On My Radar: The Match, the Fuse, and 4.50%

July 17, 2026

By Steve Blumenthal

“I am the greatest. I said that even before I knew I was.”

- Muhammad Ali

Miami Beach, February 1964. A loud-mouthed 22-year-old named Cassius Clay climbed into the ring as an 8-to-1 underdog against Sonny Liston, the most feared heavyweight champion of his era. A man who'd flattened his last two opponents in a single round each.

Clay had spent weeks promising he'd dance circles around Liston and predicting, in verse, exactly which round he'd win. Almost nobody believed him. The arena wasn't even full. Six rounds later, Liston slumped over on his stool, and the kid who talked too much became heavyweight champion of the world.

I've been thinking about that fight this week, because we've got a title bout of our own shaping up in Washington.

In one corner: the reigning, undefeated champion, Inflation. We'll call him "Sticky." He is five years into his title reign, still standing after every challenger the Fed has sent at him, and is getting a fresh wind this year from oil, tariffs, and a war in the Strait of Hormuz. Sticky doesn't knock you out. Sticky wears you down, round after round, three-and-a-half-percent at a time.

In the other corner: Kevin Warsh, two months into the job, talking like he's never lost a fight in his life. "Inflation is a choice," he told Congress this week. "The surge of the last five years will be a thing of the past." That's Clay-before-Liston bravado - a challenger nobody in the market fully believes yet, promising a knockout the oddsmakers aren't pricing in.

This week wasn't fight night. It was a pre-fight weigh-in. We had Warsh's testimony on Capitol Hill, followed by a surprise scouting report that landed Tuesday: June's inflation number came in soft, and market odds of a July 29 rate hike collapsed from roughly 40% to under 20% in 48 hours. Warsh didn't blink. "That is not my view," he said, when reporters suggested mission accomplished.

Fight night is July 29. "Float like a butterfly, sting like a bee. The hands can't hit what the eyes can't see."

Grab your coffee. Here's what's on my radar this week.

On My Radar:

Personal Note: The World Cup Final

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

The Match, The Fuse, and 4.50%

Back in April, I told you to watch the 4.50% yield level on the 10-year and that a break above it would be concerning. My guess then was that Trump and Bessent's line in the sand sat at 4.50%, and that a sustained move through it would rattle markets.

We're there.

The 10-year closed Thursday at 4.57%, having touched 4.62% earlier in the week - a seven-week high. Look at the monthly chart below, and you'll see the technical picture agrees with the fundamental one: MACD has turned higher, flashing the same kind of buy signal (for yields, which means a sell signal for bond prices) that has marked every prior cyclical upleg since the secular bond bear began in 2020.

Source: StockCharts.com, CMG Investment Research (annotations)

I've written it before, and I'll write it again: the 10-year yield is the match that lights the fuse. The Treasury cannot afford higher rates. Net interest on the federal debt is now running at ~ 22% of total federal revenue, depending on whose numbers you use and which quarter you measure. Up sharply from the low-teens a few years ago, and headed toward a quarter of every tax dollar collected within the decade if current trends hold. When I wrote in April, that number was closer to 20%. It hasn't gotten better.

A tougher Fed chair just showed up to the fight.

Kevin Warsh was sworn in as Fed Chairman on May 22, and the market got a lesson in being careful what you wish for. Warsh has spent his first two months talking tough. At his debut FOMC meeting on June 17, he held rates steady but removed the easing bias from the statement. Nine of the eighteen participants penciled in a 2026 rate hike. At the ECB's Sintra forum on July 1, his first major public remarks as chair, Warsh said flatly that "prices are too high". The June minutes, released July 8, showed a committee split down the middle on whether to raise rates before year-end.

This week, Warsh testified before the House Financial Services Committee on July 14 and the Senate Banking Committee on July 15, his first semiannual Monetary Policy Report to Congress.

Short summary:

He drew a hard line on inflation: June's better CPI print "isn't mission accomplished," and "inflation is a choice." It was clear that his job was to lower prices. He pledged that the "inflation surge of the last five years will be a thing of the past" if the Fed gets policy right.

Fed funds currently sit at 3.50%–3.75%.

Headline CPI jumped from 2.4% in February to 4.2% in May, largely an oil-price story tied to the disruption in the Strait of Hormuz that I've been tracking here for months. It was a larger-than-expected drop, driven by a 5.7% monthly plunge in energy prices.

We have a new Fed chairman trying to establish inflation-fighting credibility. He is arriving in a supply-side inflation shock he didn't create. He is not a chairman inclined to cut. But will he hike?

Warsh's response, same day: "There might be some that look at this morning's data and say, 'Oh, mission accomplished. Everything is swell.' That is not my view." He pointed out that underlying inflation is still elevated and reiterated that the Fed will stay data-dependent, meeting to meeting. So his stance hasn't shifted - he's still the guy who told Congress "inflation is a choice" and pledged to end it.

Hike odds for July 29 collapsed from roughly 40–46% the week before to about 15–17% right after the CPI print, and CME FedWatch had it down near 10% (90% odds of a hold) as of July 16. On July 15, Poly Market put the odds at under 4%.

The current read is: a July hike is very unlikely now, a hold is the base case, and Warsh's hawkish posture is more about setting up a possible September or year-end move if inflation reaccelerates. The wild card is the Strait of Hormuz. Maybe a rate increase comes this month due to higher oil prices and inflation. Or maybe Warsh moves quickly to make a point. The hands can’t hit what the eyes can’t see.

Following from The Kobeissi Letter:

Source: Polymarket, @KobeissiLetter

Bottom line: I don't know whether Warsh hikes on July 29, but I wouldn’t be surprised. Our prize fighter may need to channel his inner Muhammad Ali, who reportedly said before the Rumble in the Jungle fight against George Foreman, "Suffer now and live the rest of your life as a champion." He must take Sticky down.

But keep in mind that the setup matters more than the single meeting. We have a new Fed chair talking tough on inflation, a 10-year yield that has pushed through the level I flagged as the danger zone in April, a monthly MACD confirming the cyclical trend has turned, and a Treasury that is refinancing trillions of dollars of low-coupon debt into 4%+ paper at the worst possible moment. None of these things fix themselves quickly.

Watch 4.50% not as a level to trade around, but as a tell. As long as the 10-year holds above it, the story is the same one I've been signaling to you since April: the bond market, not the Fed, may end up setting policy.

Sources: On My Radar, April 24, 2026 — "I Hear the Train A-Coming"; Federal Reserve, FOMC statement, June 17, 2026; CNBC, "Markets are set for a much more hawkish Warsh Fed than expected," June 18, 2026; CNBC, "Kevin Warsh declines to hint at July rate decision, but says inflation 'too high,'" July 1, 2026; Yahoo Finance, "Warsh Hawkish Shock: 9 Fed Officials Signal 2026 Rate Hike"; Committee for a Responsible Federal Budget / PGPF, net interest revenue-share estimates. CNBC – June CPI report · CoinDesk – hike odds fall · TechTimes – hike odds collapse · CNBC – July rate hike odds rising (pre-CPI)

Ray Dalio on China

I found this post from Ray informative for understanding China’s hierarchical structure and its history.

And from Ray, “I recently spent a month in Asia, including 10 days in China, where I met with senior policy makers in several countries, and I found that over the past few months, there has been a big shift in the world order. I share my perspective in my latest article.

As always, I welcome your questions and thoughts.”

Click on the image. It’s a thoughtful read.

Source: Ray Dalio, Substack

Share this letter on X by clicking here.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

If you like what you are reading, click on the link and share it with a friend (it’s free).

CLICK HERE TO SUBSCRIBE TO ON MY RADAR

Several Excellent Charts

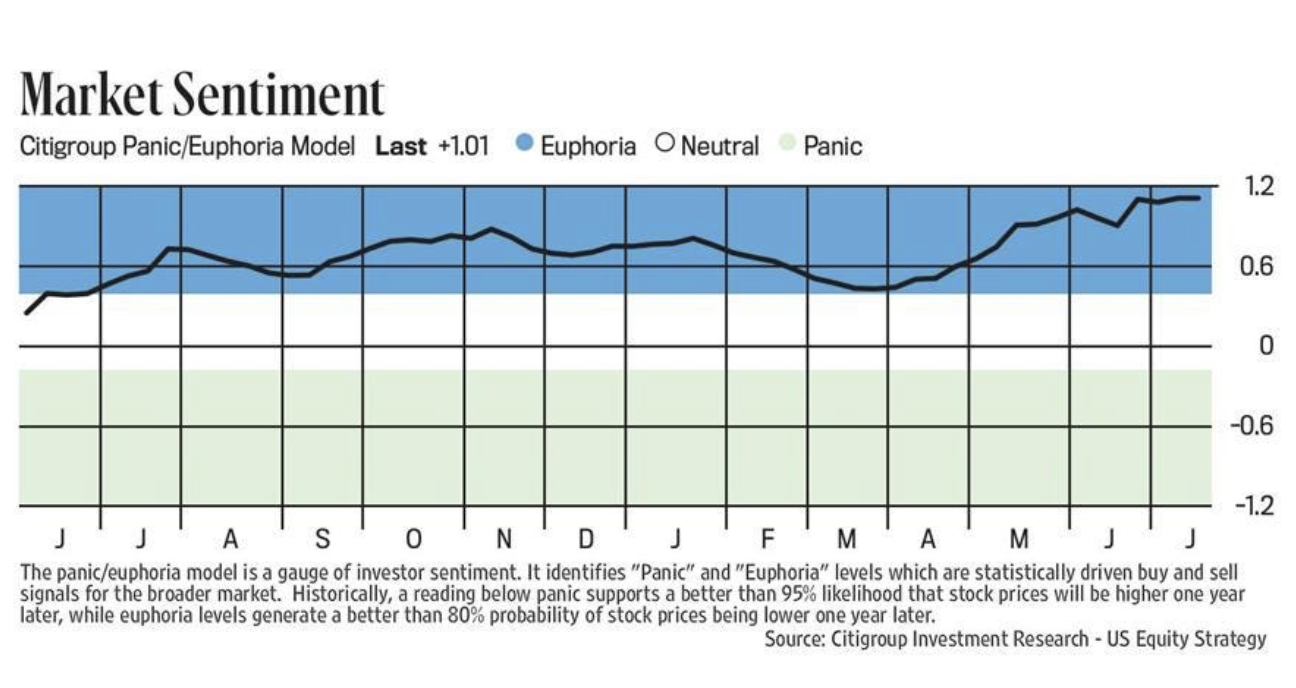

Euphoria

Peter Boockvar's market letter, the Boock Report, hits my inbox several times a day. I wrote about euphoria last week here. The following chart in Peter’s Monday AM post on July 13 jumped out at me. He wrote, “With respect to stock market sentiment, at least by the Citi Panic/Euphoria index, it is back to the recent highs of Euphoria and as a reminder, .41 is threshold so we are well above it.”

Source: Citigroup, Peter Boockvar Boock Report

Leverage

Source: Citadel Securities, GMI, @BobEUnlimited

Historic Bull Market Run

Source: Goldman Sachs, @KobeissiLetter

Price to Sales

Source: Bloomberg, Barchart

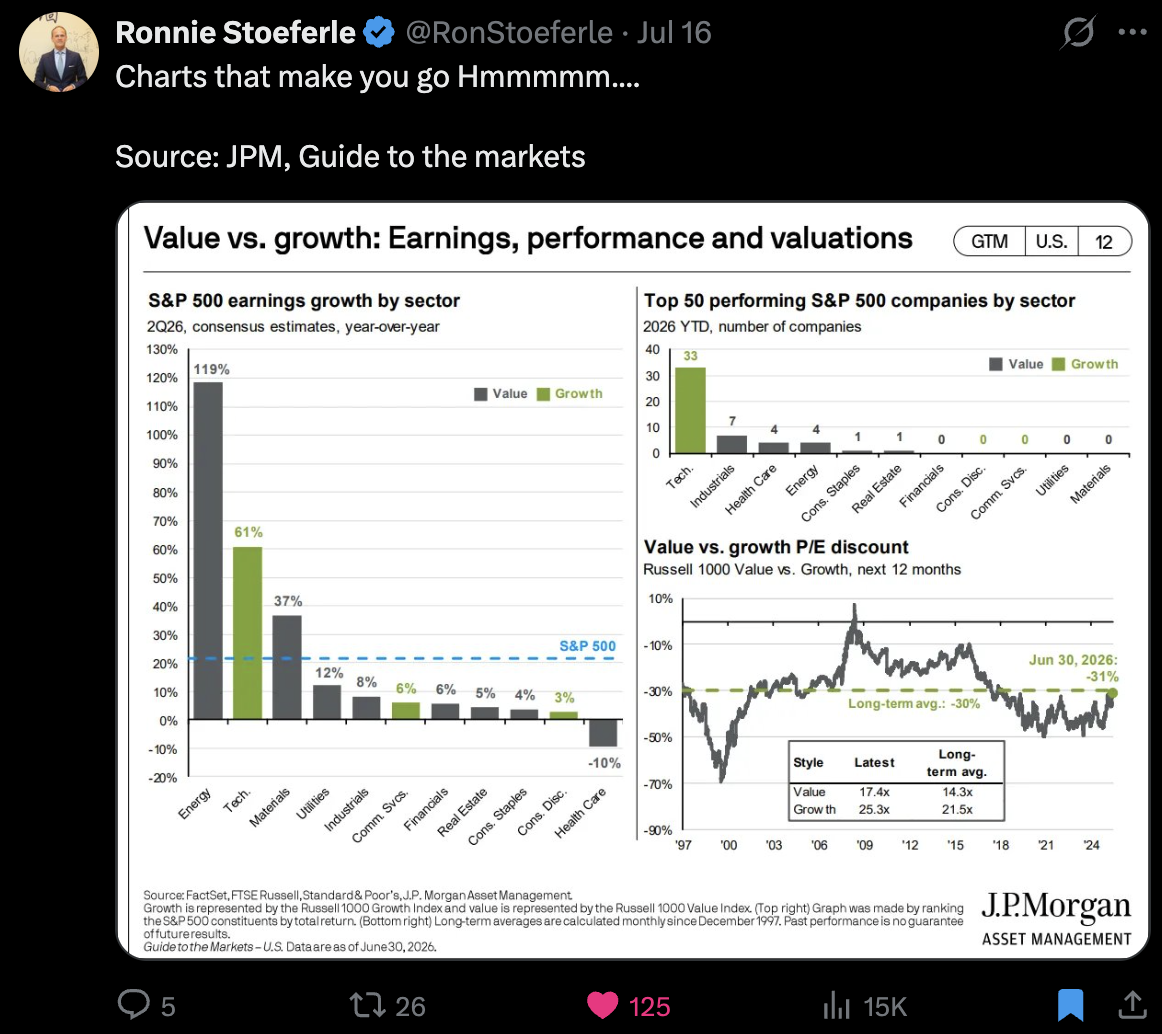

Value vs Growth

Source: Barchart, JP Morgan

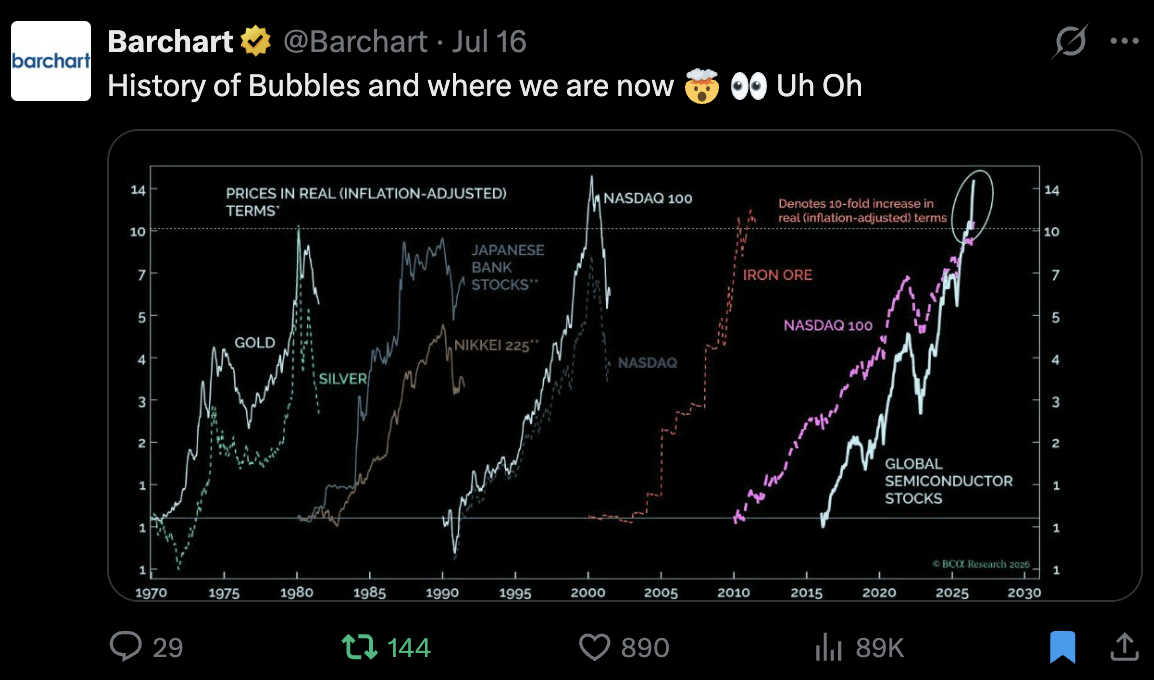

History of Bubbles

Source: @Barchart

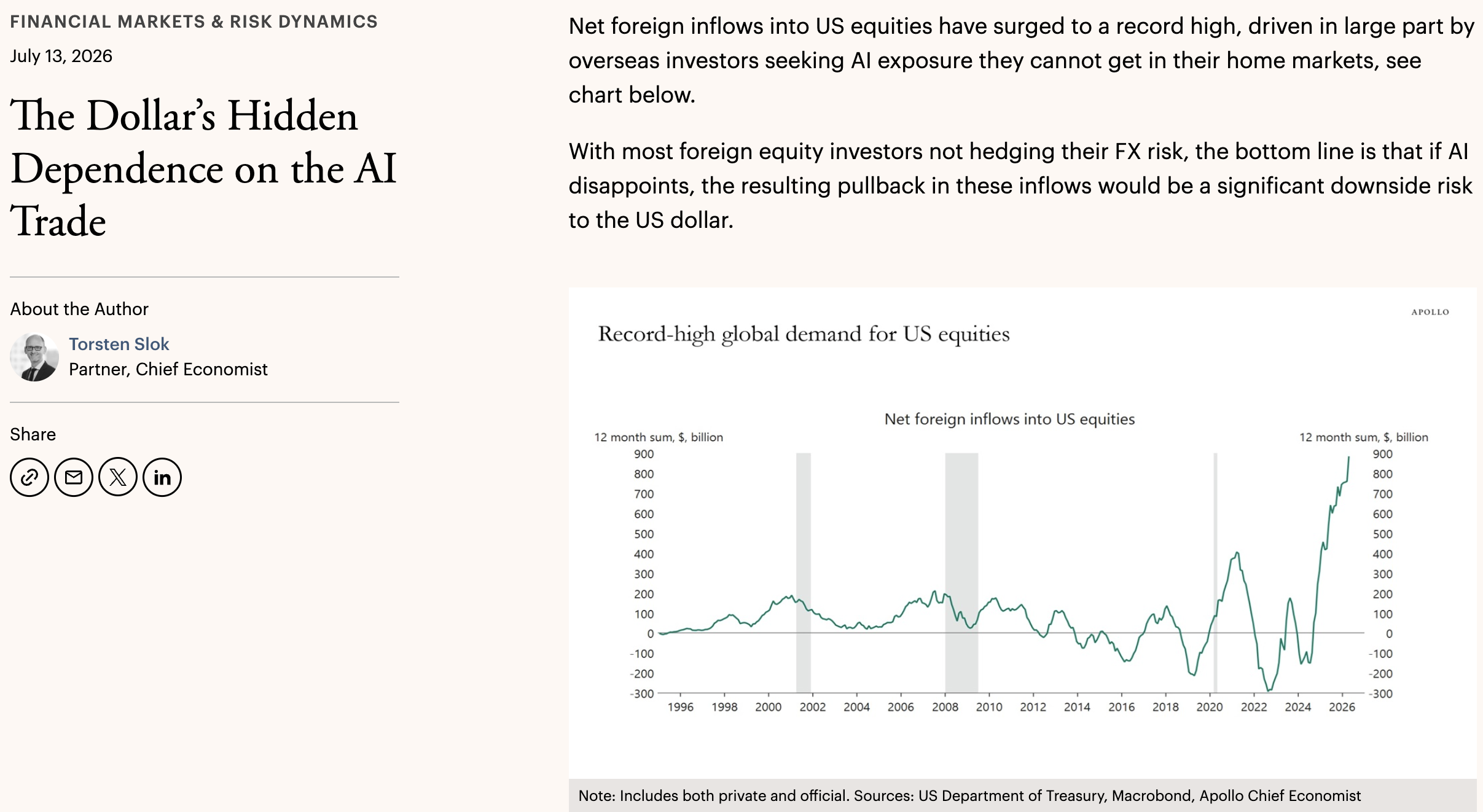

AI

Source: Apollo, Torsten Slok

Share this letter on X by clicking here.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Habib - “Haven’t Got Time for the Pain”

Tying in nicely to the 10-year Treasury watch is a fun start to this morning’s comments, with Carly Simon singing “Haven’t Got Time for the Pain.” Barry and team are not currently worried about inflation. In fact, if the Fed hikes, it could be destructive to the economy, causing a recession. We haven’t got time for the pain!

The wild card on inflation is the war in Iran.

Click on the image to watch the short video.

Source: MBS Highway

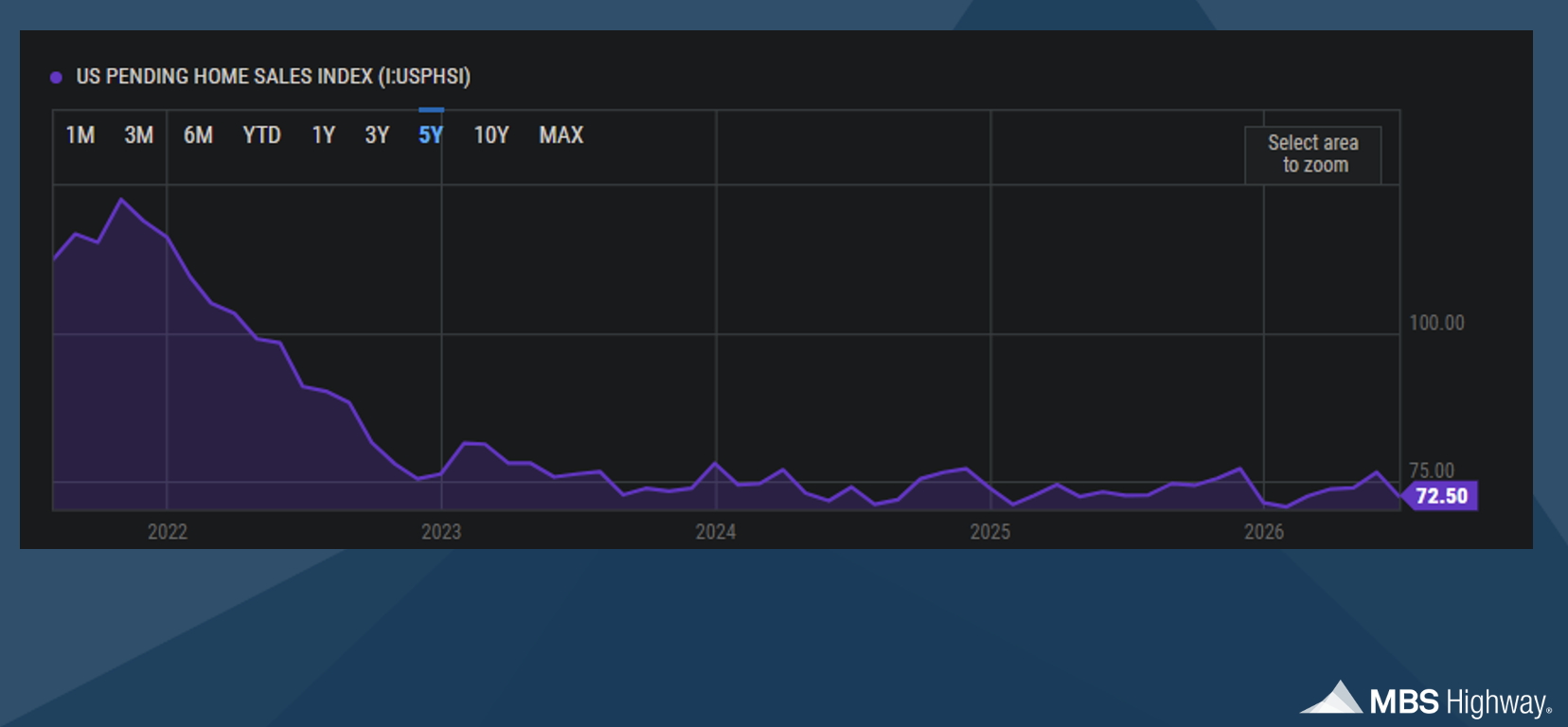

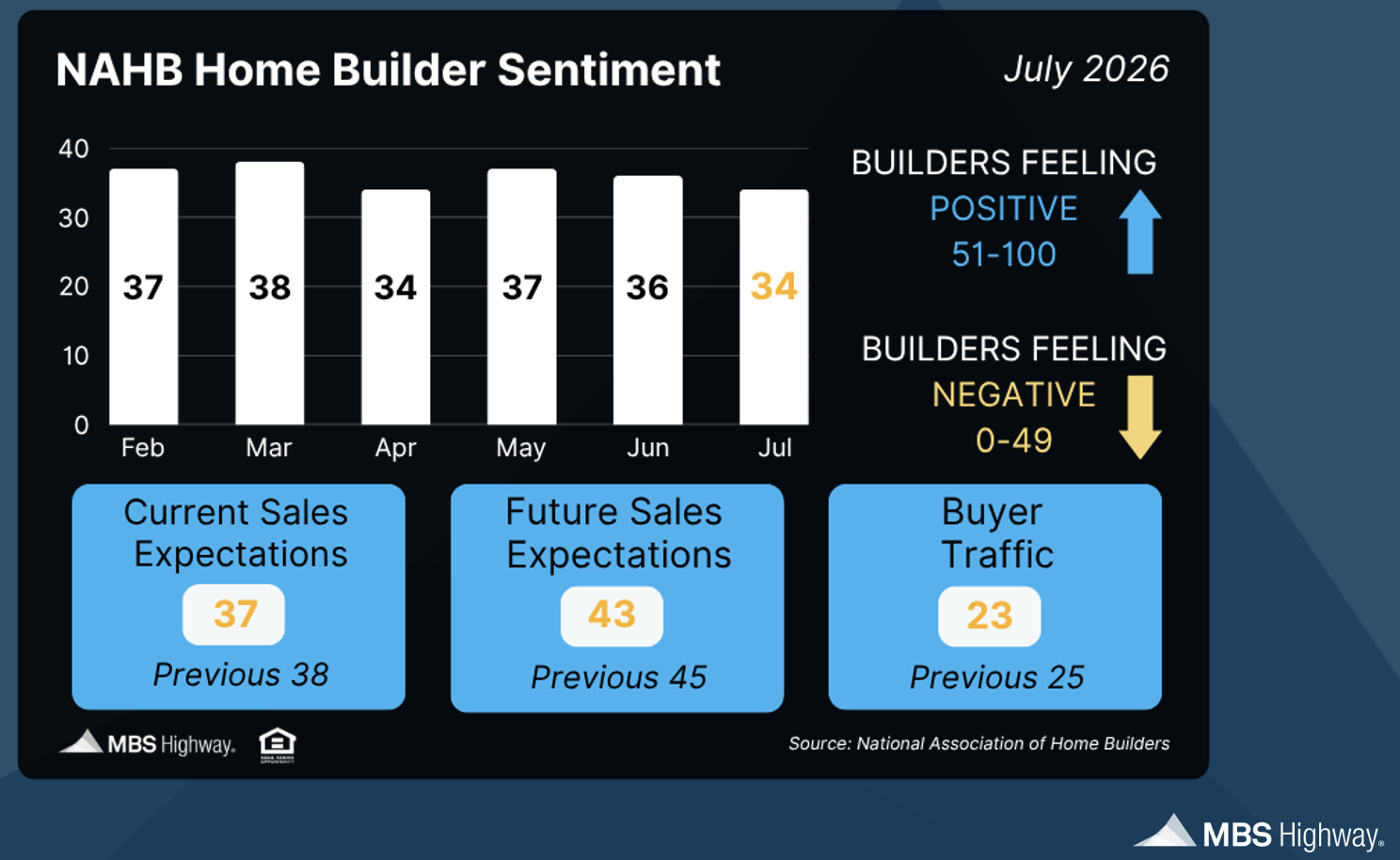

He shared two charts:

Source: MBS Highway

Source: MBS Highway

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: July 16, 2026 Update

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.”

– Charlie Munger

Trade Signals

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

About Trade Signals - Trade Signals is a paid subscription service that posts daily, weekly, and monthly market trends (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: The World Cup Final

"Impossible is not a fact. It's an opinion."

— Muhammad Ali

Tuesday in Dallas, Spain shut the door on France, 2-0. Efficient, technical, businesslike - Spain has looked like the best team in the tournament for a month, and they didn't need drama to prove it again.

Wednesday in Atlanta was a different kind of soccer entirely.

England led 1-0 into the final twenty minutes on an Anthony Gordon goal, and manager Thomas Tuchel made a decision that will be picked apart for years: he pulled a midfielder and pushed on a fourth center-back, switching to a back five and then effectively a back six, dropping everyone back to defend the lead. For a while, it worked. England had just 12% possession over the final half hour.

Lionel Messi had other ideas. Days before the match, Zlatan Ibrahimović, the great Swedish striker turned Fox Sports commentator, a man who has never once undersold himself, went live with a line built for this exact matchup: "England already witnessed the Hand of God. Now they're about to see the Left Foot of God." The hand of god was a nod to Diego Maradona, who beat England 40 years ago at the 1986 World Cup with an illegal punch of a goal that VAR would erase in about four seconds today, followed three minutes later by arguably the greatest solo goal in World Cup history.

Zlatan's point: England was about to witness Messi’s left foot.

Argentina kept crossing, kept probing, and in the 85th minute, Enzo Fernández found a seam and buried a shot from 20 yards to level it. Then, deep into stoppage time, Messi, 39 years old, playing in what may be his last World Cup, served up the cross that Lautaro Martínez headed home for the winner. Two goals, two Messi assists, one impenetrable defense that was not.

Zlatan called it the "Left Foot of God." Messi delivered it with his right foot. Regardless, Messi is a soccer god. My English friends’ hearts are broken. I feel for you. Heads up, what an impressive team and an exciting run.

Coming back to that Ali line above. Tuchel built a wall. Messi treated it like an opinion, not a fact.

The final is Sunday at 3 pm ET at MetLife Stadium: Spain vs. Argentina. Two exciting teams to watch, forward-minded, fast, and skilled. Expect an end-to-end battle. I’m frequently asked who I’d like to win, and I’m really rooting for a great game. I find it hard not to want to pull for Messi, though I’d say Spain looks like the better team.

A tip: for non-soccer people, keep an eye on the shape of the defenses. For most teams, the shape is four defenders, four midfielders, and two attackers up top. Sometimes, it’s four defenders, two defensive midfielders, three offensive midfielders and one striker up top. Don’t just follow the ball. What the defense. Then look for the spaces that the opponent with the ball is trying to get through. By moving the ball, the offense forces the defense to move and hopes to create openings or cause a mistake that leads to a goal-scoring opportunity.

The game is a multi-dimensional chess match. This final is going to be a good one. Enjoy the game!

I’ll be hosting a dinner for clients and OMR readers in Chicago on Wednesday, August 19, 2026. If you are interested in joining, please email Amy@cmgwealth.com to reserve a spot (space is limited).

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.