On My Radar - The Big Risk

May 9, 2025

By Steve Blumenthal

“The US Treasury market – the touchstone of every loan in the world, every insurance policy in the world, every equity valuation in the world – broke last month, and it broke because the full faith and credit of the United States came into question.”

— Ben Hunt, Epsilon Theory

Howard Marks once used a simple metaphor I’ve always liked: imagine a fish bowl filled with raffle tickets, each one representing an investment opportunity. Anyone can reach in and grab one, but not all tickets are created equal.

Some offer strong risk-adjusted returns. Others carry more downside than they appear to. The difference comes down to judgment. The best investors aren't lucky - they’re the ones who consistently select the better tickets by seeing what others miss.

That’s really the heart of investing: in a world where everyone has access, edge comes from thinking clearly, staying patient, and understanding risk better than the crowd.

Risk isn’t something to be avoided entirely - it’s where opportunity lives. As stewards of capital, that’s our (you, me, everyone’s) job: to see the risk and what it makes possible.

The issue isn’t subprime debt this time (like the 2008 Great Financial Crisis); the systemic risk is the $37 trillion and growing U.S. Treasury debt market.

Ben Hunt tells the story in his own powerful way. His piece, published this week, is exceptional. With his permission, I share it with you below.

I’m in Florida for business and writing you early. This afternoon, I spoke with Ben and other subscribers to his research service. The topic was, “What happens when the U.S. is just another country?” I took notes and will share them with you in an upcoming letter.

A lot is coming at us at an accelerating pace. Keep your lights on. Stay sharp. Stay patient. And, of course, grab your coffee and find your favorite chair…

On My Radar:

Our True Enemy Has Yet to Reveal Himself

Trade Signals: Update - May 8, 2025

Personal Note: Happy Mother’s Day!

See Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion purposes only.

If you like what you are reading, you can subscribe for free.

Our True Enemy Has Yet to Reveal Himself

By Ben Hunt, Co-Founder and CIO, Epsilon Theory

- May 5, 2025

Before I begin, you can learn more about Epsilon Theory and be notified when we release new content sign up here. You’ll receive an email every week, and your information will never be shared with anyone else. I am not compensated in any way for this recommendation. Just a big Ben fan!

Ben began his post by talking about the large spike in the value of the Taiwan dollar and shared the following 5-year chart for perspective. The spike down means the TWD sharply appreciated vs the USD). The move motivated him to remind everyone about what he recently wrote - What Happens When the US is Just Another Country – and by extension, when the USD is just another currency.

Treasury Secretary Scott Bessent’s “Global Grand Reordering.” Mauldin’s “Great Reset.” Ray Dalio’s “End of Debt Super Cycle.” Neil Howes, “Fourth Turning.” We are in the early innings. If you can’t see it coming, you are not looking in the right direction.

Ben’s outstanding piece, Our True Enemy Has Yet to Reveal Himself. It follows in its entirety:

“I don’t quote from The Godfather, Part 3 very much because it’s not a great movie and isn’t even in the same solar system as Part 1 and Part 2. But Al Pacino has two all-time great scenes here: the “pull me back in!” scene after the failed assassination attempt and the final, wordless cut scene of the movie, where — in a mirror-image contrast to Vito Corleone’s heart-attack-while-gardening death scene in Part 1, immersed in green and laughter and love — Michael collapses and dies alone in a silent, gravelly gray Sicilian courtyard, attended only by a stray dog. Pacino is great throughout the film, honestly, and IMO his realization that the plot against him goes a lot deeper than a blustery Joe Mantegna mobster is better acted than Marlon Brando’s far more famous “it was Barzini all along” scene.

Michael Corleone’s realization of a deeper problem (as captured perfectly by Silvio’s paraphrase in The Sopranos) is summed up in this line — Our true enemy has yet to reveal himself — and it’s a line I couldn’t get out of my head in 2008 and it’s a line I can’t get out of my head today.

No one remembers this anymore, but in the second half of 2007 auto prices and auto sales rolled over in the United States, as did home prices and home sales — two classic indicators of an economic slowdown and a recession. The Big Question was whether we were going into a recession or whether this was just a ‘mid-cycle slowdown’, to use the Wall Street lingo. If you go back and look at the financial media articles and Wall Street analyst reports in Q4 2007, you’ll see tons of stuff about that and surprisingly little about the mortgage-backed securities that would actually blow up the world in 2008. I tell people this story all the time, about how ‘normal’ the Wall Street discourse was in late 2007, and they don’t believe me. But if you were there, you know exactly what I’m talking about.

It’s not that the true enemy — an insanely over-financialized US residential mortgage market — didn’t show itself in 2007. Two Bear Stearns credit funds blew up that summer from their exposure to mortgages that were defaulting at an unexpectedly high rate, and the stock price of mortgage originators like Countrywide took a huge hit over the second half of 2007, as did every bank with a mortgage book. But the STORY was that this wasn’t a problem for the entire mortgage market and the entire financial system, that it was only a problem for mortgage lending to the poors subprime (low credit score) market. Hell, according to Fed Chair Ben Bernanke throughout 2007, the ‘subprime crisis’ was not just contained but ‘well contained’ for any major impact on the broader financial system. Sure, maybe mortgage underwriting standards had gotten a little too lax, especially at ‘rogue’ companies that took crazy risks like Countrywide and Bear Stearns, but if you just took those two bad apples off the board (Bank of America agreed to buy Countrywide in January 2008, and JP Morgan bought the corpse of Bear Stearns in March 2008), then everything would be fine. “Systemic risk is off the table” was the dominant market story in April and May 2008, and both equity and credit markets absolutely rocked.

It was all a lie, of course, that whole ‘well contained’ bit about subprime loans, and it wasn’t even a particularly well-crafted lie. I remember like yesterday the Countrywide earnings call of August 2007, where the original Orange Man — tanning bed aficionado and CEO Angelo Mozilo — told the world that ALL of their mortgages, from subprime through alt-A through prime, were deteriorating at a crazy clip. I mean, it’s not like the data was hidden … every month you could look at the delinquency and default rates for the mortgage securitizations, and every quarter the banks and the originators would take another write down and shuffle their portfolio to avoid taking marks. I remember Countrywide just dumping their Q4 loan data in late January 2008, not even bothering to have a conference call because BofA had announced the acquisition and sidelined Mozilo. Contained to subprime? LOOOL. By Q4 2007 delinquencies and defaults were spreading through every mortgage class and every geography like a highly contagious virus.

The first six months of 2008 were such a psychic struggle for me as an investor. We had gone slightly net short in the hedge fund portfolio in Q4 2007, but the truth is that we went net short more because of a recession view – which was a perfectly comfortable place for my partner and the larger value-oriented firm of which we were part – than because of my ‘true enemy’ and systemic risk view. We got paid for that net short positioning in both Q4 2007 and Q1 2008, but it was REALLY tough to stay the course in April and May if you weren’t prepared to adopt the systemic risk view. From a value investor’s perspective, honestly from any normal-times investor’s perspective, it sure seemed like a meaningful buying opportunity after the public execution of Bear Stearns and the associated all-clear signs from the Fed at the end of March. We did, in fact, shift from the recession view to the systemic risk view (that’s as much a credit to the larger firm and my partner than to me), and in retrospect that was obviously the right call, but man, those months were not easy!

I feel as strongly today as I did in 2008 that our true enemy has not yet revealed himself.

I feel as strongly today as I did in 2008 that the ‘normal’ market discourse around recession and jobs and inventories acts as a distraction from the systemic risk that is manifesting itself.

I feel as strongly today as I did in 2008 that to the degree systemic risk is being discussed, it is described as ‘well-contained’ by the US government even though we can all see with our own eyes that it is not contained at all.

I feel as strongly as I did in 2008 that because tens of trillions of dollars and thousands of financial careers are predicated on the systemic risk not happening, it is very hard to ‘see’ the true enemy and even harder to act proactively to protect yourself. I’ll go farther than that. I think that if you’re in the belly of the beast it’s probably impossible — and almost certainly it’s irrational — to act proactively on what I’m writing about. Which is maybe the biggest problem that the world has right now, that the people who are most aware of the true enemy to the global economic system find themselves in a position where it is career suicide to do anything about it.

In 2008 the true enemy was the over-financialization of the US residential mortgage market, and the catalyst for the true enemy to wreak havoc in the global financial system was a sharp, universal decline in US home prices.

In 2025 the true enemy is the over-financialization of the US Treasury market, and the catalyst for the true enemy to wreak havoc in the global financial system is a sharp, universal decline in the full faith and credit of the United States.

The imposition of ill-conceived, ridiculously implemented tariffs is one way in which this administration diminishes the full faith and credit of the United States, and over the week of April 7 – 11, we saw a flash crash in both 10-year and 30-year Treasuries following the ‘Liberation Day’ imposition of tariffs by the US.

Here are the flash crash charts in more familiar interest rate terms (crash in value = spike in rates), with 10-year Treasuries going from 3.90% to a peak of 4.56% and 30-year Treasuries going from 4.33% to a peak of 4.97%. This may not seem like a massive move if you don’t follow these markets closely, but I promise you that it is!

A one-week 65 basis point increase in US long-term interest rates in the face of a dramatic global growth slowdown is an impossible thing. Impossible, that is, if global capital believes that the United States is good for its debts. Impossible, that is, if global capital believes that US debt obligations provide the risk-free rate for the world.

But it wasn’t impossible. It happened. The US Treasury market – the touchstone of every loan in the world, every insurance policy in the world, every equity valuation in the world – broke last month, and it broke because the full faith and credit of the United States came into question.

The break was temporary. After the initial Treasury crash on Monday April 7 and Tuesday April 8, the Trump administration rushed to say ‘haha! just kidding about those reciprocal tariffs on everyone!’ and folded a lot of its cards on Weds April 9. It folded still more of its cards the following week after a resurgent Treasury crash that Friday April 11.

Why did the administration fold most of its tariff cards? Because another one-week 65 basis point increase in US long-term interest rates would break the world. Seriously, everything would break. Every insurer would be in regulatory forbearance and would need to raise capital, and so would most banks. The dollar would crash. Equity markets would crash. Lending and credit would come to a screeching halt. The Fed would be forced to engage in what’s called ‘yield curve control’ where they would flat out buy (and effectively force big US banks to buy) these 10-year and 30-year Treasuries in order to keep their value propped up and their interest rates tamped down. Would that work? Probably. For a while. Maybe. I mean it’s not like you’re engaging in yield curve control from a position of fiscal and trade strength/surplus like the Bank of Japan buying up all of its long-dated sovereign debt. The Fed would literally be doing the Weimar thing at this point. Which brings me to my next point.

The imposition of ill-conceived, ridiculously implemented tariffs is one way in which this administration diminishes the full faith and credit of the United States. It is by no means the only way.

The classic way to diminish the full faith and credit of your country is to pass a massive, unfunded tax cut and blow out your already obscene budget deficit. Like the ‘big, beautiful bill’ that the House is taking up this month.

That’s the next catalyst for the true enemy to reveal himself.

The craziest part of all this is that we saw just two years ago in the UK what happens to sovereign debt when a government of ideologues true-believers imposes a big unfunded tax cut and blows out their deficit.

On September 23, 2022, newly installed Prime Minister Liz Truss and her newly appointed Chancellor (equivalent of our Treasury Secretary) Kwasi Kwarteng presented what was called a ‘mini-budget’ — a big new tax cut program that would blow out the budget deficit, but hey, don’t worry that we’re not funding this by cutting spending or taking in new revenue because all that money going back to ‘job creators’ will surely spur economic growth and more tax revenue down the road in, like a decade or two. Plus there’s gotta be some Waste and FraudTM to eliminate. Sound familiar?

As soon as Kwarteng announced the plan, both the UK pound and their equivalent to 10-year and 30-year Treasuries (called gilts) began to crash (and so rates began to spike). And because some UK pension funds had implemented a too-clever-by-half program to hedge their long-term pension liabilities with long-term gilts, and not only that but had funded the program through leverage and derivatives which could prompt a margin call, and not only that but since they couldn’t satisfy the margin call the banks were selling their long-term gilts into this market collapse … well, in three days the interest rate on 30-year gilts blew out by more than 100 basis points. Now that’s a crash!

The Bank of England intervened on Sept 28, pledging to purchase as many 30-year gilts as necessary to stabilize the market and bail out the pension funds over the following two weeks. On the heels of the BOE announcement, rates came quickly back down to where they started by Sept 30, and the crisis was over. Except it wasn’t. Yes, the Bank of England had intervened to bail out the pension funds from their disastrous ‘liability hedge’, but the Truss/Kwarteng policy was still in effect. Long-term interest rates began to climb again in early October, not because the UK pension funds were forced sellers but because global capital had lost trust in the full faith and credit of the UK government. It wasn’t until Kwarteng resigned and the unfunded tax-cut plan was removed (with Truss’s resignation soon to follow) that the UK currency and sovereign debt returned to some semblance of normalcy.

To be sure, there are plenty of important differences between the UK sovereign debt market and the US Treasury market, all of which make the US market more robust. For example, the US Treasury market is far deeper and more liquid, especially at that 30-year point, and the US debt market has interest-only strips and other instruments that allow pension funds and insurers to hedge long-term liabilities without getting into the same pickle as the UK pension funds. But it’s not THAT different, and it’s especially not that different in the October market reaction to unfunded tax cuts after the Bank of England bailed out the UK pension funds. No, the main difference I see, and it makes the US less robust to this sort of shock than the UK, is this:

Do you really think that Trump would back down from passing a big, beautiful tax cut bill even if the bond market freaks out about it?

Do you really think that Trump would back down from passing a big, beautiful tax cut bill AND continue to back down from his tariffs?

Or do you think that Trump will start talking about the need to ‘do something’ about non-US holders of US Treasuries, because they’re not ‘treating him fairly’?

As someone who has looked at Trump debt offerings for his Atlantic City casinos back in the 2000s, as someone who has listened to Trump absolutely revel in the cramdowns of his former bondholders even as he was seeking new bondholders … I think we’re headed for Door #3. More broadly, I am convinced that Donald Trump sees debt — whether it’s his company’s debt or his country’s debt — in purely instrumental terms, as a means to secure some future concession, not as an obligation based on any moral or non-instrumental grounding. And since April 2nd, I am convinced that the rest of the world sees that, too.

It’s not the tariffs. It’s not the tax cuts. It’s not the recession. These are just the catalysts, the vehicle through which the true enemy shows himself.

The true enemy is uncompensated risk in the risk-free securities that have been financialized and levered across every substrate of the global economic system, uncompensated risk that comes from a diminishment of the full faith and credit of the United States.

To fight the true enemy, we must restore trust in the full faith and credit of the United States.

I don’t know how to do that, especially when the chief executive of the United States is only comfortable when he can act as a BB- credit, but that’s the conversation we will all be having in the weeks and months to come.”

The views are those of Ben Hunt and are subject to change.

SB Here: As you can tell, Ben is not a Trump fan. I prefer a more surgical approach to trade vs. the sledgehammer approach. But I do like the idea of gold visas.

Behaviorally, I think Ben has the right read. Agree or disagree, ultimately, the markets will be the arbitrator. The key things for us to watch are the U.S. dollar and the long-term Treasury yields. They are the heartbeat of our debt-ill patient. Watch them closely. A Trump-like Truss moment? Maybe.

Counterpoint: One million gold visas at $5 million a piece would be very good. $5 trillion in new revenue is a meaningful way to reduce the $37 trillion outstanding U.S. debt. Cutting the budget deficit to 3% of our GDP would also be good. Can either or both happen? Maybe.

We are on a path towards some form of restructuring. There are a few good tickets in the investment fishbowl today. If you are a traditional 60-40 buy-and-hold index investor, when you put your hand in to pull one out, the odds are low that you’ll pick a winner. Better to wait for the next market dislocation when overvalued stocks become undervalued. Then there will be more winning tickets in the fishbowl—Ditto for bond investors. What good is a 4.3% 10-year Treasury yield in a rising inflation, rising interest rate cycle?

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change.

The information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: Update - May 8, 2025

Market Commentary:

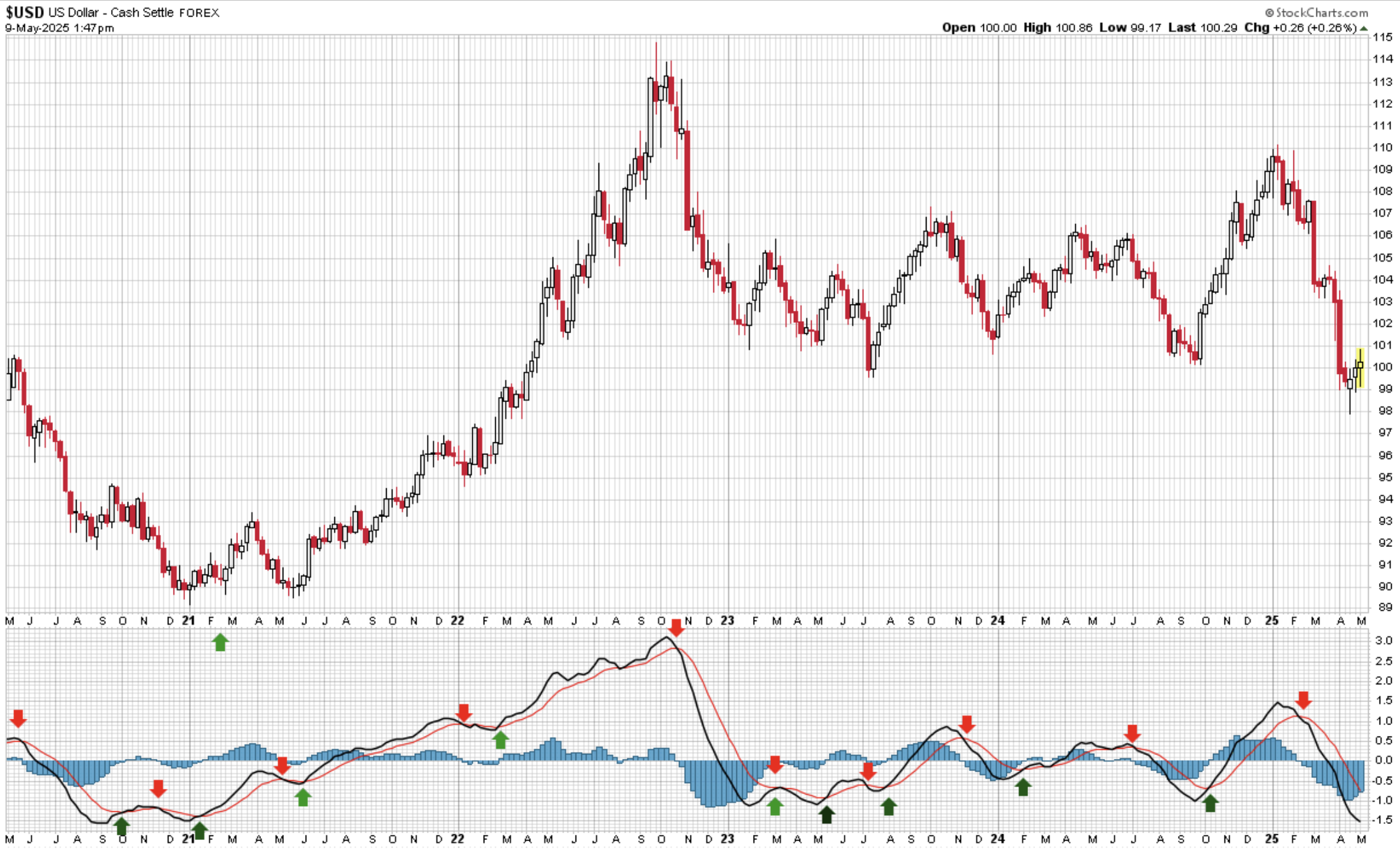

The following is an updated look at the dollar, the dollar vs. the yen, and the 10-year U.S. Treasury Yield through May 8.

U.S. Dollar

The current Weekly MACD is signaling a declining dollar.

This, in my view, is a critically vital chart to watch.

Source: Stockcharts.com

The Japanese Yen to U.S. dollar

The current Weekly MACD signal is for a rising Yen.

A rising Yen against the declining dollar is bearish for global liquidity.

Source: Stockcharts.com

10-year Treasury Yield

The red arrow in the upper right points to the current yield of 4.36%.

The current MACD trend signal is bearish on bonds, pointing to rising interest rates.

Source: Stockcharts.com

No guarantees. Not a recommendation to buy or sell any security.

I share trend charts and more each week in Trade Signals, a free service for clients.

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Happy Mother’s Day

As I mentioned, I’m in Florida for business. I'm playing Hawks Nest tomorrow with my friend and client John L.

Located in Vero Beach, Florida, Hawk's Nest is part of The Moorings Yacht & Country Club. The golf course recently reopened after being refurbished. I hear it is beautiful.

They are also hosting the Florida Mid-Amateur this weekend. We tee off just after the final pairings tee off. I sure wish I could play as well as them.

The Moorings at Hawk's Nest (Hawk's Nest Golf Course)

Susan and I will then travel across the state to Venus, Florida, to visit her mother and celebrate Mother’s Day.

The most important beings on the planet are women. No one is more important than a mother.

My mother graduated way too early. I think of her often. I feel her with me often. And I’ll be sending her extra love on Sunday.

Wishing you, your mother, and all mothers everywhere a warm and wonderful Mother’s Day!

Checking in happy and grateful.

Finally, the Mauldin Economics Strategic Investment Conference begins next week. John tells me it will be great, especially given the advanced state of our debt challenges. I’ll be taking notes and focusing on what matters most. Stay tuned!

With kind regards,

Steve

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201, Malvern, PA 19355

Private Wealth Client Website

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.