On My Radar: Oh, The Price of Wonder

June 5, 2026

By Steve Blumenthal

“All great technology changes produce bubbles. Nobody can get it exactly right. And when people bet on the technology, they think that buying the stocks is betting on the technology, which is a different thing, because the stocks can be expensive.”

- Ray Dalio

We are one week away from the much-anticipated SpaceX IPO, and it may be one of the most consequential market events in years. Anthropic and OpenAI are expected to follow shortly thereafter. Three of the most transformative private companies in the world are coming to market in rapid succession.

SpaceX is raising $75 billion and targeting a $1.75 trillion valuation, a listing that would immediately place it among the top 10 most valuable U.S.-listed companies, even though only a fraction of its shares will be available for trading.

What makes this moment particularly interesting for investors isn't just the excitement around the names themselves; it's what happens next. Nasdaq moved decisively, announcing a new “fast entry” rule allowing companies ranked in the top 40 by market cap to join the Nasdaq 100 index within just 15 trading days of their IPO, eliminating the previous three-month waiting period. FTSE Russell also did the same. The point is, S&P Dow Jones Indices and other major index providers are quietly rewriting their own rulebooks to accommodate these listings. Traditionally, a company must demonstrate four consecutive quarters of profitability before earning a seat in the S&P 500.

S&P consulted with investors about shortening the listing window for megacap IPOs, waiving minimum float requirements, and removing its profitability requirement entirely. In other words, they were seriously considering bending the rules. Ultimately, S&P held firm, declining to shorten the 12-month seasoning period or waive profitability and float requirements for their most popular index, the S&P 500. But S&P quietly changed the rules for some of its broader indexes, including the S&P Total Market Index and the Dow Jones U.S. Total Stock Market Index, which are designed to capture the full breadth of the market rather than the largest companies.

SpaceX, Anthropic, and OpenAI don't fit that mold, and the index providers know it. Rather than wait, they are signaling expedited, near-immediate inclusion pathways, a remarkable departure from decades of standard practice.

Why does that matter to you? Because every index fund, every ETF, every passive vehicle benchmarked to the popular indices will be forced to buy. The reallocation, across trillions of dollars in passive assets, will be something to watch closely. Forced buying at scale into names already priced for perfection is exactly the kind of setup Ray Dalio is drawing attention to.

The profitability test was a quality screen. The index was meant to represent the country's leading companies, and "leading" has always meant profitable. The seasoning period exists so that a newly public stock's price has time to settle before trillions of dollars of ordinary investors' savings are automatically pegged to it. SpaceX is planning to offer fewer than 5% of its shares publicly, meaning a relatively tiny float will be supporting an enormous implied weight in these indexes. Oh, The Price of Wonder.

Which brings us to this week's letter.

Grab your coffee and find your favorite chair. A lot of content this week. I have a few more thoughts on China worth sharing, we’ll take a quick look at May's month-end valuations, and you’ll find some advice from Ray that ties into today’s intro quote and title. I’m so excited about what AI is already doing for my business and what it means for future productivity and earnings growth, but at what price and when? You’ll find below that Dalio's words echo here. The AI technology is real. The valuation may be a different matter. Watch the float, watch the forced flows, and watch what happens when wealth needs to be converted into money. And don’t miss today’s personal section about the special June sky - we are in for a really cool show.

On My Radar:

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

The Ride From Bangor

I received a lot of reader feedback on last week's letter contrasting Dr. Ram Charan's "China's 90% Model," the three-decade industrial strategy designed to make the world economically dependent on Beijing, to Dr. Pippa Malmgren's latest piece, The Hug and the Circumpunct. Last week's letter stirred up more responses than normal. Please know I appreciate your feedback. I especially appreciate those who challenge my view. Especially this one from Mark in St. Louis.

"Stephen, my friend, to give Pippa the attention and credibility that you do in this newsletter is an act of naivete. The following does not make me an expert, but it probably gives me an edge in understanding China and its government: My wife was born and raised in Shanghai and came to the US in 1983. I have made 13 trips to China, we own a condo in Shanghai, we have plenty of family in and around Shanghai, and I am willing to bet I have read more about China than any of your guests, except a few who have written books.

Pippa reminds me of my 16-year-old grand niece, who is extremely bright, well-traveled, has a tiger mom, and is very creative with a wonderful imagination and an extensive vocabulary. Hence, her ability to craft a story for a creative writing class is off the charts. Pippa is my grand niece, two or three decades later. She knows how to craft an engaging narrative, but she appears to have little comprehension of the deceit and viciousness of Leninism and/or understanding of the CCP's historical roots. Specifically, let's assume Pippa's "signals" all actually occurred, which I think is doubtful. Nevertheless, they are tactical retreats, not strategic transformations, and allowing her to suggest otherwise is a disservice to your readers. Anyone who has followed CCP history since Mao knows these retreats happen regularly. What Pippa is misreading is a relaxation of tension designed to give China more time to build its economic juggernaut. Already, over 30 percent of global manufacturing is done by China, and it is easily on its way to 40 percent in the next few years.

Since you don't know me, I would be surprised if you believed what I have said. Hence, I suggest you do two things: First, ask Niall Ferguson what he thinks of Pippa's assertions. Second, Google "Rhodium Group China" and read the executive summaries for three reports: "Mining, Metals and Megawatts," "Critical Mineral Chokepoints" (May 14) and "China's Next Generation Industrial Policy" (May 11). China is weaponizing international trade while building an economic and commercial juggernaut that is designed to supplant the West's economic dominance. (Rhodium Group is regularly quoted in the Financial Times, Wall Street Journal, and elsewhere.)

I have been reading your weekly epistles for decades. Your summary of Ram Charan's work is superb. In a few words, you have described China's plan to win the war (yes, we are at war) without having to fire a shot. "The Art of War" by Sun Tzu was written a couple of thousand years ago and advises never to go to war unless you know in advance who will win. China is acting on that advice.

Thanks for the many decades of informative letters. I love your charts. I just don't want you to appear naive.

Take care, Mark in St. Louis."

"Tactical retreats, not strategic transformations." "A relaxation of tension designed to give China more time to build its economic juggernaut."

Mark also suggested I look into what Niall Ferguson might think of Pippa's thesis. I did.

Writing in The Free Press on May 13, the day Trump's plane touched down in Beijing, Ferguson said, "Trump Wants Détente. Xi Wants Taiwan." And Ferguson reminded us of a Ronald Reagan warning worth remembering. "Détente, Reagan famously said, is what a farmer has with his turkey until Thanksgiving. Source: The Free Press

Pippa’s view is that Trump is turning the Rubik's Cube, seeking a peaceful co-existence. One big turn to get his colors to align is Taiwan.

Flying home from Beijing on Air Force One:

"On Taiwan, Xi feels very strongly. I made no commitment either way."

"I think the last thing we need right now is a war that's 9,500 miles away."

The $14 billion arms sale to Taiwan, announced in January 2026, was delayed before the summit and remains on hold. Trump stated his decision on it "depends on China." Source: Global Taiwan Institute

Xi left Beijing having conceded little on the structural issues, rare earths, chips, trade surplus, the 90% Model, while gaining ambiguity around Taiwan's defense, from the sitting U.S. president.

The Ride from Bangor

Which brings me back to a car ride I have thought about many times since.

In 2019, I attended Camp Kotok in Maine. On the drive from the Bangor airport, I sat next to Dr. Jonathan Ward, author of China's Vision of Victory. Ward did his doctoral work at Oxford, using Communist Party archives that have since been closed to the world. He had spent years living in China, traveling across Tibet, crossing the South China Sea by cargo ship. He spoke Chinese. He had read the plans.

Ward's central argument: by the time China's ambitions were widely understood, Beijing's success had already begun to feel inevitable. The CCP had exploited America's desire to "sleep through difficulties." Xi merely "took the mask off" in recent years, but the strategy had been stated openly for decades. Source: Axios

The objective: dominance in global affairs on a longer time frame. The restoration of China's position as the world's supreme power by the year 2049, the centennial of the founding of the People's Republic. Axios

That was 2019. Dr. Charan's 2026 SIC presentation documented how much ground China has covered since. The 90% Model was not improvised. It was stated. It was executed.

So, Where Does That Leave Us?

I want to be fair to Pippa. Last week, I said I thought both maps, Charan's and Malmgren's, could be simultaneously true. The world can contain genuine diplomatic shifts and an unrelenting industrial strategy. Those things are not mutually exclusive. Which map proves true depends on the time frame.

But Mark's phrase stays with me. Tactical retreats, not strategic transformations.

Reagan's farmer-and-turkey line was not just a quip. It was a warning about the difference between what a negotiation looks like and what it actually achieves.

Xi came away from the Beijing summit with stability, legitimacy, and strategic ambiguity on Taiwan's defense. The 90% Model keeps running. The critical mineral chokepoints remain.

Sun Tzu wrote that you should never go to war unless you know in advance who will win. China is acting on that advice, not at the negotiating table but on the factory floor, in the rare-earth refinery, and in the energy infrastructure buildout designed to power the next frontier of technology.

The summit was a photo. The industrial strategy is the movie.

The Bullets That Could Bring China Down Without a Shot Fired

A question worth asking this morning, coffee in hand, is whether there are economic consequences to China’s plan? Every yin has a yang. Sun Tzu cuts both ways.

Beneath the disciplined march of the 90% Model, there are structural cracks that don't show up in the trade surplus data. They are the economic consequences of the strategy itself. Internal economic contradictions that compound quietly, year after year, until they don't.

Here are the potential bullets. Shots never fired. Self-inflicted.

Bullet One: Ghost Cities and the Wealth Trap

Property constituted roughly 70% of Chinese family assets, and for two decades, Beijing encouraged ordinary citizens to pour their savings into apartments in cities being built faster than people could fill them. Evergrande alone defaulted on over $300 billion in debt, leaving hundreds of thousands of buyers paying mortgages on homes that don't exist, a generational wealth destruction that has collapsed consumer confidence and suppressed the domestic spending China desperately needs to rebalance its economy. Source: Irreview Ryan J. Hite

Bullet Two: The Debt Machine Is Running Out of Road

In 2000, China needed roughly 13–16 yuan of new debt to generate 1 yuan of GDP growth. By 2025, it will need 60–75 yuan to produce that same result. Source: The Unz Review

That is not a growth model; it is a treadmill accelerating toward a wall, and Rhodium Group's assessment is unambiguous: decay of China's policy tools will almost certainly continue, as no reforms are underway to repair them. Source: The Unz Review

Bullet Three: The Currency Weapon That Cuts Both Ways

China's weak currency keeps export prices low, but it is being driven not by deliberate devaluation so much as by something more dangerous: producer prices in China fell for 34 consecutive months through mid-2025, with consumer inflation hovering near zero. China is exporting its deflation to the world while trapped domestically in a deflationary feedback loop, with suppressed spending, a weakening currency, greater export dependence, and more factory subsidies, all of which are extraordinarily difficult to escape without structural reforms, which Beijing has shown no willingness to pursue. Source: fxstreet

Bullet Four: Demographics - Getting Old Before Getting Rich

China's population peaked in 2021 and is now declining. By 2050, the UN projects 40% of the population will be over 60, with only 10% under 15. The working-age population is projected to fall from roughly 900 million today to 250 million by the end of the century.

Getting old before getting rich. This means fewer workers funding the 90% Model, fewer taxpayers supporting a rapidly expanding retiree class, and a pension system already under strain. The comparisons to Japan's lost decades are instructive. Source: WorldpopulationclockApollo Academy

Bullet Five: The Consumer That Never Arrived

The 90% Model was always supposed to be a bridge to a domestic consumption economy. That transition has not happened.

Consumption accounts for only about 32% of China's GDP, which is far below that of developed economies.

And I think it is unlikely that citizens who lost wealth in the property collapse, with thin social safety nets, and watch state-connected elites capture the gains, are not about to unleash a spending revolution on command. Source: Planning Times

Conclusion

None of this means China fails. Beijing has enormous foreign reserves, deep internal control, and a demonstrated willingness to absorb pain in the name of long-term strategy.

But the 90% Model is being funded by a deteriorating balance sheet, fueled by a deflating currency, run by a population aging faster than the strategy can mature, and sold to a citizenry whose wealth has been quietly hollowed out.

Sun Tzu also wrote: "He who knows when he can fight and when he cannot will be victorious."

The United States does not need to fire a shot to complicate China's 2049 ambition. Time, debt, demographics, and deflation are already in play on the field.

The question is the degree to which Washington understands this and the political will and skill to navigate the challenges ahead. This is what Dr. Ward has been saying all along… Wake up, free world! To which, I think our lights are turning on.

Some other resources:

Rhodium Group, "China's Financial and Fiscal Decay," March 2026 — link

IMF, 2025 Article IV Consultation — China, February 2026 — link

Apollo Academy, "China's Working-Age Population Shrinking from 900 Million to 250 Million" — link

Here is a link to Pippa's full post — The Hug Manifests.

Here is the link to my summary notes on Dr. Ram Charan's 2026 SIC conference presentation.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

* No guarantees; all investing involves risk. Views are subject to change. TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

As always, this is not investment advice. For discussion purposes only. Reach out to us if you have any questions.

Views are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. See important CMG disclosures below.

If you like what you are reading, click on the link and share it with a friend (it’s free).

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not intended to recommend buying or selling any security and is for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

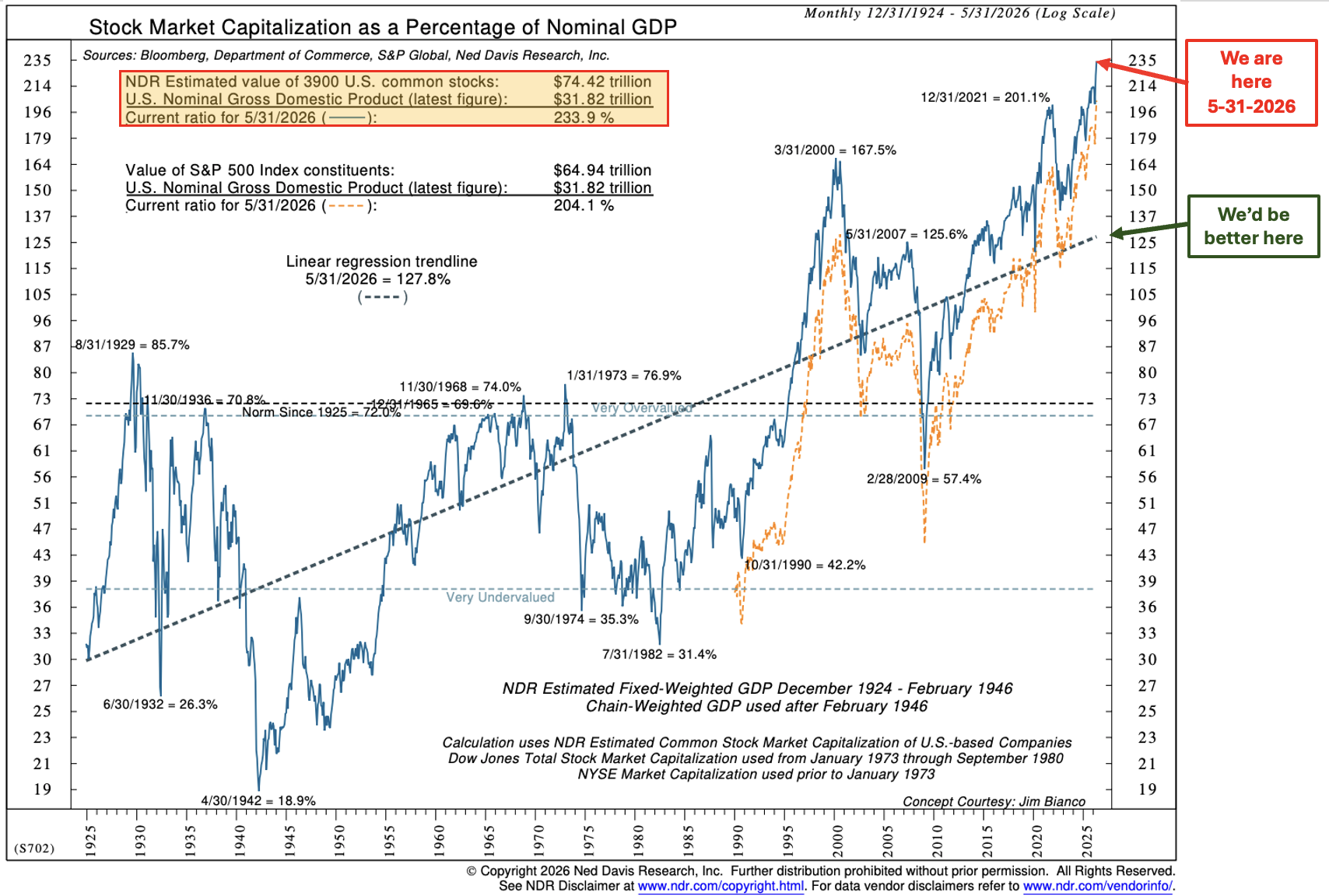

Valuations, Buffett, and Value

The Buffett Indicator

Record high, and note the distances between the red “We are here” and the green “We’d be better here” upward sloping regression line.

The S&P 500 Index is massively overvalued.

Source: NDR w CMG notations

look at saved X charts on investor over optimism

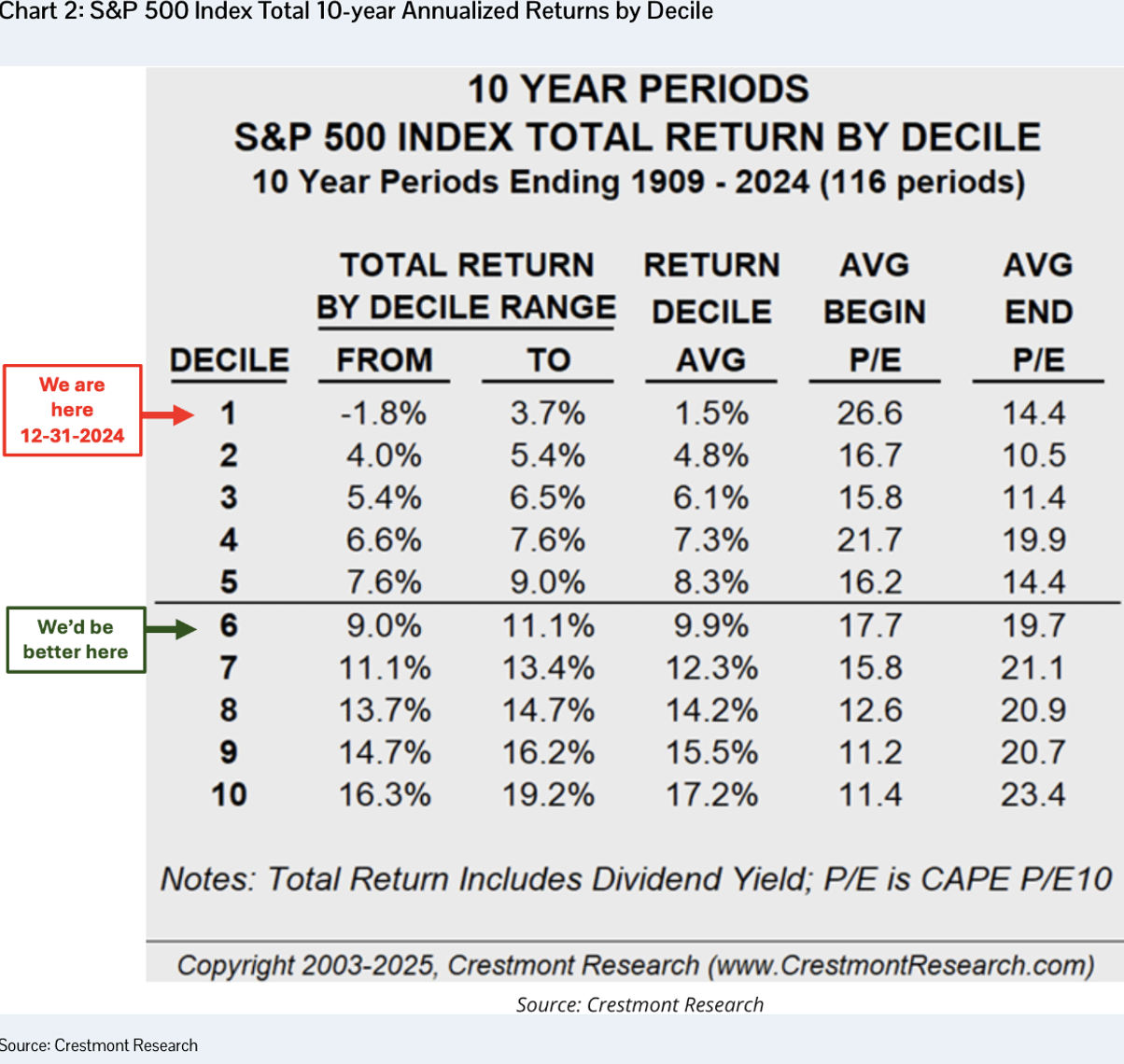

Subsequent 10-year Annualized Returns by Decile

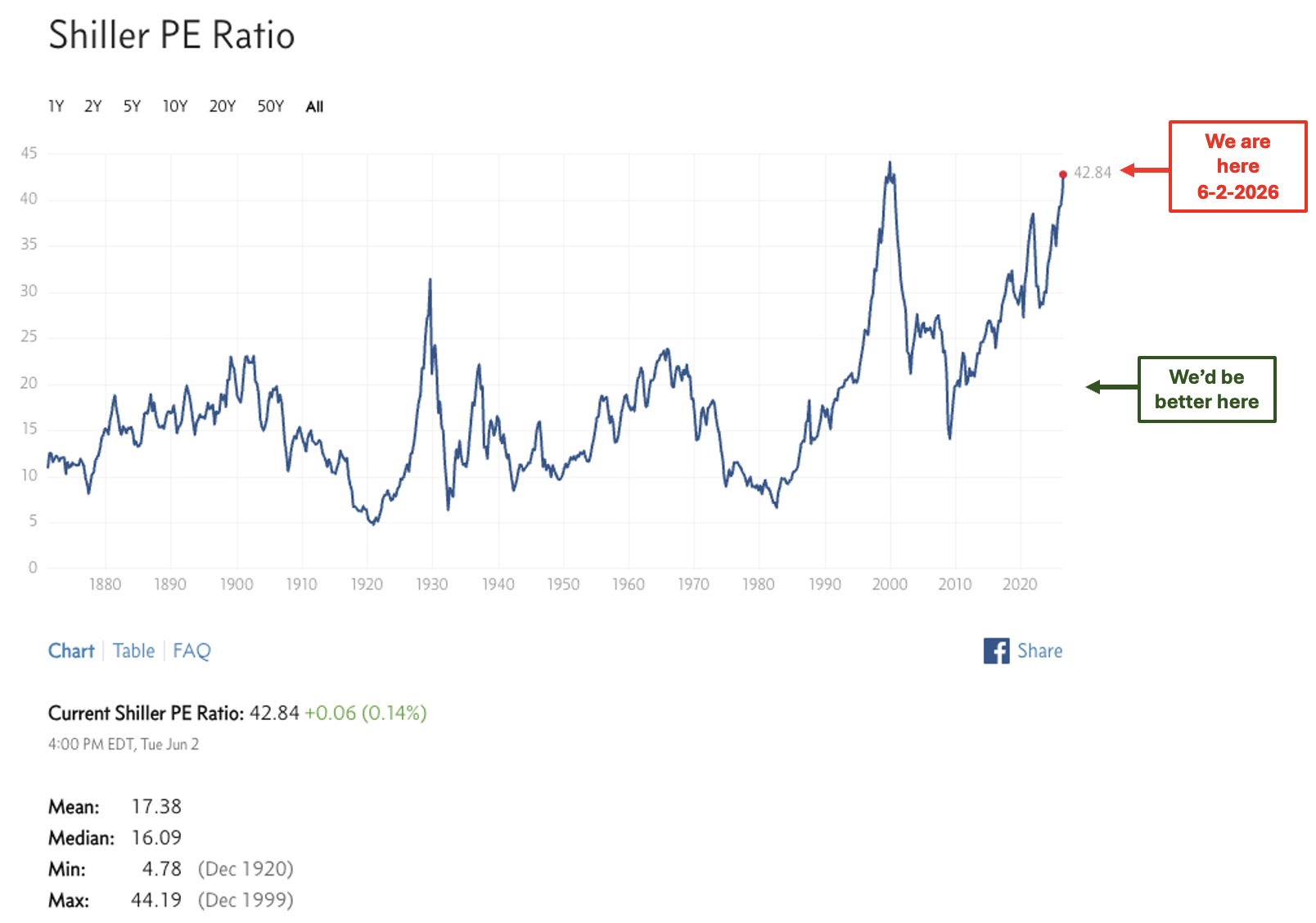

We are in the top 10% zone of the highest Shiller Price to Earnings ratio readings dating back to 1909

Note in Decile 1, the average beginning PE was 26.6. Look at the chart above again. The current reading is 42.84, which is higher than all periods, including the secular peaks in 1929 and 1966, with one exception, the tech bubble peak in 2000. To which it is nearing.

Bottom line: If you own the S&P 500 cap-weighted index, probabilities suggest returns in the -2% to +2% range over the next 10 years. And a likely very bumpy ride.

Source: Crestmont Research w CMG notation

Lastly, this period reminds me so much of 1998 and 1999. And there is no person of greater influence on investing than Warren Buffett.

In July 1999, Buffett spoke at the Allen & Co. conference in Sun Valley, Idaho, a room packed with venture capitalists, dot-com founders, and tech billionaires. His message was uncomfortable:

From 1964 to 1981, U.S. GDP grew 400%, Fortune 500 revenues grew fivefold — yet the Dow went from 874 to 875. A flat line. Great economy, terrible market, because valuations started too high.

Of 2,000 U.S. auto companies at the industry's dawn, three survived. Even transformational industries can be terrible investments when bought at mania prices.

He warned the crowd that overvaluation destroys returns regardless of how revolutionary the underlying technology is.

Nobody wanted to hear it. The Nasdaq was up 102% that year.

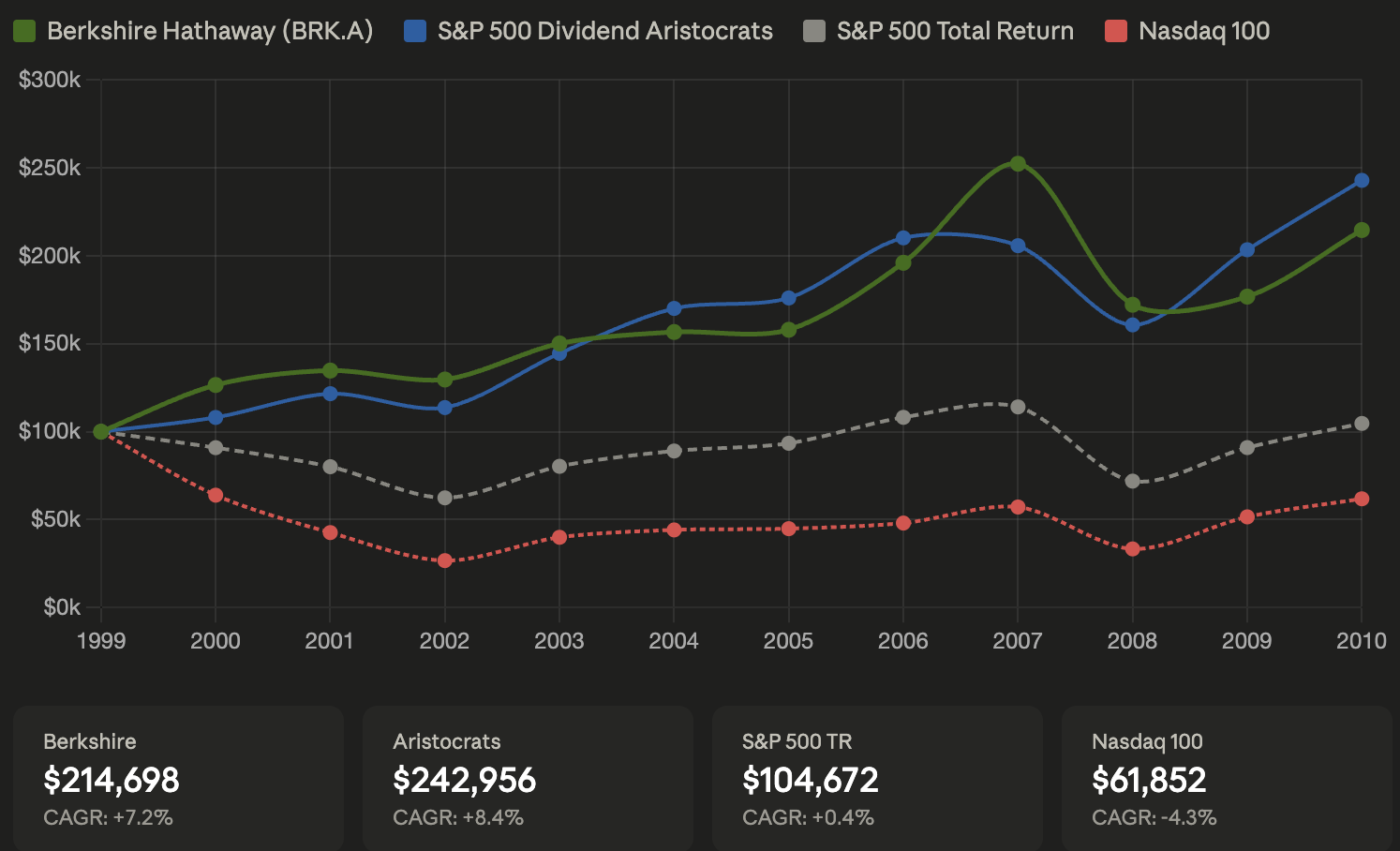

In the following chart, two things jump out. First, Berkshire and the Aristocrats tracked each other closely over the full period, with both representing a similar investment discipline: quality businesses, reasonable valuations, durable earnings.

Second, the S&P 500's "lost decade" wasn't just a bad run, it was the mathematical consequence of starting the decade at 29x earnings.

The setup today: Aristocrats at ~23.5x, S&P 500 at ~32.7x. Those being mocked for owning boring dividend compounders in 1999 had the last laugh by 2010. Worth keeping in mind.

That's the brutal math of starting overvalued. A $100,000 investment in the Nasdaq 100 on December 31, 1999, the moment everyone was piling in and mocking Warren Buffett, was worth roughly $47,000 eleven years later. You lost more than half your money over a decade while owning the most celebrated index in the world.

Meanwhile, Berkshire, down 20% in 1999 and featured on Barron's cover asking "What's Wrong, Warren?," more than doubled. High free cash flow quality businesses paying high dividends, those old-economy compounders, nearly doubled right alongside Buffett.

Feels like we are in a similar place today. Here’s a look at 1999 to 2010. Blue and green were good, white and red were bad.

Starting value: $100,000 invested 12/31/1999. BRK.A price return only (no dividend paid). Dividend Aristocrats pre-2005 data is backtested by S&P Dow Jones Indices. S&P 500 Total Return includes dividends reinvested. Nasdaq 100 returns based on QQQ/index price return. Sources: 1stock1.com (BRK.A); TradeT hatSwing.com (Nasdaq 100); S&P Dow Jones Indices; Multpl.com. Past performance is not a guarantee of future results.

NOT A RECOMMENDATION FOR YOU TO BUY OR SELL ANY SECURITY. FOR INFORMATION PURPOSES ONLY. Here are the sourced data points used in the chart:

Berkshire Hathaway (BRK.A) Annual Price Returns Source: 1stock1.com — "BRKA: Berkshire Hathaway, Inc. Class A Yearly Stock Returns." Source Nasdaq 100 Annual Returns Source: TradeThatsSwing.com — "Historical Average Returns for Nasdaq 100 Index (QQQ)" URL: Source S&P 500 Total Return Annual Returns Source: Multpl.com — "S&P 500 PE Ratio by Year" (returns derived from standard S&P 500 TR historical data) URL: Source S&P 500 Dividend Aristocrats Annual Returns Source: S&P Dow Jones Indices LLC — "S&P 500 Dividend Aristocrats: The Importance of Stable Dividend Income" (March 2025 research paper) URL: Source: SPGlobal

Important caveat to note in your letter: Dividend Aristocrats data prior to May 2, 2005, is backtested by S&P Dow Jones Indices; the index was not formally launched until that date. S&P Global flags this in their research paper as hypothetical historical performance.

We’ll review my list of valuation charts when we get the mid-year data post June 30.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Why I Recommend Being a Global Macro Long-Short Investor

I found Ray Dalio’s post this week on global macro long-short investing to be a nice summary of an investing approach worth including in portfolios as a piece of the allocation puzzle. In working with clients, my consistent message is that there is always opportunity to make money. Frankly, I write OMR each week to help me make sense of the shifting tides and better understand which waves might be best to ride. I hope you find value too. From Ray,

“I’m at a stage of my life in which I want to pass along principles I’ve learned that have helped me to people who want them, especially principles about investing, because I have a demonstrated subject matter expertise in that area, which is important. This brief note is about how to approach investing.”

“Most investors find themselves investing in certain markets and in certain ways because they accidentally stumbled into them rather than because they chose the type of investing they want to be doing. If one were to choose the best type of investor to be without any prior strong biases to be a certain type, I would recommend being a global macro investor because:

All markets are affected in big ways by global macro forces. The most important decision you have to make is what asset allocation you have—how much in stocks, bonds, commodities, real estate, gold, etc. and where to have these things. That’s a macro decision. The big moves in the value of your portfolio come from the relative shifts in the values of asset classes which are driven by macro forces. With an understanding of global macro, you can know how to structure a balanced portfolio which will allow you to make tactical movements between asset classes much better than without it. All other types of investing are focused on just one asset class in a specialized area that goes through big cyclical waves of good and bad times that for long-only investors take their portfolio values up and down in ways that are beyond their controls. In contrast, by being a global macro long-short investor who can invest in different liquid markets (stocks, bonds, gold, and other markets) in all countries from either the long side or the short side allows you to move into to what is good from the long side or bad from short side, which allows you to bet on practically anything and make money in any type of environment. So, by being a global macro long-short investor, there is no excuse for not making money other than one’s own bad decision-making.

If you don’t understand the big (i.e., macro) changes that are going on in the world (i.e., globally) you can’t adequately understand the full range of risks and opportunities that you need to understand to be successful over the long run. To close yourself to understanding the opportunities and risks that come from abroad and are reflected in their markets (which you can invest in) lowers your opportunities and increases your risks.

Global macro investing—i.e., understanding what is going on in the world and testing your ability to navigate it by betting in the markets—is a very fun, enthralling, and rewarding game. Global macro investing is very interesting because it leads you to focus on all the big things that are happening around the world, it’s very fun to be able to convert your theories about the world into bets that constantly get scored to provide you with the feedback that helps your understandings of the world get better, and it’s very rewarding because it pays very well if you can play this game well. It also gives you a great macroeconomic understanding of the forces driving politics, geopolitics, and culture, without which I don’t believe you can really understand what’s happening in the world.

Unlike illiquid private markets, liquid public markets give you a) more flexibility to rebalance and to change your positions as circumstances and your views change, and b) more and better information than private markets, which keep you stuck in your position with less information that is less reliable.

(Footnote: There are some reasons that lead some people to prefer private markets vs. public ones, although the history of average private equity returns has been about the same as public equity returns. Sometimes there are private deals that are uniquely attractively priced that one can “get in on,” sometimes there are tax advantages, and sometimes investment managers get involved with the deal to improve the business and its returns.)

Those are the reasons that I think that striving to be a great global macro long-short investor is the most rewarding type of investor to strive to be. That’s true even if you later evolve into being another type of investor, because after being a global macro long-short investor for a while, you will carry with you an invaluable understanding of global macro forces that will help you in your more specialized job.

While that’s how I see it because I love global macro long-short investing so much and have done it for so long (about 60 years), I might be biased in favor of it, so you should ask others about these points of mine and their points of view, and then decide.

By the way, I want to help you be a great global macro long-short investor. I will be regularly passing along principles and thoughts so you can look over my shoulder while I am playing the game and describing the principles that are motivating my moves. But if you want to really get into my approach, I recommend the Dalio Market Principles Online program I built with the Wealth Management Institute of Singapore, which has received a 100% recommendation rate from past participants. You can learn more here.” Source: Dalio on Substack

His current thinking on AI, wealth, and bubbles (click photo). He is asked if he thinks AI is a bubble that will pop.

His answer is yes.

Click on this short Bloomberg interview:

Source: Bloomberg courtesy Wolf Financial, X

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: June 4, 2026 Update

Market Commentary

Here’s the weekly recap through Thursday:

Subscribers - link below.

The Dashboard of Indicators follows next.

Trade Signals - subscribers only

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: June Sky

Susan (my wife) and I have a habit of stepping outside after dinner, red wine in hand, just to look up. Most nights it's quiet, a few stars, maybe the moon. But June is spectacularly different this year, and I didn't want you to miss it.

Mark these five dates:

June 9 — Venus and Jupiter pass so close they'll nearly touch. Look west after sunset - no telescope needed.

June 15 — Super new moon means zero moonlight. It's also peak Milky Way season. The sky will be dark, and you may see the full band of our galaxy for the first time in your life.

June 18 — Five objects line up in the western sky at sunset: Mercury, Jupiter, Venus, a crescent moon, and the star Regulus. All visible to the naked eye.

June 21 — Summer solstice. The longest day of the year. A good reminder that the planet is still doing its thing, indifferent to markets and headlines.

June 29 — The full Strawberry Moon rises inside the teapot of Sagittarius. A beautiful close to the month.

Put the phone down on these nights and grab a fine red wine. The sky is putting on a show.

And when you look up, really look up, it will be hard not to feel it. The enormity of it all. The billions of stars, the galaxies beyond galaxies, the sheer scale of what's out there compared to the noise down here.

Source; Click photo

Whatever is happening in the world right now, and there is plenty, so much of it feels very large until you consider the view from above.

So here's a small prayer I'll offer this month, under whatever sky finds you:

May we find peace. May we choose to work together, tolerate our differences, and even celebrate and learn from them. And may we create, for ourselves and for each other, something worthy of the brief and remarkable time we have.

The universe is vast and mostly silent. We are small, and we are here together. That still means something.

Enjoy nature’s show... and the World Cup. June is going to be great.

Kind regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

{kind=link}

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.