On My Radar: Thoughts on Private Credit

March 27, 2026

By Steve Blumenthal

“All U.S. markets will be on chain within two years.”

— Paul Atkins, Securities and Exchange Commission Chairman

The equity and fixed income markets remain under pressure today, despite or perhaps due to Trump's extension of the negotiation deadline. The 10-year Treasury Yield touched 4.45% and is at 4.42% at the time of this writing.

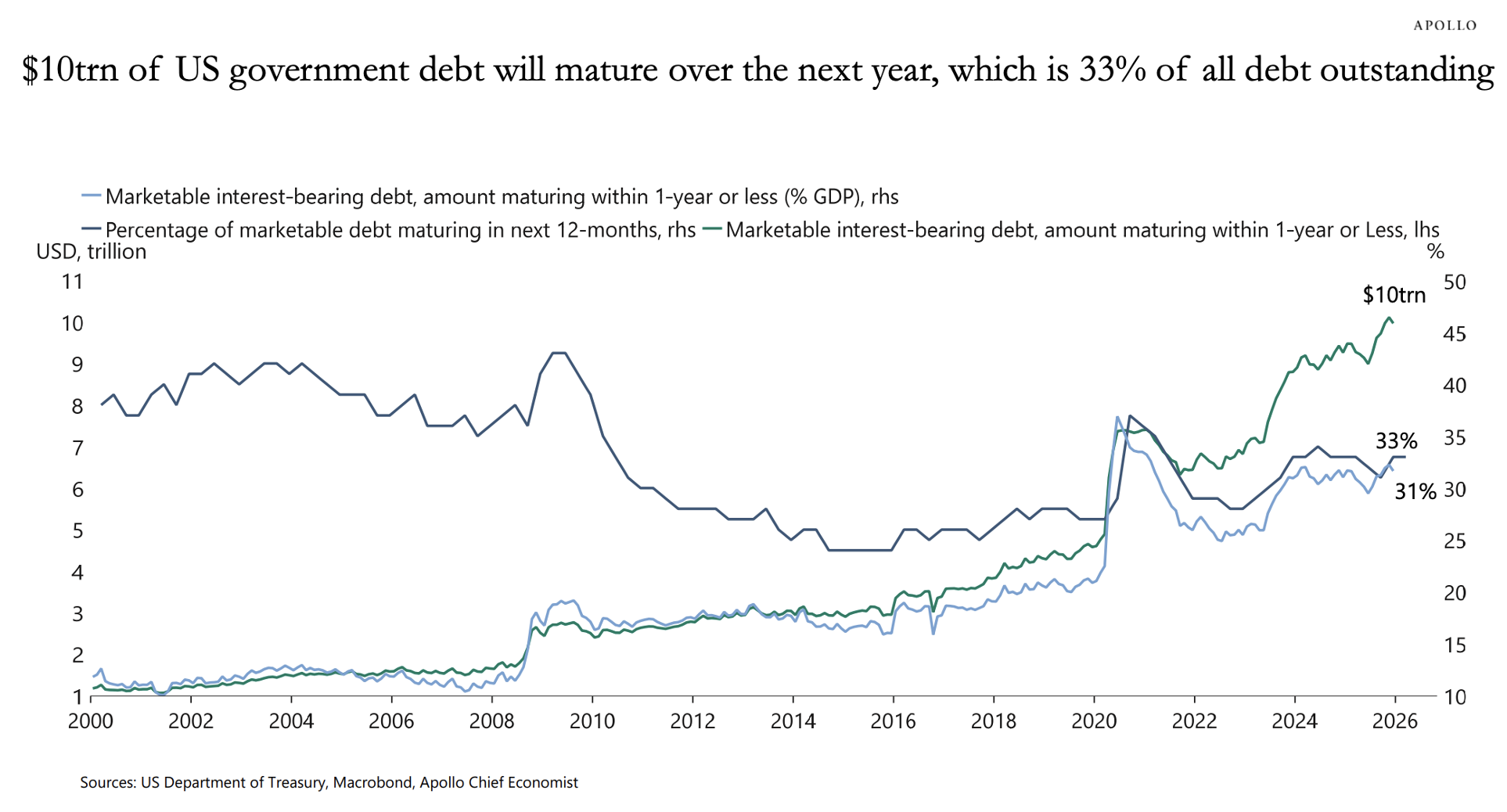

According to Apolo, $14 trillion in investment-grade bond supply is coming to market: $10 trillion in existing US government debt will need to be refinanced over the coming 12 months. Further, the budget deficit this year is about $2 trillion. That too will need to be financed.

Total gross corporate bond issuance in 2026 is likely to be around $2 trillion, driven by increased supply from hyperscalers. Adding it all up, the total investment-grade supply coming to market this year is around $14 trillion.

The bottom line is that the growing supply of investment-grade fixed-income products is putting upward pressure on rates and credit spreads.

Source: Apollo

The current average interest rate on the $39 trillion in outstanding government debt is ~3.3% – 3.35%. That’s the blended rate across all Treasury securities (short-term bills, notes, bonds), not just today’s market rates. Source: Joint Economic Committee

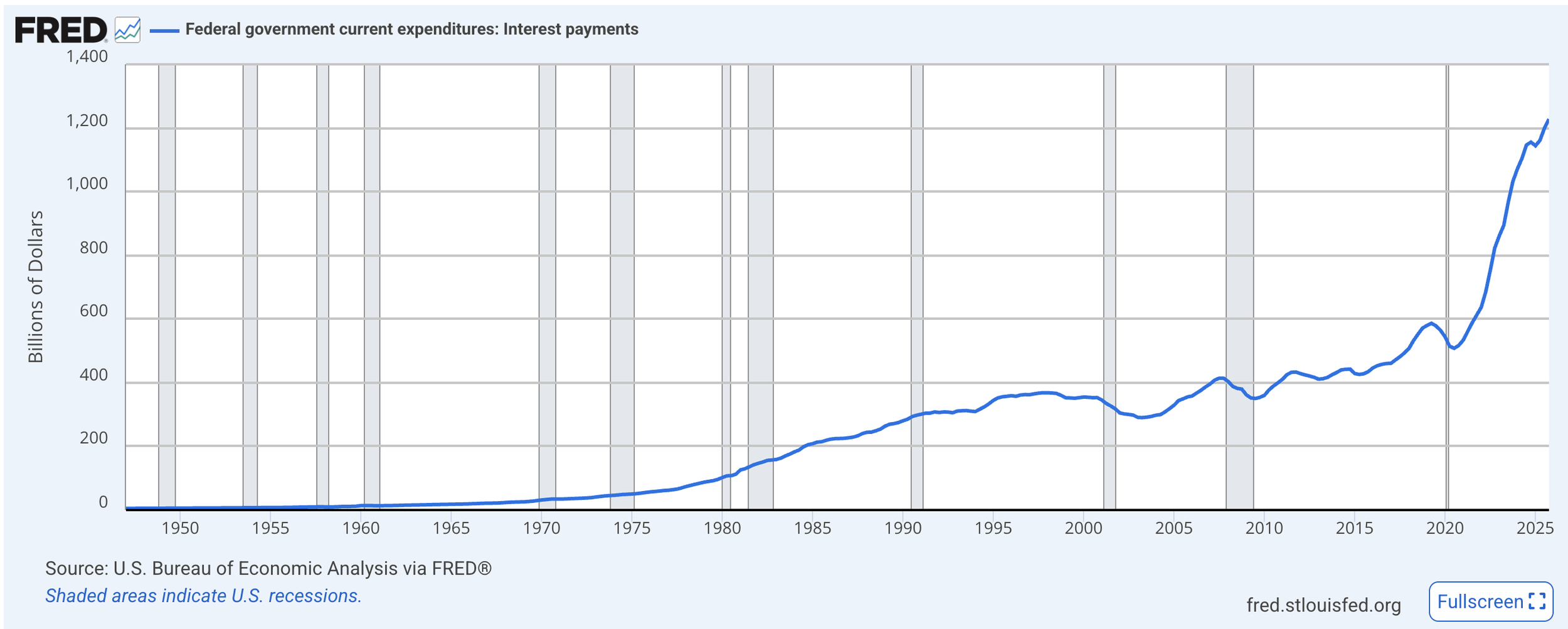

The annual interest expense now exceeds $1.2 trillion.

Source: Fred

Refinancing the $10 trillion due to roll over in 2026 at 4% to 4.5% increases the annual interest expense. Every 1% increase in rates results in ~$300–400 billion more in annual interest expense over time.

This is the trap the U.S. and other developed world governments are in. Higher interest rates coupled with continued money printing lead to higher inflation, which remains my primary economic concern.

Risk remains elevated.

Grab that coffee and settle in. Let’s switch gears and dive into the tumult you are reading about in the private credit markets. Some of it for good reason. Much of it is overblown. Full cup, let’s go.

On My Radar:

Personal Note: Tokens, The Masters, and Snowbird

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

Thoughts on Private Credit

If you've been following financial media lately, you might think private credit is on the verge of collapse. Defaults are coming. Liquidity is drying up. AI is going to blow up every software loan ever made. Retail investors were duped.

I don't buy it. And after spending time with some of the best minds in the private credit business Cliffwater, Apollo, Goldman Sachs, Oaktree's Howard Marks, and Pantheon, I think the pessimism - while not entirely without merit - is being applied with a very broad and largely inaccurate brush.

What Is Private Credit, Exactly?

Private credit is simply lending to businesses outside the traditional banking system. Think of it as being the bank: pooling capital with other investors, extending loans to companies, and collecting interest. Those loans are typically first-lien and senior secured, meaning that if something goes wrong, you're first in line to be repaid. They're generally floating rate, adjusting with interest rates rather than locking you into a fixed yield. In a potential higher inflation/higher interest rate cycle, floating rate yields is an attractive feature. And much like loans that sit on a bank’s balance sheet, private credit loans are illiquid, you can't sell them like a stock.

That last point matters. We’ll come back to it.

What's Actually Happening Right Now

Let's be honest about what has occurred. Blackstone's ~$82 billion BCRED fund received redemption requests above its standard quarterly limits, requiring internal capital support to meet exits. Blue Owl restricted redemptions from its retail-focused private credit BDC entirely, announcing a ~30% return of capital to investors and a subsequent wind-down. These are real events, and they deserve straight talk.

Here is how Pantheon, one of the most experienced private credit and secondaries investors in the world, characterizes them: “These developments reflect investor sentiment toward specific managers and portfolio quality, concerns about valuation accuracy, and heightened liquidity needs in what are fundamentally illiquid, longer-dated assets. They do not reflect structural failure of the underlying loans.”

The headline defaults, First Brands, Tricolor, and now a UK specialist lender, Market Financial Solutions, which entered bankruptcy, share a common thread. Each reflects issues of governance, execution, and probable fraud. This is not a systemic deterioration in private credit quality. Post these events, securitized credit spreads briefly widened and have since retraced as underlying performance data reaffirmed stability.

The lesson from all three situations is the same one that every experienced credit investor already knows: manager selection, loan structures, collateral control, risk sizing (diversification), and ongoing portfolio monitoring are the job.

The Liquidity Question

Much of the current anxiety centers on liquidity or the perceived lack of it. My firm’s view is that illiquidity in private credit is a feature, not a bug. It was disclosed. It was understood.

The issue, where it exists, isn't with the asset class. It's with suitability: putting the wrong investors into structures with timelines that don't match their needs. There's a difference between "this investment is illiquid and I knew that" and "I was told this was liquid and it isn't." The former is a feature of the asset class. The latter is an advisor problem, not a private credit problem.

For investors who don't need immediate access to their capital and understand what they own, the illiquidity premium is exactly why the yields are attractive. That's the deal. We’ll compare private credit relative to other investment options further below (see: A Word on "Safe" Alternatives). It’s important.

What About Defaults?

Yes, there are defaults. There always are. That's not a scandal. No one who has ever invested in corporate credit, high-yield bonds, bank loans, or mortgages has done so in a world without default risk. Default rates are priced in - it's why yields in private credit run meaningfully above investment-grade bonds. Diversification across hundreds of loans is precisely how you manage individual defaults.

Goldman Sachs' John Tousley puts the numbers in perspective: he estimates a maximum 15% default rate in software-related private credit, and roughly 7% overall - with meaningful recovery on workouts given first-lien positioning. Remember that the equity holders take the first 50% hit. Bottom line: Net losses are a fraction of the headline default figure.

The Cliffwater Corporate Lending Fund, one of the largest and longest-running private credit vehicles, with $31.5 billion in assets, has experienced just -0.02% annualized net realized losses since its 2019 inception, against -0.92% for the broader Cliffwater Direct Lending Index. That's not a crisis. That's a well-run lending operation. Source: Cliffwater – Ten Things to Know

The AI/Software Fear

The narrative has morphed from liquidity concerns to fears that AI will obliterate software companies and take private credit down with them.

Here's the logical problem: loans are senior to equity. They're underwritten to earnings. They have significant loan-to-value cushions. Even if AI disrupts a software borrower's business model, the path from "business disruption" to "loan default" to "unrecoverable loss" is a long one, with multiple checkpoints.

Every serious institution I've reviewed agrees on this point. Cliffwater's own analysis shows only ~1% of their NAV is classified as high AI disruption risk, with their tech and software portfolio growing revenue at ~10% and EBITDA at ~12%. Apollo argues that profit pools will migrate toward platforms with structural advantages in data and distribution (the mission-critical, deeply embedded platforms that private credit has historically lent to). Pantheon focuses their software lending on large companies with $1-5 billion or more in enterprise value and EBITDA typically above $150 million, avoiding non-traditional credit metrics like annual recurring revenue (“ARR”) in favor of businesses with strong proprietary data, attractive customer value propositions, and limited competition.

The consensus view is this: the question is not whether AI will disrupt some software companies. It will. The question is which ones and how well they are underwritten. Is your private credit fund lending to durable companies rather than fragile ones? "Software is dead" is a click-bait headline tactic designed to draw in readers. Yes, AI and Claude Code is disruptive but is it more productivity empowering than displacement. I see greater net growth.

Howard Marks' Honest Caution

I want to be fair to the bears, because the most credible version of the concern comes from Howard Marks, and it deserves to be taken seriously.

Marks, co-founder of Oaktree Capital, is explicit: there is no systemic problem with private credit. But he issues a pointed warning. The direct lending market has grown from near-zero to over $1 trillion in roughly 15 years and is approaching $2.3 trillion by some measures. In that time, capital has flowed in fast, and not all of it has been managed with equal discipline. As he puts it, the worst loans are made in the best of times. With 17 years of generally favorable conditions, some weaker underwriting has almost certainly found its way into the system. Source: Howard Marks Memo’s

Pantheon echoes this: credit dispersion among both managers and strategies is increasing, lax underwriting has been exposed in select credits, and risk management practices are coming under greater scrutiny. This is a normal and healthy phase of a maturing market cycle, not a death knell for the asset class. More of a cleansing process, which creates opportunity.

When stress arrives, the question will be: who made the careful loans, and who didn't? This is a manager selection story, not an asset class condemnation. The good managers will be fine. Some won't. Every manager will experience some challenges.

The Bigger Picture: A K-Shaped Credit Market

One of the most important ideas in Apollo's 2026 Credit Outlook is one the mainstream coverage has missed entirely: the defining feature of today's credit environment is not distress, it's dispersion.

Economic strength is concentrating among higher-income consumers and large, AI-exposed corporates, while pressure builds among more interest-rate- and income-sensitive households and businesses. The top 10% of consumers now account for nearly half of all consumer spending. Mag 7 profit margins rose through 2025 while S&P 493 margins declined. Corporate capital expenditure outside of AI infrastructure was essentially flat.

In credit markets, this shows up as a widening gap between high-quality and low-quality borrowers. Aggregate high-yield spreads were roughly unchanged in 2025, but lower-rated CCC bond spreads widened nearly 85 basis points. The headline numbers look fine. Underneath, the sorting has already begun.

Apollo's conclusion: this is not a market defined by forced selling or systemic stress. It is defined by choice. And in credit markets defined by choice, pricing power shifts back to lenders. For patient, disciplined buyers of credit, dispersion is not a warning sign; it's the mechanism through which attractive entry points emerge.

Apollo also flags something worth watching closely: what appears to be diversified credit exposure across sectors may actually be a single, concentrated bet on AI. As hyperscalers fund massive infrastructure buildouts through debt across public investment-grade, private credit, asset-backed finance, and commercial real estate portfolios that appear diversified, they may be carrying a growing hidden "AI beta." Apollo also suggests that for investors seeking genuine diversification, European private credit and assets such as sports financing, which are structurally insulated from the AI arms race, are worth considering. I like the sports financing idea and will have my team dig in.

The Hidden Opportunity

Here's what the bear narrative misses entirely: periods of liquidity stress in private credit don't just create problems. For the right investors, they create opportunity.

Pantheon makes this case compellingly through the lens of credit secondaries; buying seasoned, fully funded private credit portfolios from investors who need liquidity, at discounts driven by that liquidity need rather than any underlying credit impairment. Think of it as buying a good loan at a discount simply because the seller needs cash. The loan hasn't gotten worse. The seller's situation has changed.

The attributes are genuinely attractive: below-NAV entry pricing, shorter duration of two to four years, immediate current income, and enhanced transparency since the underlying loans already have observable performance histories. Vintage diversification smooths cyclical effects. Broad underlying borrower bases reduce idiosyncratic risk. Pantheon estimates a $180-200 billion pipeline in credit secondaries over the next three years, with significant opportunity emerging directly from the BDC and private wealth evergreen market dislocations happening right now.

This is the constructive flip side of the current negativity. The sellers are motivated by sentiment and liquidity needs. The buyers are acquiring quality at a discount. Forced selling creates an opportunity for the buyer.

A Word on "Safe" Alternatives

Before anyone concludes that the solution is simply to retreat to traditional fixed income, consider what the supposedly safe alternatives have delivered.

The Bloomberg U.S. Aggregate Bond Index, the benchmark for most bond funds, has returned just 0.42% annualized over the past five years. Investors in the 10-year Treasury note experienced an approximate cumulative loss of around 6% over that same period as rising rates crushed prices. The Bloomberg Agg carried volatility of 5.79% for a five-year return barely above zero. Source:

Meanwhile, the Cliffwater Corporate Lending Fund delivered 9.92% annualized over the same five years, with a standard deviation of just 1.71% and a near-zero correlation to equities.

Every asset class carries risk. The question is never "is there risk here?" It's always "am I being compensated for the risk I'm taking, relative to my alternatives?" On that basis, well-managed private credit has been a compelling answer for patient investors that the traditional bond market simply does not.

So, Where Does This Leave Us?

Goldman's Tousley frames the near-term outlook well: a little more pain is likely as markets digest excesses, some weaker loans get worked out, and underwriting standards tighten. That's healthy. Apollo agrees that rising supply and wider dispersion are creating a buyer's market where disciplined lenders are increasingly in control of pricing. Tousley's analogy is instructive: this is more Silicon Valley Bank than 2008 Great Financial Crisis. Contained, resolvable, and ultimately constructive for the survivors.

Marks reminds us to stay humble - we won't know whose underwriting was sloppy until the tide goes out. That's not a reason to avoid the asset class. It's a reason to be thoughtful about who manages your money within it.

Pantheon sees continued momentum in private credit across institutional, private wealth, and insurance channels. While volatility and manager dispersion will persist, disciplined underwriting, portfolio diversification, and selective exposure to credit secondary opportunities should enable patient investors to effectively capture the illiquidity and complexity premiums the asset class offers - potentially at better entry prices than were available a year ago.

While no guarantee can be made, I’m confident that when the tumult ends, patient capital will have benefited.

For the right investor with the right manager, private credit remains one of the more compelling places in the fixed income landscape. Not because it's without risk. But because the returns have historically compensated for those risks in a way that Treasuries and the Bloomberg Agg simply have not and likely will not give the low yields, coupled with rising inflation and rising interest rate risks. The current moment of negativity, driven more by noise than by fundamental deterioration, may prove to be an opportunity.

We wrote a paper titled “UNDERSTANDING PRIVATE CREDIT PAPER.”Click on the link to access the paper.

As always, this is not investment advice. For discussion purposes only.

Views are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. See important CMG disclosures below.

If you like what you are reading, click on the following link.

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: March 26, 2026 Update

Trade Signals Sections:

Market Commentary

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

Why Trend Following Matters

Not a recommendation for you to buy or sell any security. For information purposes only. Outlook and viewpoints are subject to change at a moment's notice. This material is for discussion purposes and does not give you specific advice. Please discuss needs, goals, time horizons, and risk tolerances with your advisor. Important disclosures.Not a recommendation for you to buy or sell any security. For information purposes only. Outlook and viewpoints are subject to change at a moment's notice. This material is for discussion purposes and does not give you specific advice. Please discuss needs, goals, time horizons, and risk tolerances with your advisor.

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Tokens, The Masters and Snowbird

I began today with the intro quote from SEC Chairman Paul Atkins, “All U.S. markets will be on chain within two years.”

It won’t just be publicly traded stocks, ETFs, bonds, and commodities that will trade 24/7 on the blockchain; most everything will be tokenized, including private credit and private equity.

I think this is fantastic news for investors. A fun new world lies ahead.

Speaking of fun, I’ll be watching the practice round on Tuesday, April 7, in Augusta, GA, at The Masters. Long-time readers know I placed a few of my father’s ashes behind the tee box on the famous par-three 12th hole. Dad was an avid golfer with a funky inside-out, looping backswing. He had a mid-teens handicap with the passion and drive of a scratch golfer. He’d golf on Thursdays, Saturdays, and Sundays. Every Monday, he’d call to check in. And every Monday, he’d say, “Steve, I just figured out what I’ve been doing wrong.” I’d smile.

I can’t think of a better place to spend some time with my old man, spiritually, than next to him at Amen Corner.

Snowbird, Utah, with the kids, follows in mid-April. I’ll be hosting a small dinner for a few clients, friends, and readers at the Steak Pit Restaurant located at the Snowbird resort on Wednesday, April 15, at 6:30 pm.

Please email Amy@cmgwealth.com if you are interested in attending.

It’s been 80 degrees and sunny in Utah. Snow coverage is an issue. I saw a press release today that Deer Valley Ski Resort is closing this Sunday. Fortunately, Snowbird and Alta receive approximately twice as much snowfall annually as Deer Valley and Park City. Yet, without a cold front and new snow, it’s going to be slushy. Fingers crossed for some fresh soft new powder snow.

Wishing you and yours the very best!

Warm regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.