On My Radar - The Times They Are A-Changin’

May 2, 2025

By Steve Blumenthal

“Come writers and critics

Who prophesize with your pen

And keep your eyes wide

The chance won't come again

And don't speak too soon

For the wheel's still in spin

And there's no tellin' who

That it's namin'

For the loser now

Will be later to win

For the times they are a-changin'”

— Bob Dylan, The Times They Are A-Changin

Another interesting week. The Institute of Supply Managers’ manufacturing index, considered one of the best leading indicators of economic growth, signaled recession. The report comes out on the first of each month. The headline number is below 50, which separates expansion from recession. We’ll look at that below, along with a few other key recession watch indicators.

Important, but what is predominantly On My Radar this week is Ray Dalio’s Monday, April 28 post. If the headline doesn’t hit you like a double espresso, then you may not be human:

It's Too Late: The Changes Are Coming

“Some people believe that the tariff disruptions will settle down as more negotiations happen and greater thought is given to how to structure them to work in a sensible way. However, I am now hearing from a large and growing number of people who are having to deal with these issues that it is already too late,” He wrote.

Ray advises “calm, analytical, and coordinated engineering and implementation…” to produce the “beautiful deleveraging and rebalancings that need to take place.” But he said, “Unfortunately, thus far we haven’t seen the better ways and have instead seen disturbing fighting and volatility that are teaching lessons that are leading to irreversible bad consequences.”

“Come, senators, congressmen

Please heed the call

Don't stand in the doorway

Don't block up the hall

For he that gets hurt

Will be he who has stalled

The battle outside ragin'

Will soon shake your windows

And rattle your walls

For the times they are a-changin'“

Grab your coffee, find your favorite chair, and channel your inner Bob Dylan, “For the times they are a-changin’.” Following last week’s American Pie piece, I seem unable to get that 1960s and ‘70s era of social conscience, depth, and poetic storytelling out of my mind.

Viewing this from an economic perspective, it’s unlikely that all of our trade partners will bend the knee. Others have to survive and are making changes. And it will be challenging, as Ray Dalio points out.

Ray’s post is short and essential - definitely worth your time. As we move forward, I’ll continue bringing you insights from some of the most brilliant minds in global economics and do my best to distill it down into language that makes sense. In that spirit, I’m resharing the Zulauf-Marks segment from last week. It’s well worth a second read. As you go through it, consider the likely outcomes and potential investment ideas for navigating these changing times.

On My Radar:

It’s Too Late: The Changes Are Coming

Recession Watch Indicators

Felix Zulauf and Howard Marks

Trade Signals: Update - April 30, 2025

Personal Note: Ever Forward

See Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion purposes only.

If you like what you are reading, you can subscribe for free.

It’s Too Late: The Changes Are Coming

By Ray Dalio, Founder, CIO Mentor, and Member of the Bridgewater Board - April 28, 2025

Many exporters to the United States and importers from other countries that trade with the U.S. are saying they have to greatly reduce their dealings with the United States, recognizing that whatever happens with tariffs, these problems won't go away, and that radically reduced interdependencies with the U.S. is a reality that has to be planned for.

Most obviously, American producers and investors in China, Chinese producers and investors in China that deal with Americans, American producers and investors in the United States that deal with Chinese, and Chinese producers and investors in United States that deal with Americans must now go about making alternative plans, regardless of what the next round of trade negotiations are like. While this need to minimize U.S. - China interdependence and worry about conflict is now broadly recognized, this view is now becoming more commonly believed by most people in most countries who are dealing with most issues related to trade relations, capital markets relations, geopolitical relations, and military relations with the United States.

Though not yet fully realized, it is also increasingly being realized that the United States' role as the world's biggest consumer of manufactured goods and greatest producer of debt assets to finance its over-consumption is unsustainable, so assuming that one can sell and lend to the U.S. and get paid back with hard (i.e. not devalued) dollars on their U.S. debt holdings is naive thinking, so other plans have to be made.

Said more simply, enormous trade and capital imbalances are creating unsustainable conditions and major risks of being cut off, so they must come down -i.e., excessive imbalances + deglobalization = smaller trade and capital imbalances.

More broadly, what I am saying is that, based on many of my indicators, it appears that:

1) we are on the brink of the monetary order, the domestic political and the international world orders breaking down due to unsustainable, bad fundamentals that can be easily seen and measured,

2) the progression of events leading to these increasing disorders is similar to those that have progressed many times throughout history, so this one looks like a contemporary version of the old story of how monetary, domestic political and social, and international geopolitical orders change,

3) there is a growing risk that the United States, imposing these challenges to deal with, will increasingly be bypassed by a world of countries that will adapt to these separations from the United States and create new synapses that grow around it, and

4) if these circumstances are managed in the best ways, the outcomes will be much better than if they are managed in the worst ways.

In my opinion, what would be best is calm, analytical, and coordinated engineering and implementation, with the imbalances and the needs for self-sufficiencies treated as shared challenges, to produce the “beautiful" deleveragings and rebalancings that need to take place. For example, as explained in my new book, How Countries Go Broke: The Big Cycle, there is a "3-Part, 3-Percent Solution" to dealing with the U.S. government debt problem that would lead to much better results than the path that we appear to be on. Unfortunately, thus far we haven’t seen the better ways and have instead seen disturbing fighting and volatility that are teaching lessons that are leading to irreversible bad consequences.

For these reasons, I fear that we are moving beyond the ideal time to be knowledgeable about and properly plan for these big changes in the world order, and believe that investors, policy makers, and other decision-makers need to stop undulating their views and positions in reaction to the day-to-day market moves and policy announcements and instead deal with these big fundamental changes in the world order calmly, intelligently, and, ideally, cooperatively.

The views are those of Ray Dalio and not necessarily those of Bridgewater (or mine).

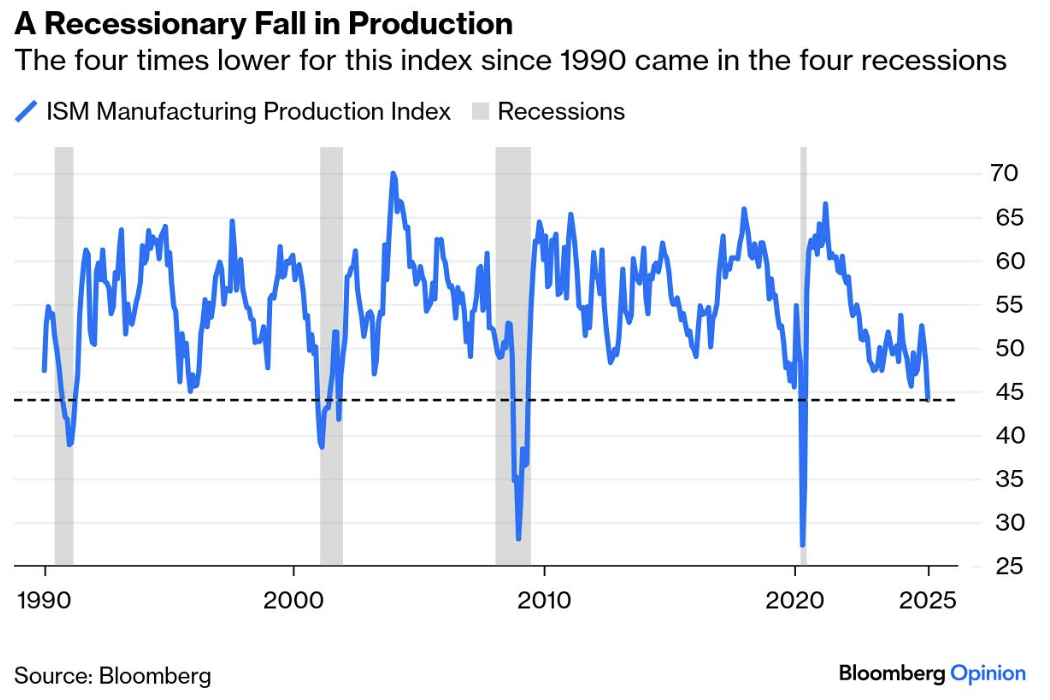

There are many recession watch indicators to follow, and none are perfect. This one has a perfect batting average since 1990. There have been four instances when the index dropped below 50, and a recession occurred in all four.

Recession Watch Indicators

Sharing with you several recession-watch indicators.

The first is the ISM manufacturing index. It has correctly signaled every recession since 1980. It signaled number five, this week.

High yield and Small Caps - A canary in the coal mine indicator. Currently not signaling recession.

The inverted yield curve - It continues to warn of recession.

Let’s begin with Bloomberg’s John Arthurs and his take on the ISM signal. John sends a daily email. To get it delivered to your inbox, sign up here.

From today’s newsletter, “The Institute of Supply Managers’ manufacturing index, long regarded as one of the best leading indicators of economic growth, was on the face of it alarming. The overall headline number is below the 50 that separates expansion from recession. Within it, the report on how much manufacturers were producing was downright alarming:”

Source: John Arthurs, Bloomberg

Interestingly, the yield on the 2-year Treasury Note moved higher, not lower. Lower yields tend to happen when heading into and during recessions.

Economists and traders found some nuances in interpreting the data. Tariff confusion? Likely. Foreigners selling our bonds? Maybe.

According to a Bloomberg article this morning, the index's new orders (imports) improved slightly, but exports fell to a low previously seen only in recessions. Businesses are likely stocking up before the tariffs kick in.

Pour enough sand into the gears of the global trade systems, and I can’t see how it doesn’t land us in recession. ISM is signaling recession.

High-Yield Bonds and Small-Cap Stocks

While the trend is lower (orange and light blue lines—focus on 2025), the current signal is bullish. The S&P 600 small-cap stock index is above its 36-day smoothed moving average line, and the number of S&P 600 stocks that are advancing in price vs. declining in price is above its smoothed moving average line. The data boxes reflect the performance when the orange and light blue lines trend higher, as in the current case.

Source: NDR

Inverted Yield Curve

Another excellent recession indicator is the inverted yield. When the longer-term 10-year Treasury Note yield drops below the short-term 6-month yield, it signals something is wrong within the system. Think of it like a high-grade fever in a human.

Not all, but most prior yield curve inversions, dating back to 1958, landed us in recession. I’ve added red arrows to mark past occurrences. The grey bars show recessions.

The most recent inversion lasted a record 30 months before normalizing in January. It has since inverted again.

It’s important to note that a recession follows when the yield curve normalizes, not when it first inverts. That has occurred.

The bottom line is that the probability of a recession is high… and the tariff situation can potentially accelerate the timing and severity.

Source: NDR

Felix Zulauf and Howard Marks

“When there is too much government debt relative to the quantity of money that is needed to service debts, the government will either increase the amount of money that exists and/or cut the amount they will pay. In either case, it’s not good for holders of debt assets.” - Ray Dalio, @raydalio, Principle of the day.

Felix Zulauf’s Adam Taggart interview - You can find the link to the full interview here.

I broke my summary notes down into six major points with bold emphasis:

1. Tariffs and the Dollar

Trump’s renewed tariff strategy, especially against China, represents a shift toward protectionism. While initially meant to rebalance the trade deficit and "onshore" production, it creates systemic consequences:

Tariffs introduce uncertainty into global trade flows, prompting retaliation or realignment from partners.

Foreign demand for U.S. assets may decline as tariffs disrupt the trade surpluses that were once recycled into Treasuries.

He suggests we’re entering a multi-year decline of the U.S. dollar, not because another reserve currency is emerging, but because less global trade is being settled in USD.

Capital flight, where foreigners sell off Treasuries, equities, etc., leads to a weaker dollar, higher yields, and a feedback loop of tighter financial conditions.

2. Inflation and Interest Rates Outlook

The structural decline in the dollar, combined with reshoring supply chains and less global labor arbitrage, points to:

Persistent upward pressure on prices, especially for goods that were previously cheaply imported.

This likely marks the end of the disinflationary period that resulted from decades of globalization, leading to a shift in the regime toward higher structural inflation.

Consequently, interest rates will need to stay elevated to counteract these inflationary forces. This is a stark departure from the ZIRP/NIRP era.

Geopolitical Economics

The U.S.’s era of global financial and military leadership is giving way to a multipolar world.

3. Breakdown of Multilateral Trade Norms

The death of GATT/WTO rules, as the report phrases it, signals a breakdown in the rules-based global trade system.

Trump's unilateral tariffs violate WTO norms, and while the Biden Administration initiated moves like removing Russia from SWIFT, Trump is accelerating the decoupling of U.S. economic dominance.

Other nations are responding by diversifying away from the US Dollar in trade and reserves, further eroding its dominant role.

4. Pax Americana in Decline

The U.S.’s era of global financial and military leadership (Pax Americana) is giving way to a more multipolar world.

As the U.S. retreats from acting as a global enforcer, regional powers like China are asserting themselves.

This accelerates a geopolitical realignment with long-run implications for capital flows, currency reserves, and commodity trade.

Economic Cycle and Policy Response

5. Recession Likely in 2025, Stimulus Thereafter

Felix forecasts a brief global recession due to the tariff shock and widespread uncertainty.

Trump is front-loading pain to reset global trade terms early in his term. From late 2025 into 2026 (midterms), fiscal stimulus is expected, including tax cuts and public investment, especially in the U.S., Germany, and China. A trigger for a strong stock market rally in 2026 into 2027.

However, the stimulus will be debt-financed, requiring central banks to monetize deficits, which could lead to steeper yield curves and renewed QE-like policies.

Markets and Monetary Implications

Felix is expecting a roller coaster-like ride for equities. Trade the trends. Buy and hold to produce little net gain over the coming 10 years. He is bullish on gold, bitcoin, and commodities.

6. Asset Price Signals

Equities: Most global indices have corrected. Felix believes we are currently in a bottoming process (over the next three to six months) and forecasts an S&P 500 rally of as much as 40% from current levels in 2026 and 2027. (SB here: This is undoubtedly not the general consensus.)

Gold: Acting as a safe haven and de facto reserve asset. The current rally is entering a parabolic climax phase (~$3,400 target), but remains structurally bullish as dollar hegemony wanes.

Bitcoin: High-beta proxy for risk sentiment, also potentially co-opted by the Trump administration to boost demand for U.S. Treasuries by using crypto collateral in financial plumbing.

Commodities: He expects oil to eventually surge beyond $150–$200 per barrel (not a typo) due to underinvestment, geopolitical realignments, and replenishments of strategic reserves.

Bottom Line

Felix is forecasting a macro regime shift: from globalization to protectionism, from USD dominance to multipolar trade, from disinflation to structurally higher inflation. He forecasts that market volatility will remain elevated as the system rebalances. He believes that equity markets are near a medium-term bottom, especially if Trump tones down tariffs ahead of the 2026 midterms.

At a higher level, he argues that we’re witnessing the end of the post-WWII U.S.-led economic order and entering an era where geopolitics, inflation, and trade frictions define capital flows and monetary policy more than they have in the last 30 years.

Source: Sited in the above video with the replay link.

Views are Felix Zulauf’s and are subject to change. This is not investment advice for you. Speak with your advisor. Please reach out to me if you would like to know what we’re doing. All investing runs the risk of loss. There are no guarantees.

Lights on! Let’s see what the great Howard Marks has to say.

Howard Marks on Globalization (from X)

1 - Globalization was the invisible force behind 30 years of disinflation.

Cheap labor from abroad

Unlimited access to global supply chains

Relentless outsourcing to drive margins up

This kept consumer prices low and profits high. That era is ending.

2. Deglobalization is inherently inflationary. When you replace efficient, global production with expensive, domestic alternatives:

Input costs rise

Supply chains slow down

Price volatility increases

Mark’s sees this as structural, not temporary.

3 - Tariffs are a symptom of a deeper fracture. Forget just US-China. Look around:

US-Europe disputes

India is raising import duties

China retaliating against Western tech restrictions

This isn’t a trade war. It’s a global economic divorce. And the market isn’t pricing it in.

4 - The old playbook dies here. For decades, the move was:

Long multinationals

Long emerging markets

Short volatility

Buy the dip

In a tariff-heavy, fragmented world:

Margins get squeezed

Supply chains fracture

Inflation spikes unpredictably

Policy risk rises

It’s a different game now.

5 - Marks’ big thesis: Pricing power is survival. In a fragmented, inflationary market, the companies that win are those who can:

Control their supply chain

Set their own prices

Operate regionally

Withstand higher input costs

This will radically reprice sectors.

6 - The likely winners in this regime:

Domestic manufacturers

Defense and aerospace

Commodities and miners

Infrastructure and utilities

Industrials with pricing power

He said, “Safe-haven hard assets will matter again.”

7 - The losers?

Global retailers are reliant on imports

Debt-loaded companies exposed to rate shocks

Tech firms with fragile margins

Emerging markets tied to exports

Many of today’s market darlings are structurally disadvantaged in this environment

8 - The wildcard risk: Policy intervention. As inflation persists and economic pressure mounts, governments will:

Subsidize industries

Impose new price controls

Restrict capital flows

Markets aren’t built for this kind of hands-on management. Volatility will rise.

9 - The market isn’t pricing this in yet. Most models still assume a return to pre-2020 norms.

Marks argues this is a decade-long shift, not a blip.

Smart money will start repositioning before it’s obvious.

10 - Bottom line: Howard Marks’ message is clear:

“If you don’t adjust to this new world of tariffs, fragmentation, and inflation volatility — you’ll be left behind.”

He said, “Markets change. Winners change. The playbook must too.”

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. The information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: Update - April 30, 2025

Market Commentary:

The orange line in the following chart points to a logical overhead resistance level. It also corresponds with the April 2nd “Liberation Day” close. That’s the 10% across-the-board tariff day, with special extra tariffs given to China.

An equity sell-off from here is probable. Not a guarantee.

Investor sentiment has moved away from extreme pessimism levels. While investors are still feeling more bearish than bullish, this is no longer bullish for equities. Extreme bearish readings (fear) are a short-term bullish indicator for stocks, while extreme bullish readings (greed) are short-term bearish for equities.

The following chart also shows that the Weekly MACD trend indicator is bearish but improving (bottom section, lower right).

Source: StockCharts.com

No guarantees. Not a recommendation to buy or sell any security.

I share trend charts and more each week in Trade Signals, a free service for clients.

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Ever Forward

I recently watched the Bob Dylan movie A Complete Unknown and enjoyed it. Mr. Tambourine Man, Like a Rolling Stone, Don’t Think Twice, It’s All Right, and Blowin’ in the Wind. What a poet, what a genius, what a voice. And maybe he is right…

The answer, my friend, is blowin' in the wind

The answer is blowin' in the wind

Florida is next—hat tip to my friend John L. His course, Hawks Nest, is hosting the Florida Mid-Amateur next week. And, I’ve got my fingers crossed for a Knicks game in NYC.

The weekend weather here is suburban Philly is looking pretty good. Coach Sue’s team has a big away game. I’ll be heading to Stonewall to play a few holes on Saturday. Sunday is power washing day. The back patio needs some love; I’ve been holding it back. I don’t mind power washing day. It can be meditative in a way. With ear buds in and volume high, I’ll be listening to Bob Dylan, and focusing on opportunities. There are many.

Now sing with me:

“Come writers and critics

Who prophesize with your pen

And keep your eyes wide

The chance won't come again

And don't speak too soon

For the wheel's still in spin

And there's no tellin' who

That it's namin'

For the loser now

Will be later to win

For the times they are a-changin'“

Restructuring is needed. It’s coming; as Zulauf and Marks pointed out, there are opportunities. It’s not in overvalued equities, low-yielding bonds, and bond funds.

Every forward.

Steve

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201, Malvern, PA 19355

Private Wealth Client Website

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.