On My Radar - What’s the Trade?

March 28, 2025

By Steve Blumenthal

“The Big Short Part II: It may just be the biggest bubble of all time.”

— Stephen Blumenthal, CMG, CEO, CIO

I have a good friend nearing the end of his career in private equity. We spent the day skiing this week. Of course, geopolitically and economically, nothing feels right.

He told me a story about a gathering of fund managers and economists. All were spewing about the then-current state of play. Cutting through the noise, one woman said, “Enough! What’s the trade?”

In 2008, the big play was to short the housing market. Michael Lewis storied it in his best-selling book, The Big Short. Of course, it wasn’t just the collapse of subprime mortgage bonds; the housing and equity markets also took it on the chin.

A lot of homework, patience, and guts went into that trade.

In my view, Ray Dalio is doing the world an excellent service by helping many better understand the current state of play. What he calls his “most important chapter” was posted on his LinkedIn page this week. I will share some highlights today, along with a link to the full post.

Grab that coffee and read on. As you read, keep your judgment and emotion hats on the shelf, and put your investor hat on. There are many moving pieces with decisions to be made that require leadership and execution that we don’t know about yet. In the direction of optimism, I have to say that I felt some hope after listening to David Friedberg's interview with Howard Lutnick on the All In podcast. It was a candid discussion with ideas on how to right-size the U.S. debt mess.

“What’s the trade?” I conclude with a few of my thoughts in that direction.

On My Radar:

How Countries Go Broke: The Overall Big Cycle, by Ray Dalio

All In Podcast - Howard Lutnick

What’s the Trade?

Trade Signals: Update - March 27, 2025

Personal Note: Snowbird Photos and Ghibli

See Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion purposes only.

If you like what you are reading, you can subscribe for free.

How Countries Go Broke: The Overall Big Cycle, by Ray Dalio

March 26, 2025 via LinkedIn

“If I had to pick the most important chapter in the book, this would be it. That is because it deals with the biggest and most important forces that are dramatically changing the world order, and it shows how and why these forces have repeatedly driven history through its big cycles. Having seen so many of these cycles, watching what is happening is like watching a movie that I have seen many times before—just a contemporary version in which the clothes that the people are wearing and the technologies that they are using are more modern. I hope to show you what I see. Also, by showing what happened in the past and why it happened, we can understand how previously unimaginable developments are now happening and could happen in the future.

While this book is mostly focused on understanding what’s going on with debt/credit/money/economic cycles, we can’t look at this dynamic in isolation and make sense of it because how these cycles transpire is influenced by other big forces. Similarly, to understand what is happening in other areas, we need to understand the debt/credit/ money/economic force as it has big effects on developments in most areas. Together, five big forces produce the Overall Big Cycle that leads to radical changes in monetary, domestic, and/or world orders.

I comprehensively explained how this Overall Big Cycle works and how it was manifest over the last 500 years in Principles for Dealing with the Changing World Order, but I won’t cram that 600-page book in here. Instead, I am going to give you a brief summary. That way, when we turn to Part III about what has happened in our current Big Cycle, and Part IV, in which I will try to look into the future, you will be able to see how what actually happened compares with my templates of both the Big Debt Cycle and the Overall Big Cycle.

HOW THE MACHINE WORKS

Because everything that happens has reasons that make it happen, it appears to me that everything changes like a perpetual motion machine. To understand this machine, one needs to understand its mechanics. Because everything affects everything else directly or indirectly, these mechanics are very complex. Sometimes I try to explain what I know about them with enough of their complexity to show them in useful detail, such as I did previously in this book to explain how countries go broke. And sometimes I try to explain them simply. As the saying goes, “Any fool can make something complicated. It takes a genius to make it simple.” In this chapter, I will try to explain the Big Cycle simply. I will begin by explaining my approach.

As a global macro investor for most of my life, I have tried to understand and model the cause/effect relationships and use my models to bet on what will happen in the markets. To do that, for about the last 35 years, I have created computerized expert systems that enable the computer to make decisions like I make them. These systems are based on the following principle:

Decision-making systems should be based on timeless and universal relationships, meaning that they should explain all the big, important developments in all time frames and in all countries, though not necessarily precisely or in detail. If they fail to explain all the big developments in all time frames and in all countries, that indicates that an important influence is missing and needs to be added to the template/model.

The expert systems I have built are previously developed forms of artificial intelligence. Now, with various breakthroughs in artificial intelligence, I am—and I believe we all are—on the brink of being able to understand all of the cause/effect relationships that drive everything, though for now we still have to labor along the old-fashioned way, with people studying what happened using the computing and AI tools available today. That is why, in my own feeble attempts to understand and describe the most important mechanics that change the world as we know it, I do these in-depth studies and create explanations of them. What I am about to describe is a result of this process. However, because the forces that drive the Big Cycle are so big, it is easy to see and understand them without worrying about the details and the complexities.

Zooming out to the highest level, the five most important drivers of change are:

1. The debt/credit/money/economic cycle

2. The internal order and disorder cycle

3. The external geopolitical order and disorder cycle (i.e., the changing world order)

4. Acts of nature (droughts, floods, and pandemics)

5. Human inventiveness, most importantly of new technologies

These forces affect each other to shape the biggest things that happen, creating cycles that move markets and economies around an upward-sloping trend line. The incline of its upward slope is primarily driven by the inventiveness of practical people (e.g., entrepreneurs) who are given adequate resources (e.g., capital) and work well with others (their coworkers, government officials, lawyers, etc.) to make the inventions and products that create productivity improvements.

Over a short period of time (i.e., 1-10 years), the short-term cycles, especially the debt and political cycles, are dominant. Over a long period of time (i.e., 10 years and beyond), the long-term cycles and the upward-sloping trend line in productivity have much bigger effects.

As I explained earlier, conceptually the way this dynamic transpires looks like this to me:

SB here: I encourage you to click through to Dalio’s LinkedIn post to better understand the nuances of the 5 most important drivers of the Big Cycle. Here is the link.

I want to provide you with Ray’s conclusion of this segment of his new book, which will be available in June 2025.

From Ray:

“That’s enough of the Big Cycle for now—enough to help you better understand the dynamics you’ll read about in Part III as you look at the events that have unfolded since our current Big Cycle began in 1945 with the end of World War II. It will also help you understand the perspective I take when I attempt to look into the future in Part IV. But before we move on, it is worth sharing one final principle, which has the biggest impact on how the challenges that arise during the Big Cycle are handled, namely:

The biggest and most important force is how people deal with each other.

If people deal with their problems and opportunities together rather than fight each other, they can get the best possible results. Unfortunately, while technology has evolved a lot, human nature hasn’t changed much, so this is still probably beyond the capabilities of humankind.”

The views expressed in this article are mine and not necessarily Bridgewater’s.

The information provided herein is not intended to provide a sufficient basis on which to make an investment decision and investment decisions should not be based on simulated, hypothetical, or illustrative information that have inherent limitations. Unlike an actual performance record simulated or hypothetical results do not represent actual trading or the actual costs of management and may have under or overcompensated for the impact of certain market risk factors. Bridgewater makes no representation that any account will or is likely to achieve returns similar to those shown. The price and value of the investments referred to in this research and the income therefrom may fluctuate. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur. Investments in hedge funds are complex, speculative and carry a high degree of risk, including the risk of a complete loss of an investor’s entire investment. Past performance is not a guide to future performance, future returns are not guaranteed, and a complete loss of original capital may occur. Certain transactions, including those involving leverage, futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Fluctuations in exchange rates could have material adverse effects on the value or price of, or income derived from, certain investments.

Bridgewater research utilizes data and information from public, private, and internal sources, including data from actual Bridgewater trades. Sources include BCA, Bloomberg Finance L.P., Bond Radar, Candeal, CBRE, Inc., CEIC Data Company Ltd., China Bull Research, Clarus Financial Technology, CLS Processing Solutions, Conference Board of Canada, Consensus Economics Inc., DataYes Inc, Dealogic, DTCC Data Repository, Ecoanalitica, Empirical Research Partners, Entis (Axioma Qontigo Simcorp), EPFR Global, Eurasia Group, Evercore ISI, FactSet Research Systems, Fastmarkets Global Limited, the Financial Times Limited, FINRA, GaveKal Research Ltd., Global Financial Data, GlobalSource Partners, Harvard Business Review, Haver Analytics, Inc., Institutional Shareholder Services (ISS), the Investment Funds Institute of Canada, ICE Derived Data (UK), Investment Company Institute, International Institute of Finance, JP Morgan, JSTA Advisors, M Science LLC, MarketAxess, Medley Global Advisors (Energy Aspects Corp), Metals Focus Ltd, Moody’s ESG Solutions, MSCI, Inc., National Bureau of Economic Research, Neudata, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Refinitiv, Rhodium Group, RP Data, Rubinson Research, Rystad Energy, S&P Global Market Intelligence, Scientific Infra/EDHEC, Sentix GmbH, Shanghai Metals Market, Shanghai Wind Information, Smart Insider Ltd., Sustainalytics, Swaps Monitor, Tradeweb, United Nations, US Department of Commerce, Verisk Maplecroft, Visible Alpha, Wells Bay, Wind Financial Information LLC, Wood Mackenzie Limited, World Bureau of Metal Statistics, World Economic Forum, and YieldBook. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability, or use would be contrary to applicable law or regulation, or which would subject Bridgewater to any registration or licensing requirements within such jurisdiction. No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater® Associates, LP.

[1] Additionally, there is the demographic force that will certainly lead to a lot of old people who don’t work and will be expensive to support (because at that stage in their lives, their healthcare costs will be high), a shrinking workforce in developed countries, large increases in population in less developed countries, and only a small percentage of the people being truly productive.

[2] I explained these more completely in Chapter 5, “The Big Cycle of Internal Order and Disorder,” of Principles for Dealing with the Changing World Order.

All In Podcast - Howard Lutnick

Domestic and international politics play a significant role in the outcome of the debt crisis. Last week’s “Signal” text breach remains a big concern.

I subscribe to my friend Danielle DiMartino Booth’s Daily Quill. She is a fabulous writer. I asked if I could share her latest piece with you, “Not in Our Hemisphere — Contextualizing the Tariff Terror Crusade.” She points to an article in the Atlantic, “China’s exploitation of overseas ports and bases.” We are in a cold war with China. They are not our friends.

Protecting our ports is a good idea. Strategically, an agreement with Greenland is a good idea. The Cold War could turn hot. Picking fights with our long-time allies? Concerning is an understatement. War is afoot.

Danielle attended a presentation where Condoleezza Rice was the keynote speaker. Rise said, “There’s this notion that if we [U.S.] leave the playing field, it’’ll be okay, but in fact, great powers don’t mind their own business. And the great powers that would supplant American power are not ones that share our values, will not uphold our interests - China, Russia… we have to get up and go back to bat because too much is at stake for the United States to turn its back on the international system.”

Danielle wrote, “Our allies are being forced to fend for themselves, and this is the right thing up to a point. But we must appreciate the context in which events are unfolding… we need to thread the narrowest of needles.”

Trump seems hell bent on taking a wrecking ball to most everything. Some of it I like. Some of it I cringe. From an economic perspective, I see a fast path into recession soon. Buckle up.

If you caught last week’s OMR, I shared a link to the All In Podcast discussion with Treasury Secretary Scott Bessent. I’m thrilled he is leading the Treasury. I didn’t mention the additional podcast discussion: Commerce Secretary Howard Lutnick. That one I downloaded for my plane ride west.

Next, you’ll find the link. I’m adding it after Ray Dalio’s “Most important chapter in my book” post. As with Dalio, keep your investor hat on and listen from the perspective of understanding the potential moves that the administration may make.

Lutnick gives us a candid inside view of potential solutions to our debt problem. I’ve been talking with my brilliant network about their thoughts on getting out of this debt and entitlement mess. I must admit, I was at peace for the first time (debt reset hope) after listening to Lutnick’s ideas. Can many of them get implemented? With great hope, I’ll keep watch.

I believe Treasury Secretary Scott Bessent completely understands how economic systems work. He gives me hope… I put him in the plus column. I put Commerce Secretary Howard Lutnick in the plus column, too.

If you don’t understand the significance of our massive debt mess, then none of what I’m writing about will make sense. We’ll get through this. I like the idea of getting through it well.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

What’s The Trade?

Back to my friend and our chair lift discussion. After discussing the end of a long-term debt cycle and the coming debt restructuring, he looked at me with his private equity hat on and asked, “OK, what’s the trade?”

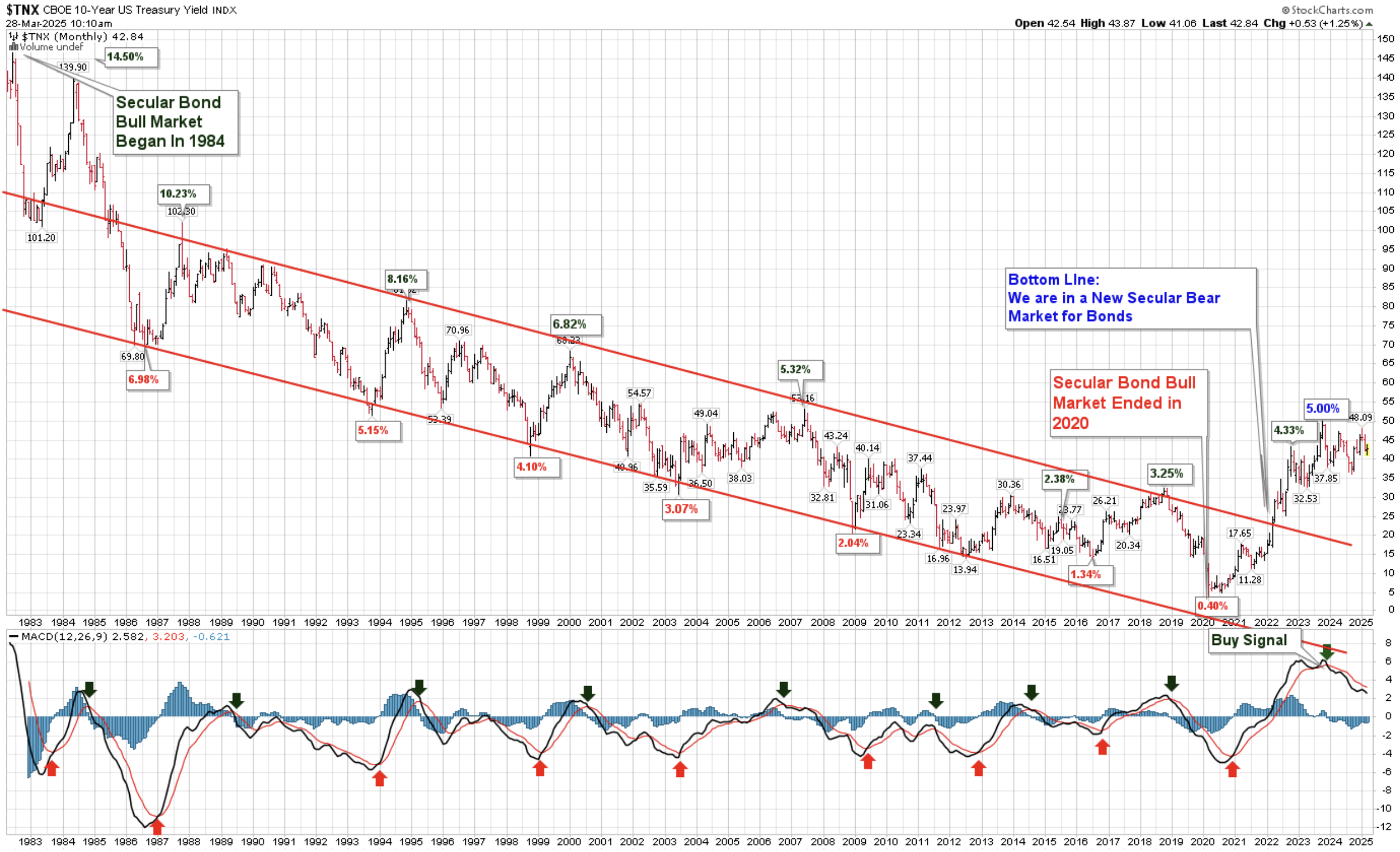

Investing is a probability game, and the big plays come around infrequently. For example, shorting the subprime mortgage market in 2007-08, and going long any risk in the early 1980s when Treasury yields rose to 15% were no-brainers, though there were many reasons to feel concern for those living through it at the time. Add shorting long-term Treasury bonds in the summer of 2020, when the 10-year Treasury yield was less than 1% and the government money spigots were turned on.

If Dalio is correct, and I think he is (no guarantees), the U.S. and other countries will continue to inflate their way out of the debt crisis. Currencies will be debased, and we’ll experience a series of waves of inflation. Imagine the 10-year Treasury Yield in the 7%, 8%, or even 10% range. Inflation could exceed 10%, and buyers of Treasury debt could revolt.

The 10-year Treasury Yield went from 5% to 2% in the last Big Short subprime crisis from 2007 to 2009.

Currently, the 10-year yield is 4.30%. I believe it will decline to 3.25% in the coming recession. The key at that point will be policy response. Based on history, it is probable that policymakers will respond by printing more money. I believe the long-term bull market in bonds ended in 2020. We broke above the down trendline in early 2021, and the dominant direction in yields is up.

What’s the trade? I answered my friend, saying, “Shorting the long-duration U.S. Treasury Zero Coupon bonds when the 10-year reaches the mid-3 % range.”

The Monthly MACD is currently signaling lower yields. The same is true for the Weekly MACD. The entry point, in my view, comes in the next recession. Not today.

NOTE: NOT A RECOMMENDATION FOR YOU TO BUY OR SELL ANY SECURITY. THIS IS FOR DISCUSSION PURPOSES ONLY.

Stockcharts.com

Gold has been on a fantastic bull market run. I remain bullish on both Gold and Bitcoin.

Diversification is essential as every asset is a risk asset—size various positions based on risk tolerance, goals, and income needs.

I favor short-term private credit, specifically niche lending strategies with interest rates that fluctuate with the base lending rate (SOFR). If inflation moves higher, SOFR moves higher, and your yield increases. If I’m entirely wrong in my view that interest rates move higher, then our floating rate investments float lower but still pay a relatively better payout. Doing this removes the loss of principal risk that comes with fixed-rate bonds when interest rates rise. Many private credit funds yield in the 9% to 15% range.

Avoid overvalued, overweight, overconcentrated cap-weighted index funds. If Dalio’s “End of Debt Cycle” or Scott Bessent’s “Grand Global Reordering” proves correct, a severe bear market lies ahead. I would argue that most private equity funds are overvalued. Avoid private credit funds that are tied to leveraged buyout deals... That is likely to be dangerous.

Yet, not everything is overpriced. Cash provides optionality. There is a reason why Warren Buffett is sitting on record amounts of money.

As his late great partner, Charlie Munger, said, “The big money is not in the buying and selling, but in the waiting.” There will be great businesses to buy at reasonable valuations in the next major market dislocation. I have a shopping list of high and growing dividend companies I’m interested in, along with some of the popular names you know well. I’m just waiting for the bear market to stabilize valuations. When? Don’t know.

Other niche plays include small modular nuclear, natural gas, oil, commodities (especially agriculture), base minerals, gene editing, AI, and robotics. Select international markets are undervalued-to-fairly valued.

Yet, back to my friend’s question, what’s the trade? This time, it is not subprime mortgage bonds; I think it is shorting the debt of the U.S. and developed world governments.

The Big Short Part II: It may just be the biggest bubble of all time.

Investor hat still on - see opportunity, not fear. Risk management is at the top of my mind. I hope I’m wrong; I want to be prepared if I’m right.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: Update – March 27, 2025

March 12, 2025 -- S&P 500 Index 5,599

“Stay on top of the current market trends with Trade Signals.”

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.”

– Charlie Munger

Trade Signals is Organized in the Following Sections:

Market Commentary

Trade Signals - Dashboard of Indicators

Market Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

Market Commentary

Sharing with you an updated look at the Weekly MACD trend signal for the 10-year Treasury Note Yield.

Here is how to read the chart:

The green arrow in the bottom right indicates that the current yield trend is down.

The yellow zone is what I’m calling the next recession target zone. 3.25% is a technical target that I believe is probable. No guarantees. I could be wrong.

The monthly MACD long-term trend chart, shared above, reflects the dominant trend.

Source: Stockcharts.com

Bottom line: The trend remains bearish for U.S. equities. Value-oriented stocks are holding up well. Expect inflationary pressures from tariffs, an economic slowdown, and weaker corporate earnings. The risk of recession remains high.

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Snowbird Photos and Ghibli

“When government, in pursuit of good intentions, tries to rearrange the economy, legislate morality, or help special interests, the cost comes in inefficiency, lack of motivation, and loss of freedom. Government should be a referee, not an active player.”

— Milton Friedman

We spend a lot of time debating things in our family. Time skiing and being together in Snowbird, Utah, has been fantastic. My son asked a question that many are thinking: Why don’t we tax all the billionaires to solve the debt problem?

Here is the back of the napkin math: We are nearly $37 trillion in outstanding U.S. government debt. We take in ~ $5 trillion in tax revenue annually and have been spending ~ $7 trillion annually, $ 2 trillion more annually than we take in. We have a spending problem.

The latest available data shows that the combined wealth of all the billionaires in the United States is approximately $6.72 trillion. This figure comes from an analysis of Forbes wealth data at the close of 2024, which reported 813 billionaires in the U.S. with this total wealth. Source

Suppose we tax all the billionaires 100% of their $6.72 trillion wealth. That would cover the $2 trillion in excess spending for approximately 3 years.

A growing problem with all that debt is that it is being refinanced at higher interest costs. The annual interest cost on all the debt is ~ $1.2 trillion. Approximately $9.2 trillion of U.S. government debt is due to mature or must be refinanced in 2025. The annual interest cost is the spark that lights the reset fuse.

Tax 100% of the billionaire’s collective wealth, and we barely scratch the surface. And where might that money run to before the confiscation?

How do we solve the problem? The ‘can’ has been kicked down the road about as far as it can go. We have an out-of-control spending problem, an enormous debt issue, entitlement budget issues, and rising interest expense issues, and it is likely to come to a head over the next five years (my best guess).

Reason for Hope

On my plane ride west, I listened to the All In interview and then closed my eyes. I loved what I heard—some intelligent ideas. I believe there is a way out of this mess. Some turmoil, no crash. Bottom line: there is reason for hope. Whether we size the moment is another issue. Not all will agree.

I will bullet point out some of Howard Lutnick’s ideas next week, and we can use them as a blueprint of sorts to help us gauge probable outcomes.

Since my job is in the investment business, I view things based on my understanding of how systems work. Right now, I see a high recession probability, followed by more money printing, more debt, higher inflation, and higher interest rates. If Lutnick succeeds, conditions may improve. Of course, there is no guarantee. Everything in life involves risk.

Snowbird and Ghibli

It’s been spring skiing conditions all week. Sunny with temperatures in the mid-50s. Miracle March (over 10 feet of snow) left us with a solid base but shortened the time on the mountain. The best window to ski was from 10 am to 2 pm. There is a point when the snow softens perfectly, called corn snow, where turning on the edge of your skis is a fun ride. But when corn snow turns to mush, the snow becomes too sticky to enjoy.

The following are a few pictures from the mountain. Brianna and her friend turned us on to a new AI tool called Ghibli that turns your photos into the animation style of Studio Ghibli.

It’s about a seven-minute tram ride to reach the top of Hidden Peak at 11,000 feet. A few yards away from the group photo is where we placed my father’s ashes. He passed in 2011. He got my siblings and me into skiing at an early age, and we did the same with his grandchildren. It’s been a wonderful experience for all of us.

I’ve been coming to Snowbird since the age of 18. Dad was a CPA, and one of his clients moved to Salt Lake City, and he would fly out to do the doctor’s annual audit. Next week, I turn 64 and haven’t missed a year since 1979.

We say a prayer for Pop and head down the hill. One of our favorite runs, we decided to name Pop’s Path. I like that—a big hat tip to my old man.

The depth of real wealth is measured in love, not money. Hug the ones you love most, life moves by much too quickly.

Back in the work saddle next week.

All the best to you and yours,

Steve

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201, Malvern, PA 19355

Private Wealth Client Website

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.