On My Radar: Fiscal Dominance and the Not QE Question

December 12, 2025

By Steve Blumenthal

“It’s only QE if they buy duration. Otherwise, it’s just sparkling money-printing.”

— Lyn Alden, @LynAldenContact

What is fiscal dominance? It’s a term you will hear increasingly about, and an important concept. I’ll try to explain it in lay terms today.

Imagine the economy has two big bosses who are supposed to work as a team but often fight:

The Federal Reserve (the central bank) considers itself the responsible adult. Its job is to keep inflation low and the economy stable by controlling interest rates and the money supply.

The government (Congress + President) – the one that spends money on Social Security, Medicare, defense, tax cuts, student-loan forgiveness, new highways, etc., and borrows trillions when it spends more than it collects in taxes.

Normally, the Fed is supposed to be independent. If the government spends too much and borrows too much, the Fed can say:

“Okay, that’s inflationary. I’m going to raise interest rates and maybe even shrink my balance sheet to cool things down.”

That keeps the government somewhat honest, because higher interest rates make all that borrowing painfully expensive. Fiscal dominance is when the tables flip, and the government becomes the real boss. Here’s how it happens in plain English:

The government has run up so much debt (and keeps adding more every year) that interest payments are now huge.

If the Fed tries to raise rates or keep them high to fight inflation, the government’s interest bill explodes → budget chaos → possible default scare → political meltdown.

So the Fed feels forced to keep interest rates lower than it otherwise would, and sometimes even print money (QE, buying Treasuries, etc.) to help the government finance its deficits on the cheap.

In short:

Fiscal dominance = “The government’s giant borrowing needs are now calling the shots, and the Fed has to play along or the whole system blows up.”

Real-World Example Right Now (2025):

U.S. debt is over $38.4 trillion and rising fast.

Annual interest payments exceed $1 trillion (larger than the defense budget).

The government presents no realistic plan to reduce spending or raise sufficient taxes to balance the budget.

So when money markets get tight (like recently), the Fed steps in with measures such as “$40 billion a month in T-bill purchases” — not because the economy is collapsing, but partly to ensure the Treasury can keep borrowing smoothly without interest rates spiking.

That’s fiscal dominance in action: the Fed says “this is just technical plumbing,” but everyone knows part of the reason they’re doing it is that the government can’t afford much higher interest rates.

Bottom Line: Fiscal dominance is when debt and deficits get so big that the central bank loses its ability to say “no” and instead becomes the government’s helper, keeping rates low and liquidity flowing so the borrowing party can continue.

It’s why people like Lyn Alden say “nothing stops this train.” This past week, the Fed sprinkled more liquidity into the system in order to keep the plumbing from breaking—another sign along the road towards a future restructuring. QE occurs when central banks begin buying longer-duration Treasury notes and bonds. I think that day is coming.

So grab your coffee, no sugar needed. The Fed is providing plenty. Today, let’s go deeper, using the Fed’s actions this week as our guide. Also, good friend Barry Habib did a post-Fed meeting update, which he titled “Surprise Shawty.” It’s insightful and fun. Barry graciously allowed me to share the short video with you. You’ll find the link below.

On My Radar: Fiscal Dominance and the Not QE

Not QE?

Barry Habib on Fed Cut - Surprise Shawty!

Trade Signals: December 11, 2025

Personal Note: SoFi Stadium, My Birds, and West Palm Beach

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

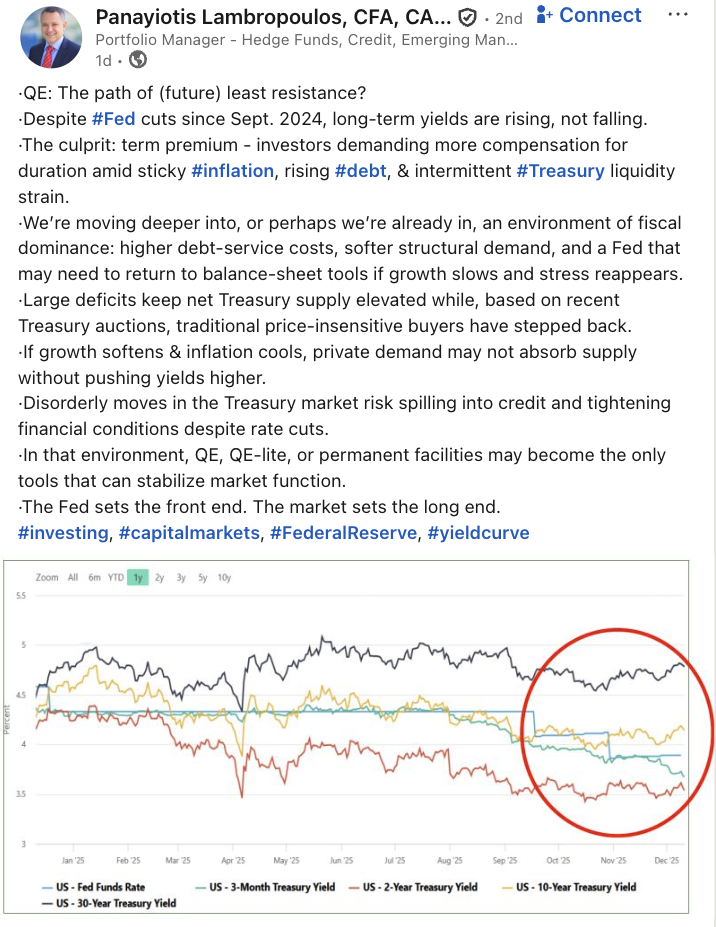

Not QE?

On December 10, 2025, the Federal Open Market Committee (FOMC) voted 9-3 to cut the federal funds rate by 25 basis points, lowering the target range to 3.50%-3.75%. This marked the third consecutive rate cut in 2025, following reductions in September and October, amid a cooling labor market and somewhat elevated inflation (with core PCE projected lower than prior estimates but still above the 2% target). Fed Chair Jerome Powell held a press conference immediately after the announcement, where he described the decision as a "close call" and emphasized a data-dependent approach, signaling potential pauses or further adjustments based on incoming economic data like employment reports and inflation readings.

The surprise: In addition to the rate cut, the FOMC announced it would resume balance sheet expansion through targeted purchases of shorter-term Treasury securities to maintain "ample" reserve levels in the banking system. Specifically, the Federal Reserve will begin buying up to $40 billion per month in Treasury bills (T-bills) starting December 12, 2025 (the Friday following the meeting). Powell signaled that these purchases are expected to remain elevated for a few months—particularly to offset anticipated increases in non-reserve liabilities, which peak around April 2026, before tapering to around $20-25 billion per month, in line with seasonal patterns.

During the press conference, Powell addressed the move directly, stressing its technical, non-stimulatory nature and explicitly distancing it from broader monetary easing, such as quantitative easing (QE).

QE? Let’s take a look and contemplate what this means.Continuing from the intro above: Powell repeatedly clarified that this is not quantitative easing or a signal of aggressive easing. "It is not intended to significantly influence the economy... This is about the plumbing of the financial system, not about moving policy."

I agree, it's monetary expansion, “Not QE.” It is only QE if the Fed targets buying longer-duration assets to stimulate the economy.

The signal is clear. There is stress in the system and plumbing problems in the funding markets. The Fed's move is a symptom of deeper structural issues rather than a deliberate signal of easing.

Too much government debt and spending is the problem. Currently, 20% of government tax revenues go toward paying the interest expense on outstanding debt.

What we need to watch is “Not QE” turning to “QE.” Regardless, the $40 billion in liquidity injections risk becoming inflationary.

Bottom line: the Fed can tinker at the edges, but none of this resolves the debt and spending problem. The path we’re on is one where policy becomes increasingly reactive rather than proactive.

My friend Thaxter sent me the following - same point.

Source: Linkedin

Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. See important CMG and NDR disclosures below.

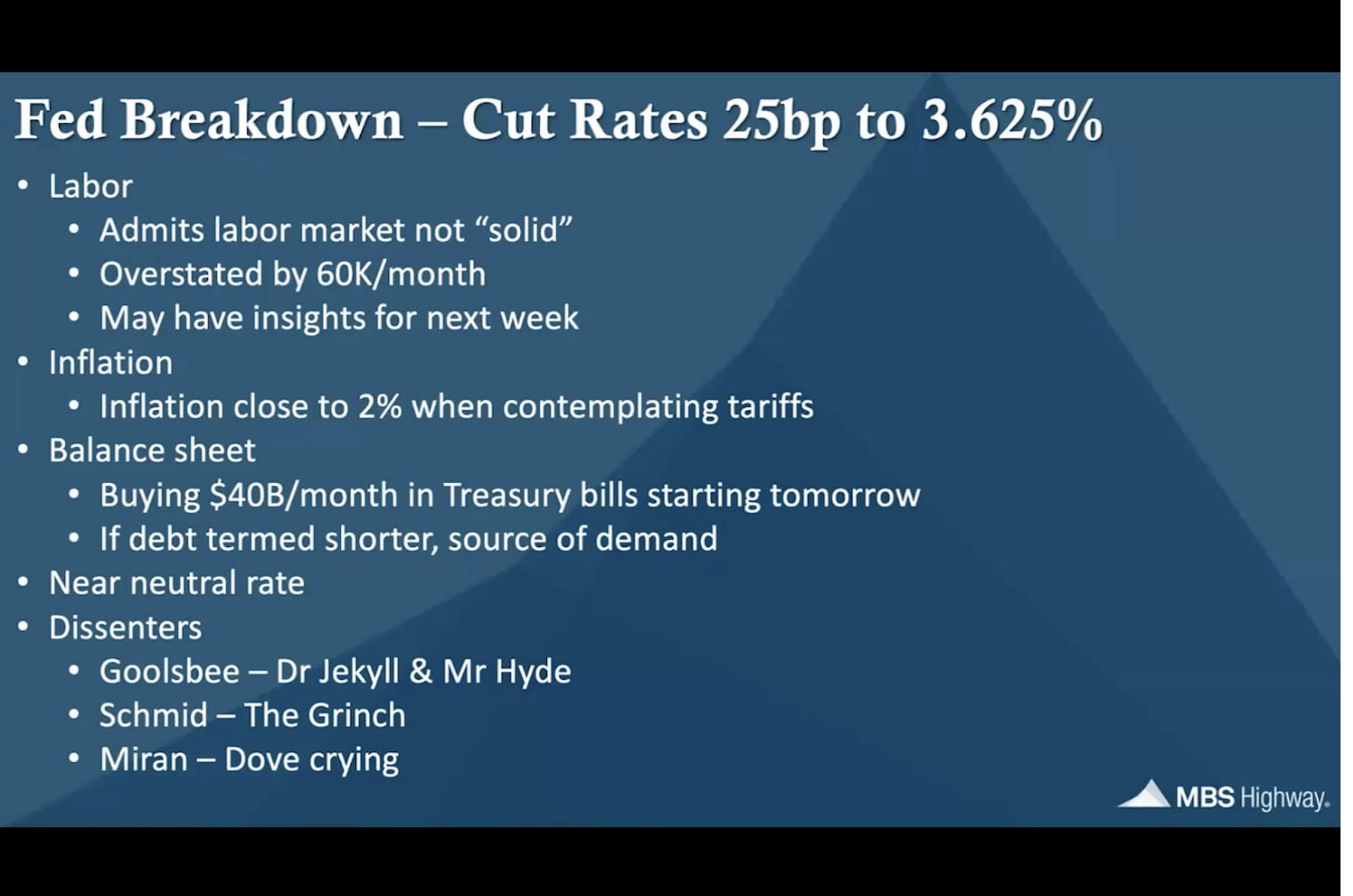

Barry Habib on Fed Rate Cut - Surprise Shawty!

First, a quick summary taken from Barry’s presentation. Click on the picture of Barry to watch his and his team’s excellent update.

Source: MBS Highway

Source: MBS Highway

Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

If you like what you are reading, click on the following link.

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: December 11, 2025 Update

Trade Signals is Organized in the Following Sections:

*Trade Signals basics: The Market Commentary section summarizes notable changes in the core key indicators: Investor sentiment, market breadth, stocks, treasury yields, the dollar, and gold. The Dashboard of Indicators provides a detailed view of all Trade Signals indicators.

Market Commentary - Fed 25 bps Cut and Surprises with QE Start at $40 Billion Per Month

From my friend Peter Boockvar: The Fed repeated that “economic activity has been expanding at a moderate pace.” The Fed has only jobs data from the BLS through September; they said, “The unemployment rate has edged up,” and that “More recent indicators are consistent with these developments.” They repeated that “Inflation has moved up since earlier in the year and remains somewhat elevated.”

I’ll have more commentary on QE and the current state in Friday’s OMR.

The 10-year Treasury Yield declined to 4.10% on Fed day but is now back up to 4.18%. The Weekly MACD is signaling higher interest rates. The Zweig Bond model remained in a -1 bear signal.

Not a recommendation to buy or sell any security. Used for risk management purposes. Consult your advisor.

You’ll find a detailed description of how it works in Trade Signals.

Key Macro Indicators - Investor Sentiment, Market Breadth, The S&P 500 Index (Stocks), The 10-year Treasury Yield (Bonds), and the Dollar

About Trade Signals

Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process.

Yes, it’s that simple.”

– Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: SoFi Stadium, My Birds, and West Palm Beach

Checking in, not so confident as my Philadelphia Eagles have dropped three in a row. That may make others happy, and I get that. That’s what makes sports so much fun. But the overtime loss on Monday night to the LA Chargers was painful to watch.

I was at the game. A big thanks to a big man, Mark C., proudly wearing his Chargers jersey. And what a stadium. The best stadium venue I’ve experienced. Here’s a shot of Mike F, Kyle North, and me.

West Palm Beach is next. We are hosting a dinner for 30 clients and readers on Monday evening. We have room for a few more. If you are interested, please contact Amy at Amy@cmgwealth.com.

Wishing you a wonderful weekend! And best of luck to your favorite team.

Warm regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.