On My Radar: Mutually Assured Economic Destruction?

April 3, 2026

By Steve Blumenthal

“The standoff over Kharg Island has evolved into the ultimate game of mutually assured economic destruction. We were looking at a scenario where both Washington and Tehran are actively threatening a literal “scorched earth” policy over a 5-mile-long, twenty-square-kilometer piece of coral.”

— Dr. Pippa Malmgren, Source Substack

Twenty percent of the world’s oil supply runs through the Strait of Hormuz. How does the world adjust to the loss of 20 million barrels per day? At what price must oil rise to destroy the demand for oil? To put this into perspective, back in 2020, during COVID and the global shutdown that followed, oil demand declined by 8.1 million bpd. We are potentially destroying double that amount. Source: S&P Global

From Pippa, “Kharg Island is now in the spotlight because Kharg Island is the ultimate “single point of failure” for the Iranian regime. If the islands in the Strait of Hormuz are the weapons Iran uses to project power, Kharg is the vault that funds them. It contains a massive storage buffer of over 30 million barrels. To put it bluntly: whoever controls Kharg Island controls the financial oxygen of the Islamic Revolutionary Guard Corps (IRGC). Without the revenue flowing through those deep-water berths, the regime cannot fund its internal security apparatus or its regional proxies.US Marines are seemingly on the way. Iranian IGRC forces have been rushing in (Man) shoulder-fired surface-to-air missiles (MANPADS) to the island and actively laying anti-personnel and anti-armor mines along the beaches and possible landing zones to repel the potential US Marine assault. Now they hear the American President scolding allies for failing to show up in time and urging them to “take” Iran’s oil and gas while they can.”

While I have been and remain fundamentally bullish on oil, what wasn’t captured in my view was a war with Iran and the risk of a closure of the Strait of Hormuz.

“The standoff over Kharg Island has evolved into the ultimate game of mutually assured economic destruction. We were looking at a scenario where both Washington and Tehran are actively threatening a literal “scorched earth” policy over a 5-mile-long, twenty-square-kilometer piece of coral. Iran has a massive coastline, but almost all of the water along the mainland Persian Gulf is entirely too shallow for Very Large Crude Carriers (VLCCs)—the massive supertankers required for global export.

Kharg Island, sitting about 20 miles offshore, is a geological anomaly surrounded by naturally deep water. Over the decades, Iran has routed massive subsea pipelines from its inland oilfields directly to this 5-mile strip of coral. Because of this depth, it is the only place where Iran can efficiently load its crude onto the world’s largest ships. The U.S. has explicitly stated that if Iran continues to choke off the Strait of Hormuz, the American military will drop all “decency” and completely wipe out the oil infrastructure on the island (TIME: Kharg Island in Sights). Seizing or destroying it isn’t about capturing territory; it is about permanently amputating the IRGC’s primary financial circulatory system. Iran’s doctrine dictates they will sabotage and destroy their own oil infrastructure rather than hand the leverage over to Washington.

Furthermore, their “scorched earth” strategy extends beyond the island: Iranian leadership has declared that if they lose Kharg, they will unleash relentless, unrestricted attacks on the vital energy infrastructure of neighboring Gulf countries like the UAE and Saudi Arabia (The Cradle: Iran Mobilizes for Ground Assault). If Iran goes down, they plan to take the global energy economy and millions of civilians who need water (H20) with them. The fight is over control of the molecules that pass through these waters and these facilities. The hostage here is all of us. Iran’s bet is that we can’t survive without these molecules of oil, gas, petroleum byproducts, and drinking water. America’s bet is that this event is so important that it will quickly catalyze the necessary shift in global demand to American molecules and to a new era of energy from atoms.” Wrote Pippa. Subscriber to her Substack here.

The following is an excellent update I received yesterday from RG Partners, one of our oil investments.

“Oil prices surged sharply on April 2, with WTI climbing as high as $111+. The move was driven primarily by escalating geopolitical tensions after President Trump confirmed the U.S. would continue military strikes on Iran over the next two to three weeks. The lack of a clear timeline for de-escalation has shifted market sentiment, with traders now pricing in a prolonged disruption rather than a short-lived conflict.

A central concern is the effective disruption of the Strait of Hormuz, a critical chokepoint responsible for transporting approximately 20% of global oil supply. Recent missile attacks on energy infrastructure and tankers have heightened fears of broader supply interruptions. While physical supply losses remain limited for now, the market is rapidly embedding a geopolitical risk premium tied to the potential for further escalation or direct damage to oil infrastructure.

Market dynamics are reinforcing this uncertainty. Notably, WTI briefly traded at a premium to Brent, an uncommon occurrence, signaling tightness in near-term U.S. supply and heightened demand for prompt delivery. While U.S. producers have begun modestly increasing rig counts, the response remains cautious and insufficient to offset near-term risks. Forward outlooks vary widely, with estimates ranging from ~$95/bbl in a normalization scenario to $120–$130 in the near term, and potentially above $150 if disruptions to the Strait persist into mid-May.

The trajectory of oil prices will largely depend on how quickly tensions de-escalate and whether the Strait of Hormuz reopens. A resolution within weeks could quickly compress the current risk premium and push prices lower, while a prolonged conflict or escalation involving infrastructure damage would likely sustain elevated prices. In the meantime, global markets, particularly Europe, are expected to begin feeling economic impacts as existing supply buffers diminish.

For RGP, this environment is supportive. Higher and sustained oil prices directly enhance the economics of domestic production, improving cash flows, margins, and the value of existing reserves. In addition, geopolitical instability reinforces the importance of U.S.-based energy assets.” Sources: RGP, “Oil Prices Surge 7% as US Maintains Pressure on Iran.” GlobalData, 2 Apr. 2026, HE: Crude Oil Jumps 11%.” Hart Energy, The Washington Post. “U.S.-Iran War and the Future of the Strait of Hormuz.” 2 Apr. 2026

My Camp Kotok fishing friend Jim Bianco summarized the Iran challenge this way: “On April 1st, Trump threatened to bomb Iran back to the Stone Age if they don't reopen the Strait within weeks. It's the classic 20th-century playbook: overwhelming offense force, massive bombardment, industrial-scale destruction. The problem? That playbook doesn't work against distributed, cheap, rapid-iteration systems—especially when your enemy is organized under a mosaic structure.

Iran's "Mosaic Defense" doctrine is a decentralized command system where authority and capability are distributed across multiple geographic and organizational nodes. Each region operates semi-autonomously with overlapping chains of command and pre-planned contingencies. It's designed so that when you destroy the center, the edges keep fighting. You cannot decapitate a system with no head. You cannot out-bomb your way to victory when your enemy is not centralized; this was the solution for 20th-century industrial warfare.

Why We're Stuck

Whether you viewed this as a war of choice or not, it has now become a war to keep global trade open. This is precisely why the US cannot declare victory and walk away from the Strait of Hormuz— or TACO.”

You can find Jim’s full post here.

We appear to be nearing a tipping point. Is there a global realignment being negotiated behind closed doors that may prevent a global economic crisis? We may soon find out.

Grab that coffee and find your favorite chair. The above is depressing, and sadly, it is our current state. Let’s shift our thinking and focus on potential opportunities. Valuations can help in this regard. If a recession is afoot, keep in mind that among bear markets since 1946, the average decline during a recession has been 35.8%, compared with 27.9% in non-recession bear markets. Source

Today, you’ll find the most recent quarter-end valuation data, and let’s consider potential buying levels if a recession-driven bear market takes hold. Also, you’ll find a chart of the Mag 7's performance relative to the S&P 500 Index since the market peak (Trade Signals section). Worth a look. Finally, our good friend Barry Habib talks about the job numbers out this morning. Hint: don’t buy the BS coming from the BLS.

On My Radar:

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

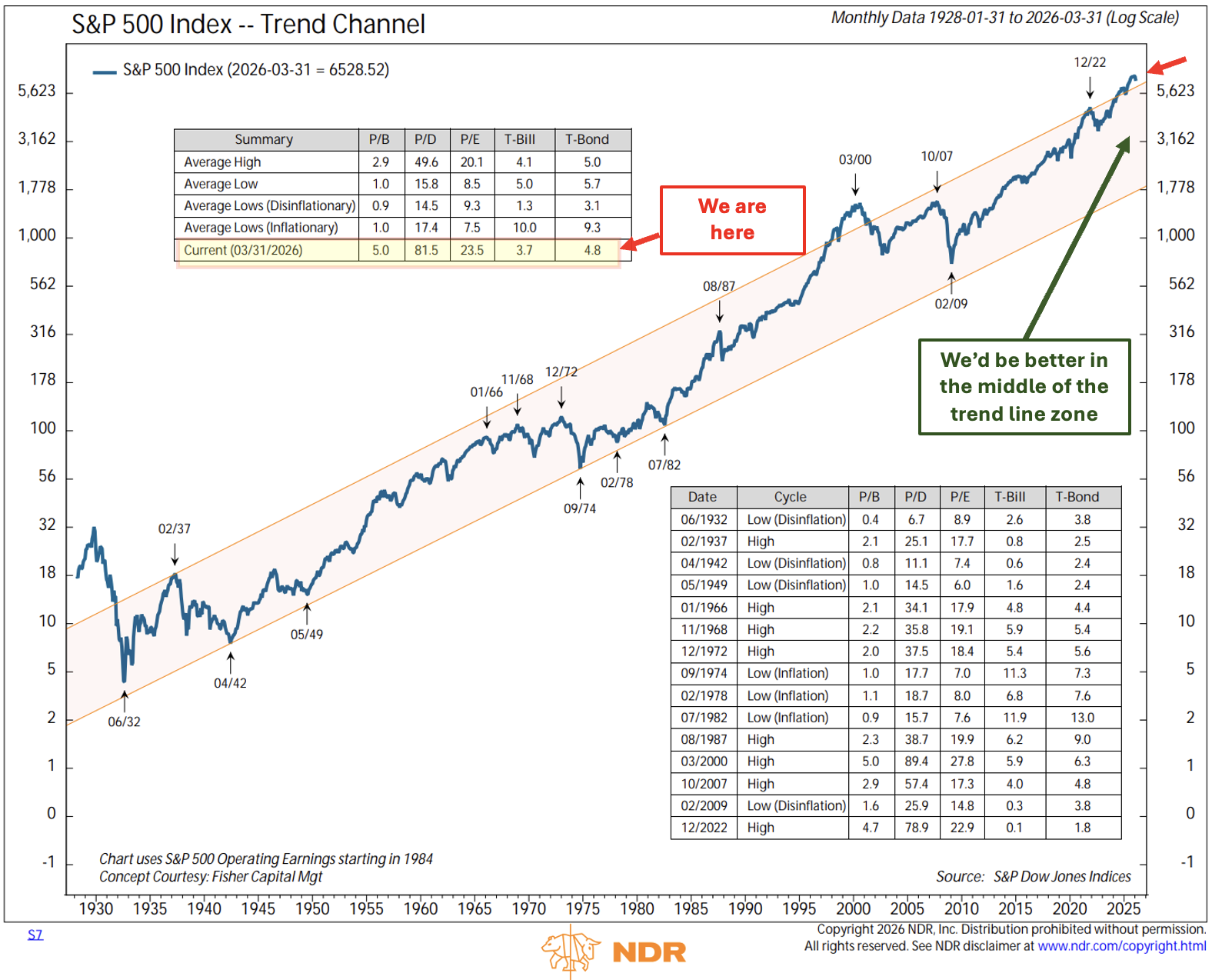

Valuations Targets

I love this Trend Channel chart from NDR.

Here is how to read the chart:

Red arrows indicate our current state.

The upper right-hand arrow shows we sit well above the upper trend line.

Compare the P/B (price to book), P/D (price to dividend), P/E (price to earnings) to the prior “Average High.”

P/B, B/D, and P/E are all higher than Average High

All are higher than the highest high except for March 2000

Next, compare the current numbers with the other market peaks listed by date in the lower-right data box.

Finally, view the “Cycle” low data in the lower-right data box to get a sense of other historical lows (buying opportunities).

Note: This is absolutely impossible to time. But if you can game plan a probable risk-on buy range, I believe you’ll be better prepared to act when everyone else is panicking. You’ll know we are there when you want to throw in the towel and sell everything you own. You won’t be immune to the fear. Use it as a trigger and do the opposite!

Source: NDR, CMG annontations

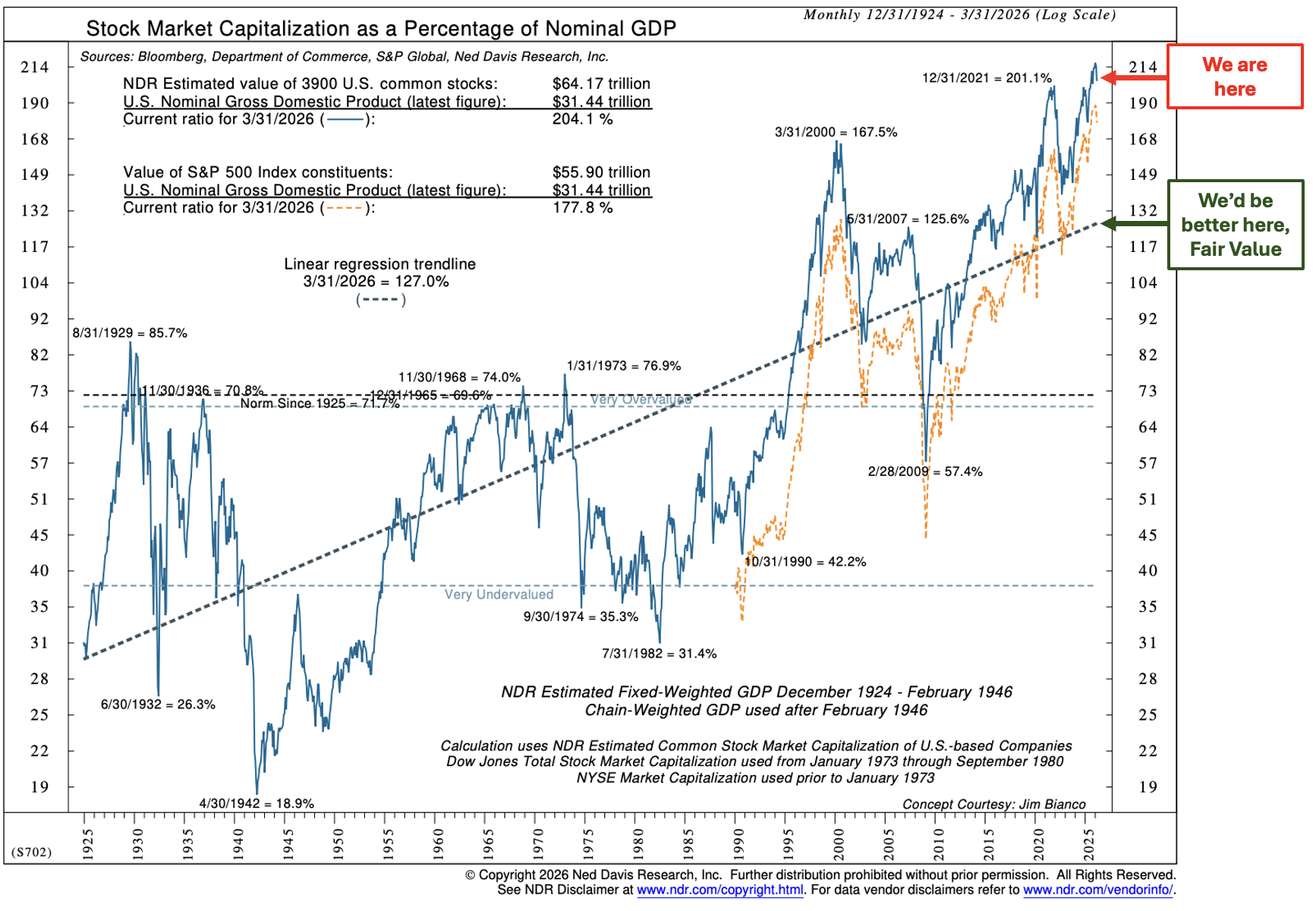

The Buffett Indicator

Source: NDR, CMG annontations

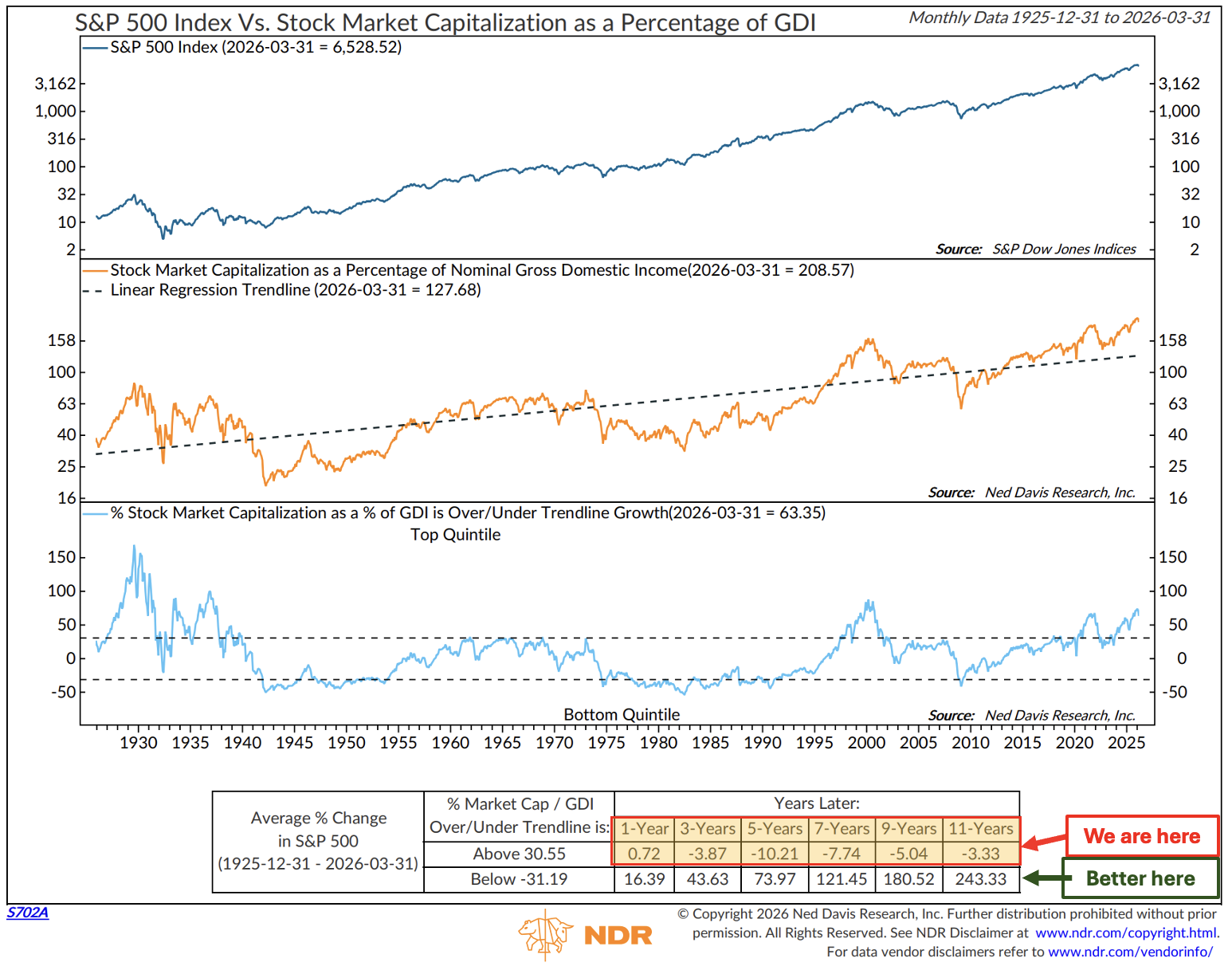

Another favorite of mine is the total Stock Market Cap to Gross Domestic Income.

The key here is to look at the blue line in the lower section.

The current ratio is well above the historical trendline.

I’m looking for a reversion to the historical trend line.

Source: NDR, CMG annontations

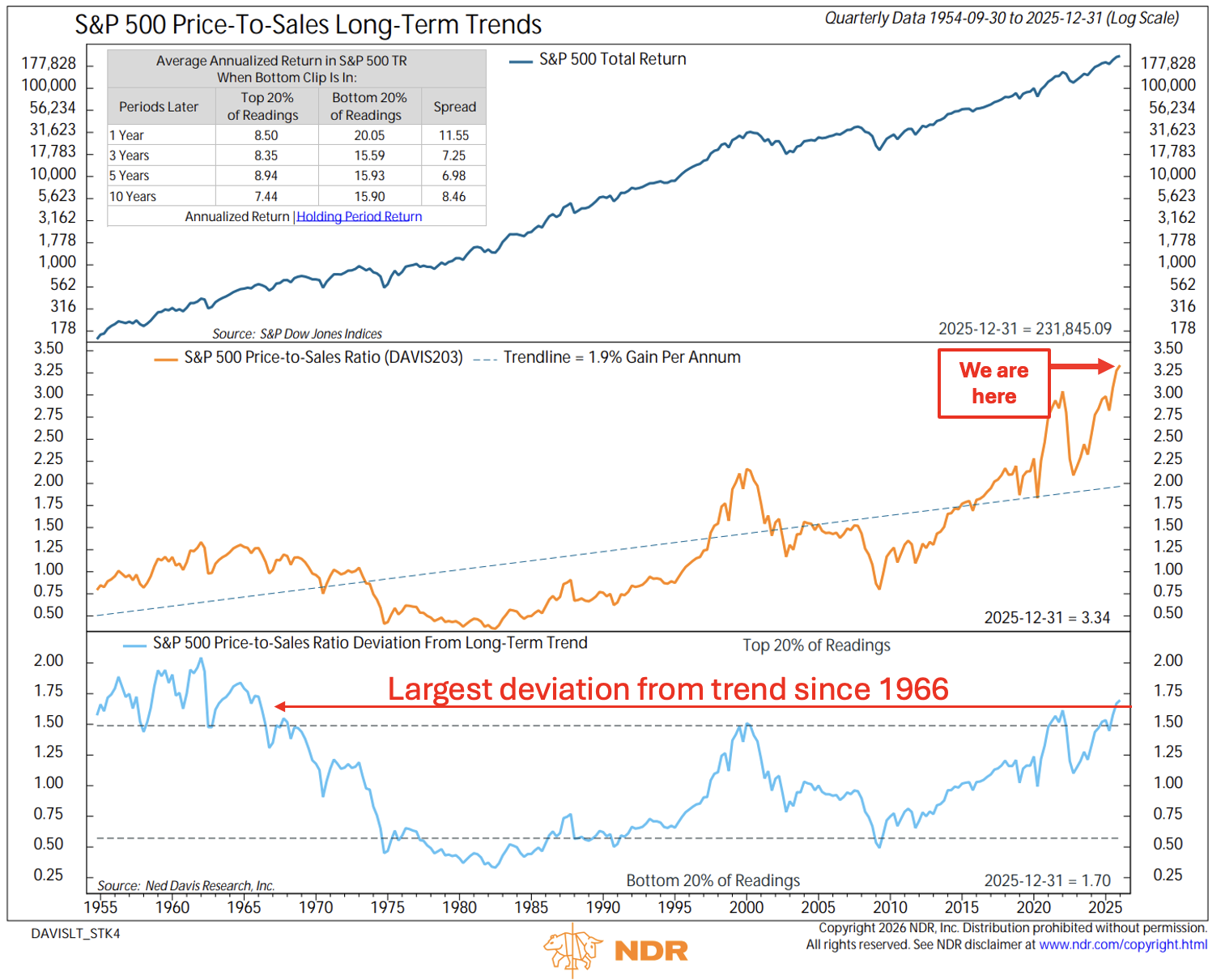

Price to Sales

The market is extremely overvalued by this measure

Source: NDR, CMG annontations

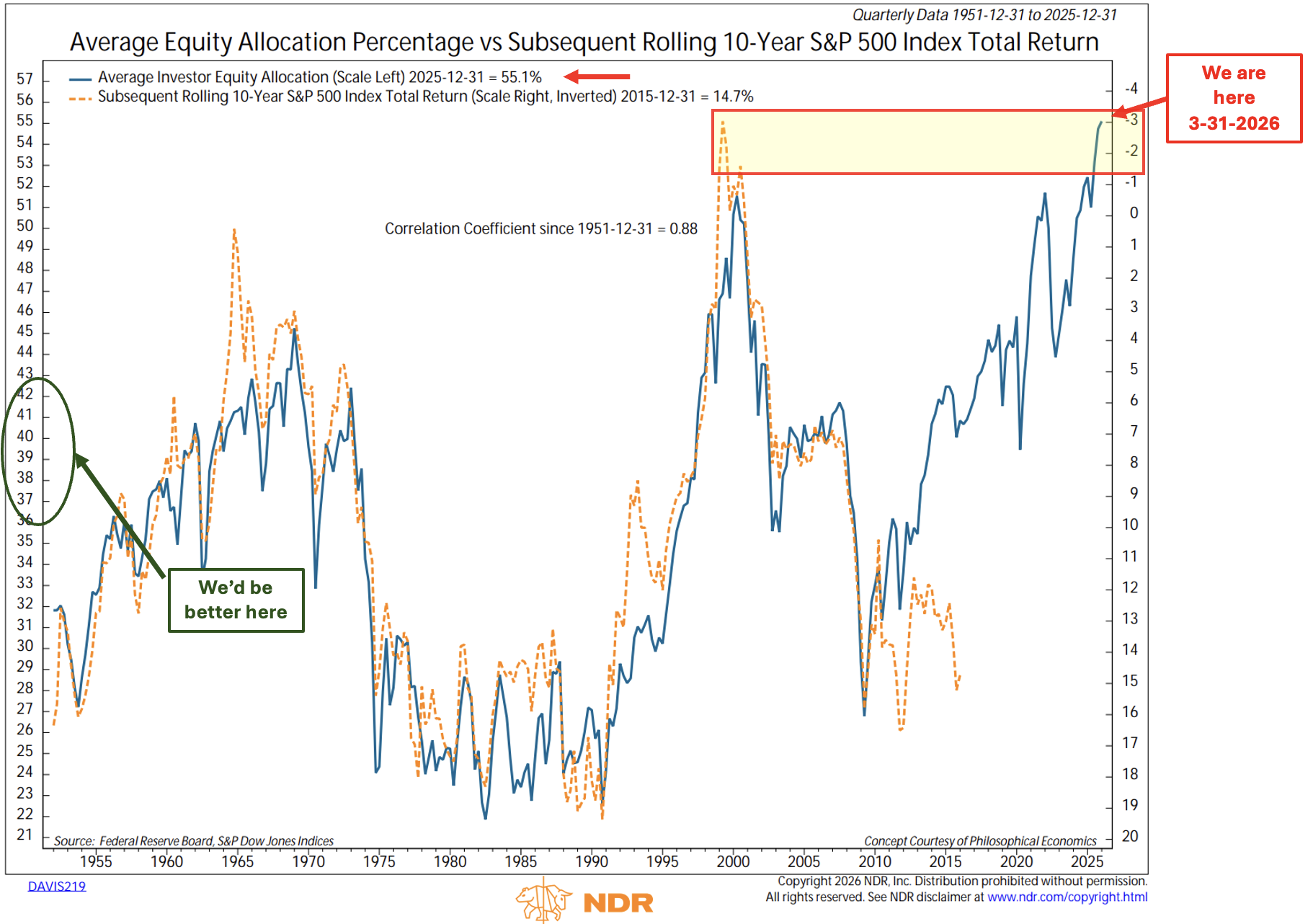

Average Equity Allocation Percentage vs Subsequent Rolling 10-Year Total Returns

The average investor equity allocation as of the latest data (12-31-25) is 55.1%. That is higher than any reading dating back to 1951.

The orange line plots the actual 10-Year rolling returns. You can see it stopped 10 years ago, since that is the last known data point.

The key point here is the high correlation between high equity allocation percentage to low subsequent 10-year returns and low equity allocation percentage to high subsequent 10-year returns.

Think about it this way. When investors are fully invested, they have less money available to buy stocks. At some point, bond yields may be high enough to pull money out of stocks and into bonds.

Source: NDR, CMG annontations

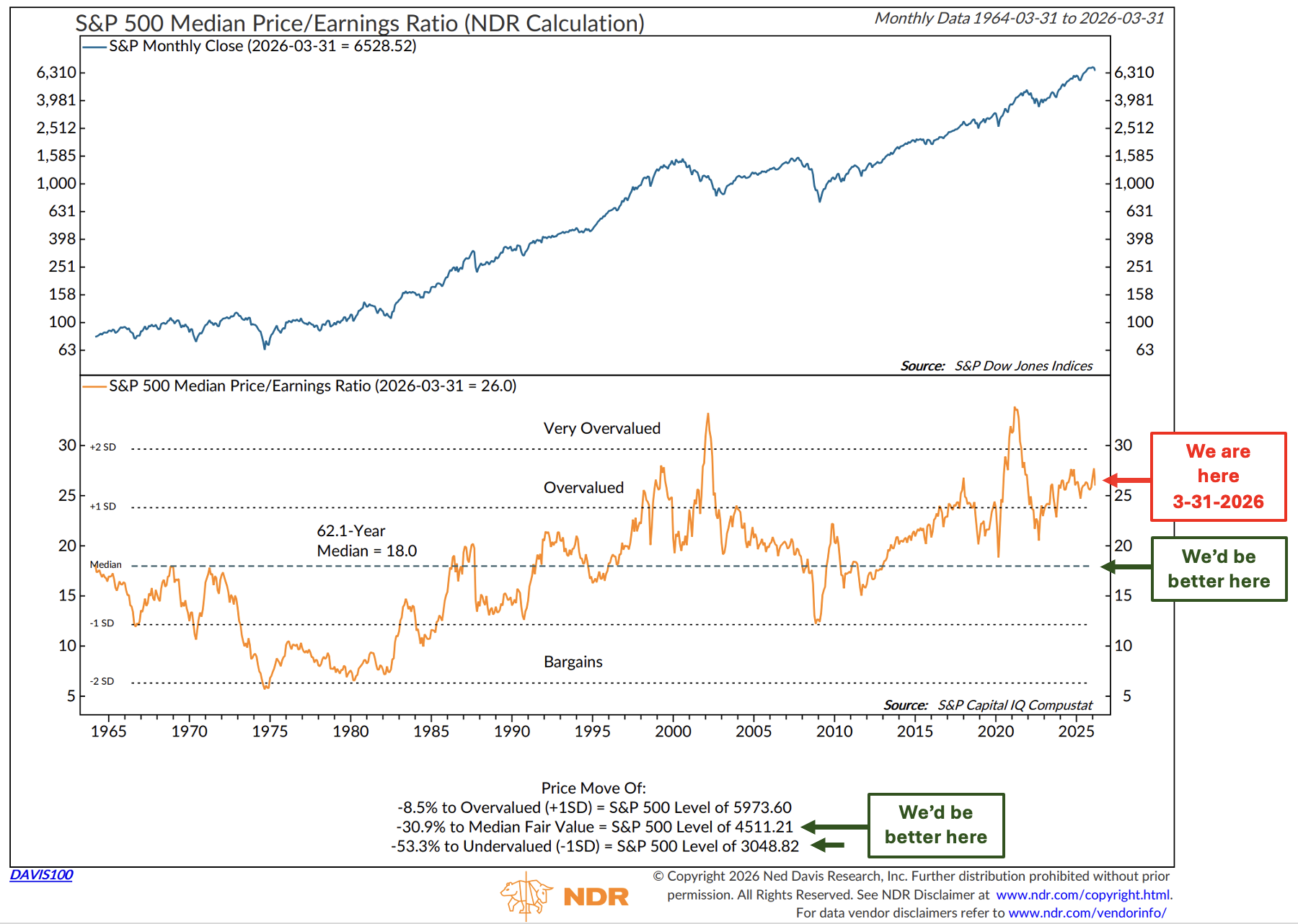

Finally, Median PE is Lower than last month but still too high

Median Fair Value is 4511.21 at March 31, 2026, month-end (dotted line, green “We’d be better here” arrow).

An additional 30.9% decline is needed.

Source: NDR, CMG annontations

Interesting Charts

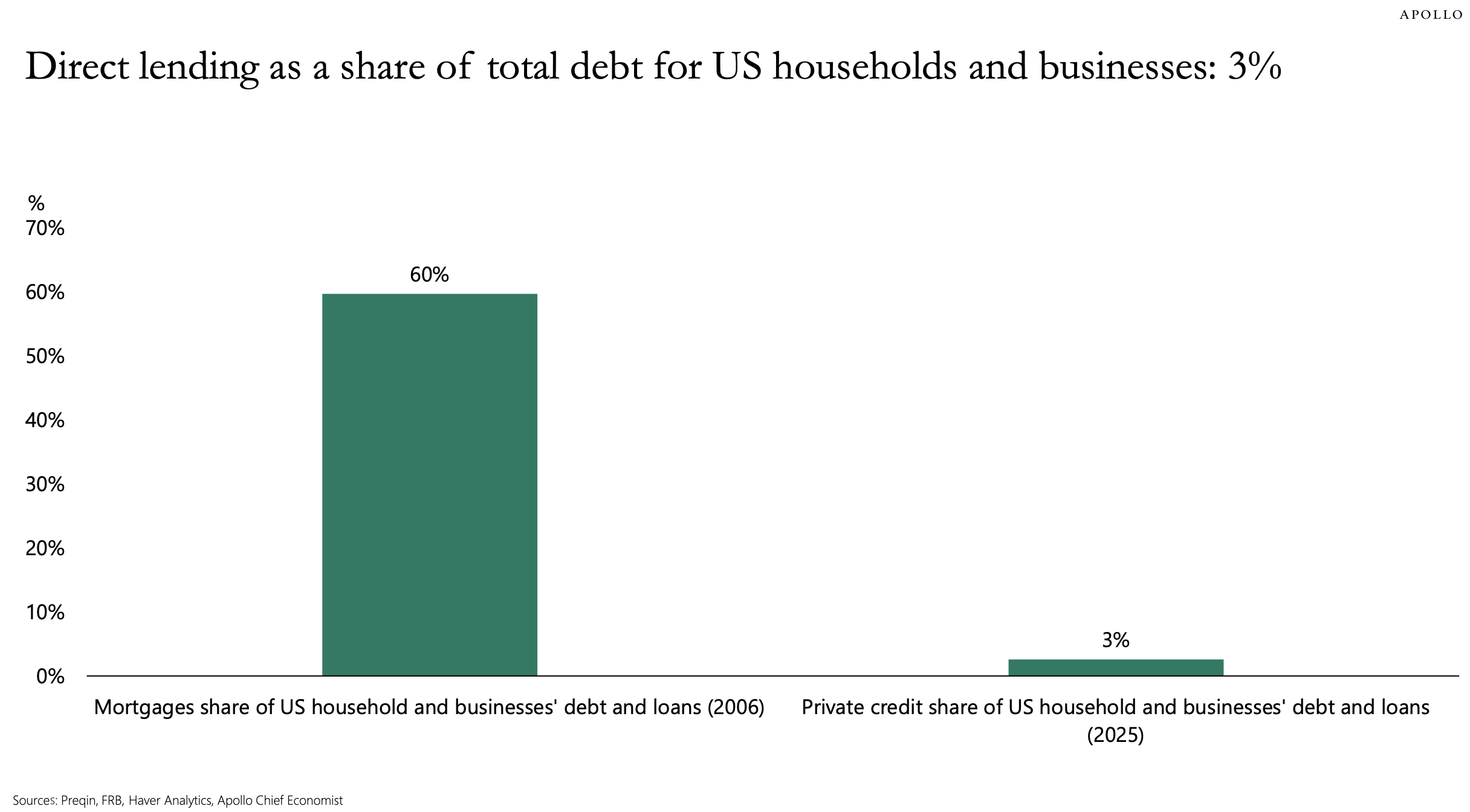

As a follow-up to last week’s post on Private Credit (here), I maintain that there is no systemic risk associated with private credit.

The following shows mortgages’ share of US household and business debt and loans (2006) vs. Private credit share of US household and business debt and loans (2026):

Source: Apollo

What About Bonds as a “Safe” investment?

Still too much government debt to be refinanced this year (approximately $10 trillion)

Deficit spending remains out of control

More money for printing is probable, which drives inflation and interest rates higher

Bonds don’t do well in rising interest rate environments

At some point in the future, bonds will be attractive again

While private credit, like bond investing, is not risk-free, there are advantages to the floating-rate structure of loans in a higher-for-longer interest-rate environment.

Source: X, @charliebilello

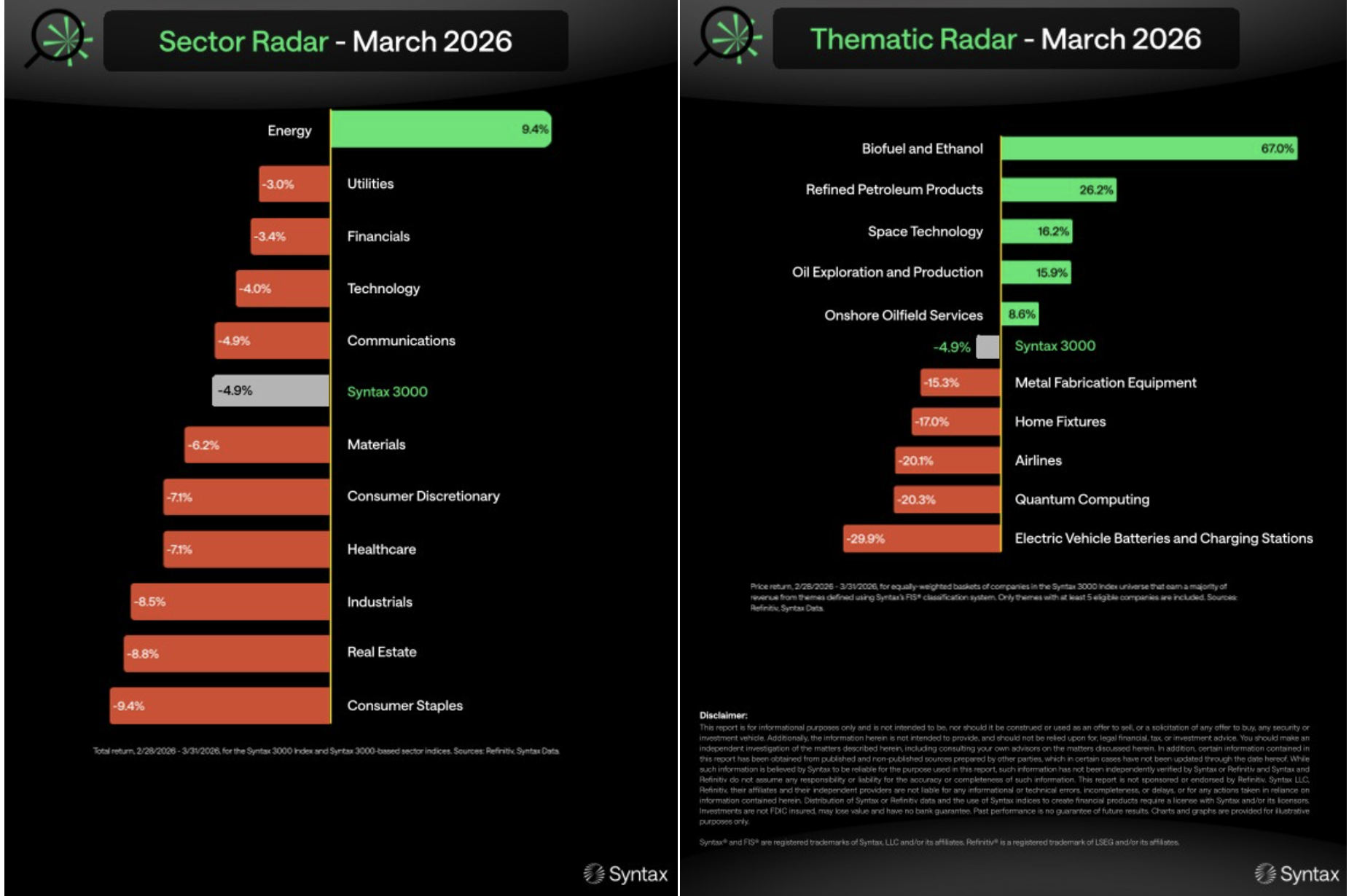

March 2026 Sector Performance - Got Energy?

Source: LinkedIn, Syntax

Oil Prices and Inflation

Wave two of inflation is upon us

Source: X, @KoveissiLetter

BLS At It Again with Nonsensical Report 4-3-26

Worth the short watch. Click on the photo. Barry is the man.

Source: MBS Highway

As always, this is not investment advice. For discussion purposes only.

Views are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. See important CMG disclosures below.

If you like what you are reading, click on the following link.

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: April 2, 2026 Update

Market Commentary

The significant economic and market risk remains the Strait of Hormuz. The risk of recession within six months is high. The economic impact of losing 20% of the global oil supply is material. I don’t yet see recession risk in the lagging indicators I follow each week, but this risk is unprecedented. Lights on!

Drawdowns from Jan 2026 Highs

“The S&P 500 is only down 9% from its January high. But 6 of the 7 members of the Magnificent Seven are already in bear markets.” This is likely to shake investor confidence and potentially spending patterns.

@PeterMallouk

Source: GeminiAI, @PeterMallouk

Trade Signals - subscribers only

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

Not a recommendation for you to buy or sell any security. For information purposes only. Outlook and viewpoints are subject to change at a moment's notice. This material is for discussion purposes and does not give you specific advice. Please discuss needs, goals, time horizons, and risk tolerances with your advisor. Important disclosures.Not a recommendation for you to buy or sell any security. For information purposes only. Outlook and viewpoints are subject to change at a moment's notice. This material is for discussion purposes and does not give you specific advice. Please discuss needs, goals, time horizons, and risk tolerances with your advisor.

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Happy Easter

Three of our six children are coming home for the weekend. A big dinner is planned for Sunday night.

I’ll be at Augusta National for The Masters practice round on Tuesday, walking the course with my investment hero, Mark Finn, along with a few very good friends, Mike F, Joe Q, and Terry T. The Masters tournament begins next Thursday. No, Tiger, as I’m sure you are well aware. I hope he can get himself together. We all need help sometimes, and sometimes big help. Wishing him well soon.

Snowbird, Utah, follows with the kids in mid-April. I’ve been obsessively looking at the weather forecast, and it looks like 30” of new snow. I’m hoping for spring conditions and mid-morning corn snow. The only thing better is a foot or more of fresh soft powder. Fingers crossed.

I’ll be hosting a small dinner for a few clients, friends, and readers at the Steak Pit Restaurant located at the Snowbird resort on Wednesday, April 15, at 6:30 pm. Please email Amy@cmgwealth.com if you are interested in attending.

Family office meetings in Austin, TX, follow later in the month.

The weekend forecast looks warm with some rain. I’ll take warm. The flowers can enjoy the rain.

Wishing you and your family a wonderful long holiday weekend. Let’s hold our glasses high, close our eyes, and see the world in a better place.

Happy Easter!

Kind regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.