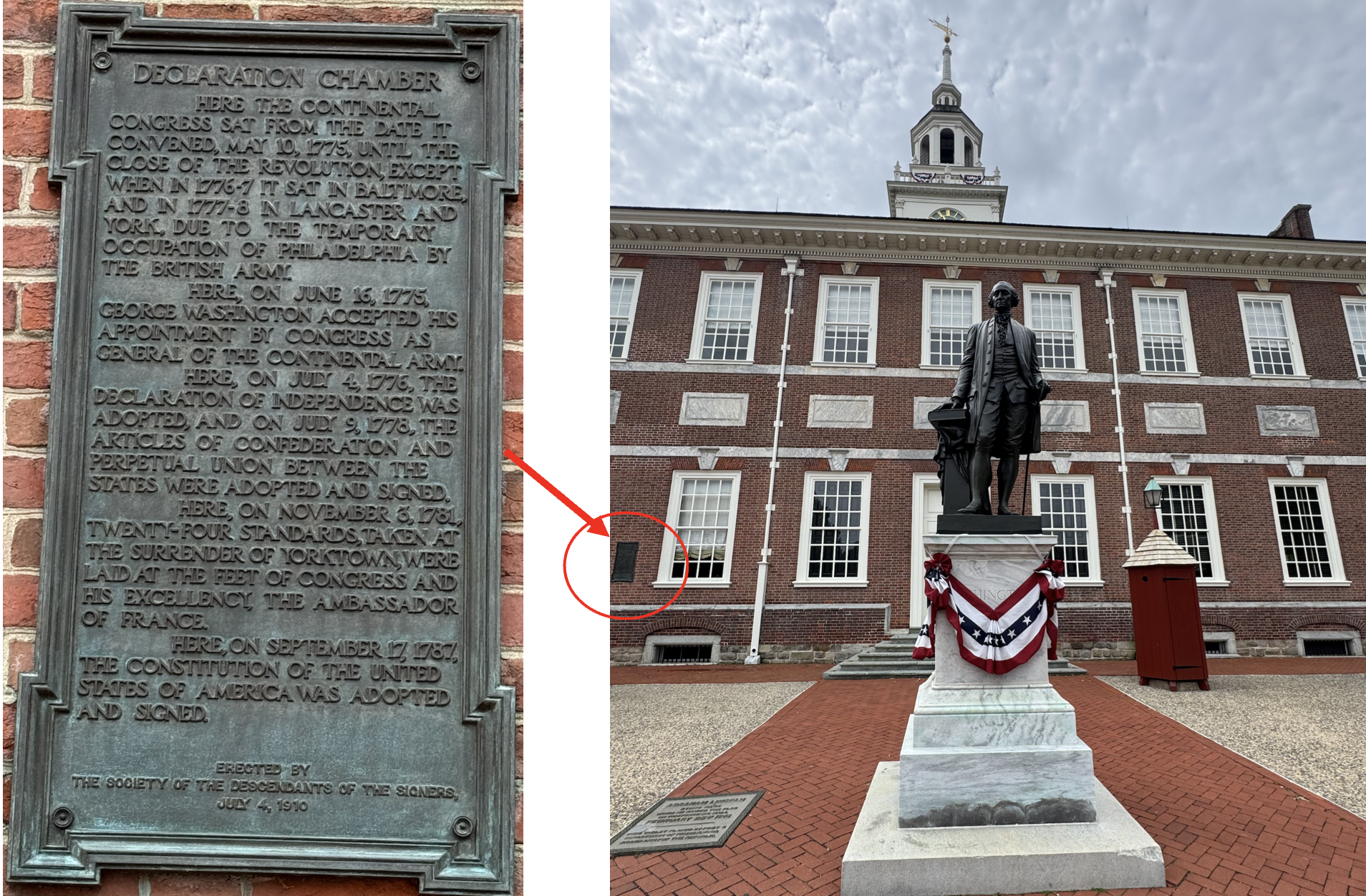

Independence Hall

The Declaration of Independence was adopted here in 1776, and the Constitution was drafted and signed here in 1787. Standing inside is a reminder that liberty and self-government began not on a battlefield, but around a table. This is where America found its voice.

Independence Hall, plaque near entrance (expand screen to read), George Washington

The Betsy Ross House

A glimpse into the life of the woman credited with sewing the first American flag commissioned by General George Washington. The risk was treason and death. Ross worked in secret. The house remains a powerful symbol of the craftsmanship and patriotism woven into the nation's founding. Pictured is a flag in her bedroom. Her grave site sits on the property in front of her house.

Source: Steve’s iPhone

Benjamin Franklin

Franklin gave us the lightning rod and bifocals, then helped secure French support that turned the tide of the Revolutionary War. He believed knowledge, hard work, and civic duty are what build both a life and a republic.

After leaving the Betsy Ross house, en route to the hotel, we passed a church a few blocks away. To our surprise, there was a celebration ceremony taking place. We walked in, Susan had some fun jumping in line (lower left) and we found Ben Franklin’s grave site (note the penny’s). Pretty cool!

Back to the Game, and the World Cup

Outside distractions matter when the pressure is real and cruel. The red-card scandal poked the Belgium bear, and they answered with purpose. Our team didn't deliver, but our opponent was mighty, with a century's head start on us in this beautiful game. Worth noting: just over three months earlier, Belgium beat us 5-2 in an international friendly. They have history.

As a fan, I’m sad to see the USA exit the World Cup. Their style of play was infectious through five games. The excitement across our country and the international fans who traveled here to cheer on their own teams are something to behold.

I believe visitors saw the best of us: our fun, our food, our people, our diversity, our kindness, our welcome. That, too, is authentically American. As a country, we get excited, we get behind the underdog, and we jump in with both feet, no matter how deep the water. May that never change. It's a superpower in its own right.

A French coach, a friend of Susan’s who coaches here often, once told me he loves how Americans always believe something is possible, that there's always hope. That simple thought stays with Susan and me. I bet you feel it too.

As fans, may we find the grace to judge the team less and support its future more. We are playing skilled, smart, and exciting soccer to watch. Closer… we are closer.

Set against the 250th anniversary of our independence, just days behind us, it takes a vision, a belief, and the bravery to see it through, no matter the setbacks.

Let’s keep the hope alive.

I admire these athletes, standing on the world's biggest stage, risking it publicly, chasing a dream bigger than any one of them. May our biggest losses become our greatest teachers.

Memory of a goldfish, goalie Matt Freese. Let it go. Memory of a goldfish!. Fix, improve, and keep moving forward. Never stop.

Always happy to talk soccer, and I welcome your opinions that come with it.

Argentina is looking very good. Messi! Unreal! Norway looks strong, as does France. I have Spain vs Belgium on the TV as I finish writing you. Tomorrow, England plays Norway, and Argentina plays Switzerland. Enjoy the remaining games, and best of luck to your favorite team.

Glasses high, here’s a toast to the courage of our founding fathers. And here’s another toast to one of the greatest sporting events on the planet.

May it bring us closer together.

Every forward.

Enjoy your weekend!

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.