On My Radar: Charan vs. Malmgren — Two Maps, One World

May 29, 2026

By Steve Blumenthal

“The statesman’s duty is to bridge the gap between his nation’s experience and his vision.”

— Henry Kissinger

There is a particular kind of intellectual tension that makes you stop in the middle of a sentence and stare out the window. I had that experience this week.

I spent part of the week revisiting Dr. Ram Charan's 2026 Strategic Investment Conference presentation, his forensic breakdown of China's 90% Model, the three-decade industrial strategy designed to make the world economically dependent on Beijing. I spent much of this morning rereading Dr. Pippa Malmgren's latest piece, The Hug and the Circumpunct, in which she argues that something genuinely historic happened at the Temple of Heaven when Trump and Xi met. Not a photo opportunity. A civilizational pivot.

Ram - Pippa. Two brilliant, credible people. Two completely different maps of the same terrain.

Two weeks ago, I shared my notes from Dr. Ram Charan’s presentation at the Mauldin Economics 2026 Strategic Investment Conference on China with you. Dr. Ram Charan is a world-renowned business advisor, author, and speaker who has spent the past 40 years working with many top companies, CEOs, and boards of our time. Fortune magazine has called him "the most influential consultant alive."

In 2019, Dr. Jonathan Ward opened my eyes to China’s Vision of Victory, his popular must-read book. Dr. Charan's presentation highlighted the gains China has made since then. Both were, and may well continue to be, right.

Dr. Pippa Malmgren’s (bio) post-Trump/Xi take is entirely different.

My job this week is to hold both maps at once and try to figure out which roads are actually open.

Grab your coffee and find your favorite chair. We’ll examine and consider their diverse views. Also, Jim Bianco’s SIC presentation was exceptional. You’ll find my bullet point notes along with a few charts in the Bianco section below. Importantly, I want to say thank you for the time you spend with me each week. It’s appreciated!

On My Radar:

Personal Note: The Beautiful Game

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

China vs. U.S. - Dr. Charan vs. Dr. Malmgren

Two Smart People. Two Very Different Views on China.

Last week, I shared Dr. Ram Charan's analysis of China's 90% Model. A 30-year, methodically executed strategy to build overwhelming capacity in strategic industries, convert trade surpluses into geopolitical leverage, and diminish American economic power without firing a shot.

I wouldn't call Charan's view alarmist. It is simply factual, documented, and, in his words, not hidden. He sees the Beijing summit as a tactical pause in a long economic war. Xi sent Trump home with Boeing orders and warm optics while the structural issues, rare earths, chips, and the 90% model remained firmly in China's favor.

This week, Dr. Pippa Malmgren sees the same summit through an entirely different lens. Where Charan sees a transactional cease-fire, Pippa sees a geopolitical turning point.

Her argument: both sides looked into the abyss (4 million kilotons of nuclear capability between the U.S., China, and Russia alone) and made the only rational choice available. War/mass destruction or shared co-existence and abundance.

The visit to the Temple of Heaven was not a photo opportunity. It was, in her reading, a deliberate ritual act signaling that geopolitics is no longer a zero-sum game.

She calls it a shift from scarcity thinking to abundance thinking, from "Make War-La" to "Make Money-La." She points to tangible signals most of the press missed entirely: the first Chinese tanker through the Strait of Hormuz, Xi's explicit statement that the IRGC is a problem that needs to be shut down, joint agreement that Iran cannot have a nuclear weapon, and the quiet repositioning of Japan as Taiwan's regional protector.

So who is right? My honest opinion is both. Charan describes the structural reality that has been building for three decades. Malmgren describes a potential inflection point in how the two superpowers choose to manage that reality going forward.

The 90% Model does not disappear because of a summit. But if Pippa is correct that something deeper shifted at the Temple of Heaven - that both leaders genuinely subordinated short-term rivalry to the imperative of avoiding catastrophic conflict while riding a wave of technological abundance - then the investment implications are profound and largely unpriced in the markets.

Charan’s Argument: The Leopard Does Not Change Its Spots

Dr. Ram Charan's framework rests on something Pippa's optimism cannot easily dismiss, a 30-year track record of execution. The 90% Model was not improvised. Charan says it was deliberately formulated under President Hu after Tiananmen, openly stated in Mandarin, and executed with remarkable consistency across multiple leadership transitions.

Solar panels. EVs. Rare earths. Semiconductors. Shipbuilding. The pattern repeats: hyperscale production, loss-leader market share, purposeful currency devaluation (making Chinese goods even more competitively priced), and, eventually, the displacement of every foreign competitor.

The 90% objective is to drive your competition out of business and create economic dependency. Charan says, “This is not ideology. It is an industrial strategy backed by a $7.4 trillion reserve war chest and a $1.25 trillion annual trade surplus projected to reach $1.8 trillion this year.”

The Beijing summit, viewed through Charan's lens, fits the pattern perfectly. Xi is a master of patience. He received Trump with military honors, rose seeds, and a walk through sacred gardens.

Yet not much was actually achieved.

Xi committed to 200 Boeing jets - a gesture almost identical to the 300 planes promised during Trump's 2017 Beijing visit, before relations soured.

Rare earth exports remain 50% below pre-restriction levels, with no resolution in sight.

Not a single Nvidia H200 has shipped to approved Chinese buyers, and critically, Beijing is actively discouraging its own companies from purchasing them, preferring Huawei's domestic chips instead.

That is the 90% Model at work in real time: China is willing to forgo access to the world's best chips today to own the capability tomorrow. The structural leverage did not move one inch. Xi sent Trump home feeling like he won. That is precisely what a 50-year strategy looks like when it is working.

Malgrem’s Argument: This Time Really Is Different

Pippa's argument is not naive optimism. It is grounded in a specific and uncomfortable logic: the weapons now in play make traditional great-power competition not just costly but existential. One Satan II missile carries the explosive equivalent of the entire Allied bombing campaign of World War II, and can be delivered in under 30 minutes. The Poseidon torpedo is designed to flood entire coastlines with radioactive seawater for generations. In this environment, the old Kissinger calculus of managed rivalry breaks down entirely. There is no 'winning' in a kinetic exchange between peer nuclear powers. She says that both sides know this with a clarity that no previous generation of leaders has possessed.

But Pippa goes further than just the nuclear arithmetic. She describes something closer to a Rubik's Cube — a world in which every geopolitical problem is connected, and none can be solved in isolation. To get China's cooperation on Iran and North Korea, Taiwan must be quietly renegotiated. To secure that deal, Venezuela and Cuba must agree to expel Russian and Chinese intelligence and military operators. To make that credible, the U.S. must stop fomenting regime change through color revolutions. Which means Trump must tame what Pippa calls America's own 'shadow,' the Deep State.

Pull one piece, and every other piece moves.

In her framing, she asks: “Are the U.S. and China swapping Cuba and Venezuela for Taiwan?” Sort of, she says, with conditions. Both sides are behaving in ways that signal 'this is mine, and that is yours.”

That sounds abstract. But the actions on the ground appear strikingly concrete.

Venezuela and Cuba

In January, U.S. special forces extracted Nicolás Maduro from Caracas. The Trump administration's explicit demand, stated publicly within days, was that Venezuela sever all ties with China, Russia, Iran, and Cuba before resuming oil production.

The strategic objective, according to analysts at the Center for Strategic and International Studies, was not primarily the oil itself but the removal of China and Russia from their forward operating base in the Western Hemisphere, described as fully aligned with the administration's national security strategy. The Cuba play mirrors it: secure commercial access, extract nickel and cobalt for critical mineral supply chains, and push Beijing and Moscow off the island entirely.

North Korea

Pippa predicted that the U.S. and China would quietly bless a joint effort to contain and absorb the North Korean problem. Replacing the old proxy-conflict framework with a multi-year strategy in which Xi and Trump ultimately share the glory of lifting the 1953 Armistice. Pippa indicated that the validation of this came fast.

China's Foreign Minister Wang Yi visited Pyongyang just before the Trump-Xi Summit. Following the Beijing meetings, the White House confirmed that Trump and Xi shared a goal of denuclearizing North Korea, language Beijing had completely scrubbed from its official diplomatic readouts since 2022. Xi is now expected to visit Pyongyang imminently, his first trip since 2019, following directly on the heels of summits with both Trump and Putin. As one Brookings analyst put it this week: Beijing has become 'the center of gravity for global diplomacy in the first half of 2026.'

Taiwan

The quietest piece of the puzzle. On the very day the Trump-Xi Summit opened, official cross-strait directives authorized Shanghai residents to apply for tours to Kinmen and Matsu, the same frontline islands that triggered two near-wars in 1954 and 1958. Regional scholars and Beijing policy analysts are noting that Beijing is deliberately using these travel restarts to convert former military tripwires into showcases of cross-strait commercial alignment.

Not reunification by force. Integration by commerce. The 'Make Money-La' dynamic Pippa described, playing out in real time.

Here is the point I find most striking. Charan framing: watch what they do, not what they say, actually validates Pippa's thesis rather than undermining it. Venezuela, Cuba, North Korea, Taiwan: these are not press releases. They are actions.

The Rubik's Cube is moving. The honest question is whether it is moving in a single coordinated direction or whether each piece is moving for its own unconnected reason. That is precisely the uncertainty investors must sit with.

The Most Probable Outcome

The honest conclusion is that both frameworks may be correct. They are simply operating on different time horizons.

Charan is right about the structural reality. The 90% Model is real, durable, and nowhere near dismantled. One summit does not reverse three decades of industrial strategy. Rare earths, chip self-sufficiency, shipbuilding dominance, and the trade surplus machine will continue to grind. Any investor or policymaker who reads the Temple of Heaven symbolism as the end of that competition is making a category error.

But Malmgren is likely right that something genuinely shifted in intent. The nuclear arithmetic is simply too stark for either side to ignore indefinitely, and the abundance thesis - cheap energy via SMRs, AI-driven productivity, the conversion from scarcity to surplus- gives both sides a credible off-ramp that did not exist a decade ago. The economic incentives for cooperation now rival, and may soon exceed, the political incentives for rivalry. I like her optimism.

My view is the probable outcome looks something like a managed, durable détente. Not entirely dissimilar to Nixon-Brezhnev in the early 1970s, in which two superpowers compete fiercely on industrial and technological grounds while simultaneously constructing guardrails against catastrophic escalation.

In the outcome:

Trade expands in non-sensitive sectors. Cultural and brand exchange increases.

Iran and North Korea are jointly managed toward a resolution.

The U.S. quietly walks back its commitment to defend Taiwan, allowing for slow, peaceful integration, in exchange for agreed-upon multipolar restructuring and Chinese cooperation on Iran.

Ukraine is settled on terms that leave no one fully satisfied and everyone functional.

The structural competition over chips, rare earths, and the 90% Model does not end. It simply moves into a more formalized arena with agreed rules of engagement - much as the Cold War eventually did.

In summary, a more clearly agreed-upon multipolar world.

What This Means for Investors

If this view proves correct, and there is no guarantee it will, it suggests that the tail risk of a catastrophic superpower conflict, which markets have persistently underpriced, is diminishing.

It does not mean China is no longer a strategic competitor. It means the competition is being channeled. The distinction matters enormously for positioning across equities, commodities, defense, energy, and emerging markets.

A few things worth watching:

Energy

If the U.S. genuinely becomes China's energy partner, Alaska LNG, protected Hormuz passage, the geopolitical risk premium in oil shifts structurally. That matters for positioning.

Defense

A managed détente does not mean lower defense spending. It means defense spending shifts from Taiwan contingency planning toward technology competition: AI, space, cyber, hypersonics.

Emerging Markets and Commodities

A multipolar world with agreed-upon spheres of influence has historically been a tailwind for commodity-rich emerging markets, which are no longer forced to choose sides.

Critical Minerals

Venezuela and Cuba's nickel and cobalt, and the broader push to accelerate the buildout of Western Hemisphere supply chains. This is a multi-year investment theme.

My Bottom Line

Dr. Ram Charan gave us the map of the terrain. Dr. Pippa Malmgren may be telling us that the rules of the game just changed. Both deserve to be read carefully and held simultaneously.

I'll be watching to see if both China and the U.S. do what they say they will do.

Watch the actions, not the words. So far, and this surprises me a little, the actions are lining up with Pippa's map.

I'm pulling for her.

Here is a link to Pippa's full post — The Hug Manifests.

Here is the link to my summary notes on Dr. Ram Charan's 2026 SIC conference presentation.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

* No guarantees; all investing involves risk. Views are subject to change. TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

As always, this is not investment advice. For discussion purposes only. Reach out to us if you have any questions.

Views are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. See important CMG disclosures below.

If you like what you are reading, click on the link and share it with a friend (it’s free).

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not intended to recommend buying or selling any security and is for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

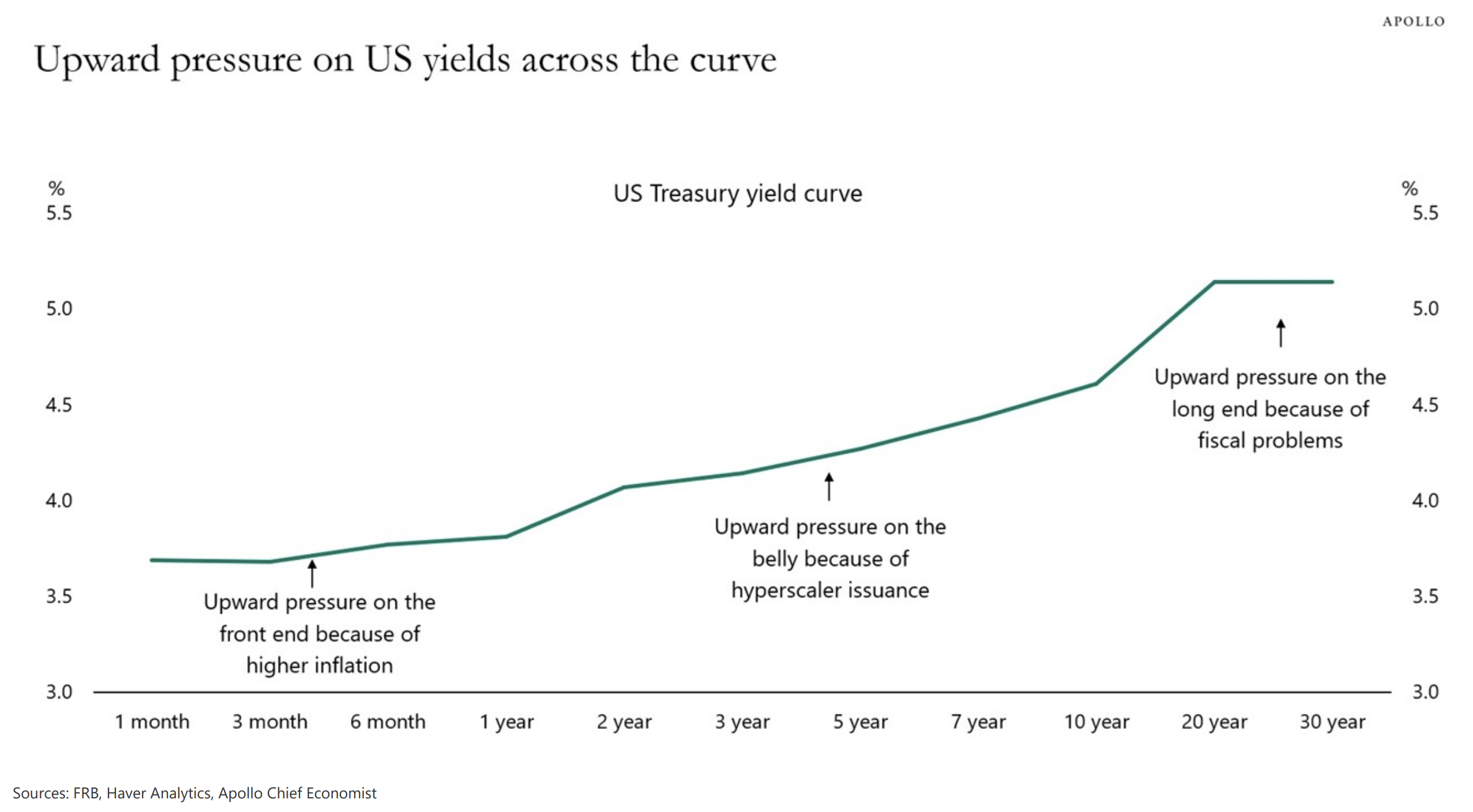

Three Persistent Trends Pushing Rates Higher

From Torsten Slok at Apollo: “Three Forces Pushing Rates Higher Across the Curve

Front-end rates are under upward pressure because inflation is higher for longer.

The belly of the curve is seeing upward pressure on yields because of hyperscaler issuance.

And long-end rates are moving higher because of more Treasury supply and less Fed demand.

The bottom line: Investors should position for a persistently higher rate environment.Source: Apollo

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

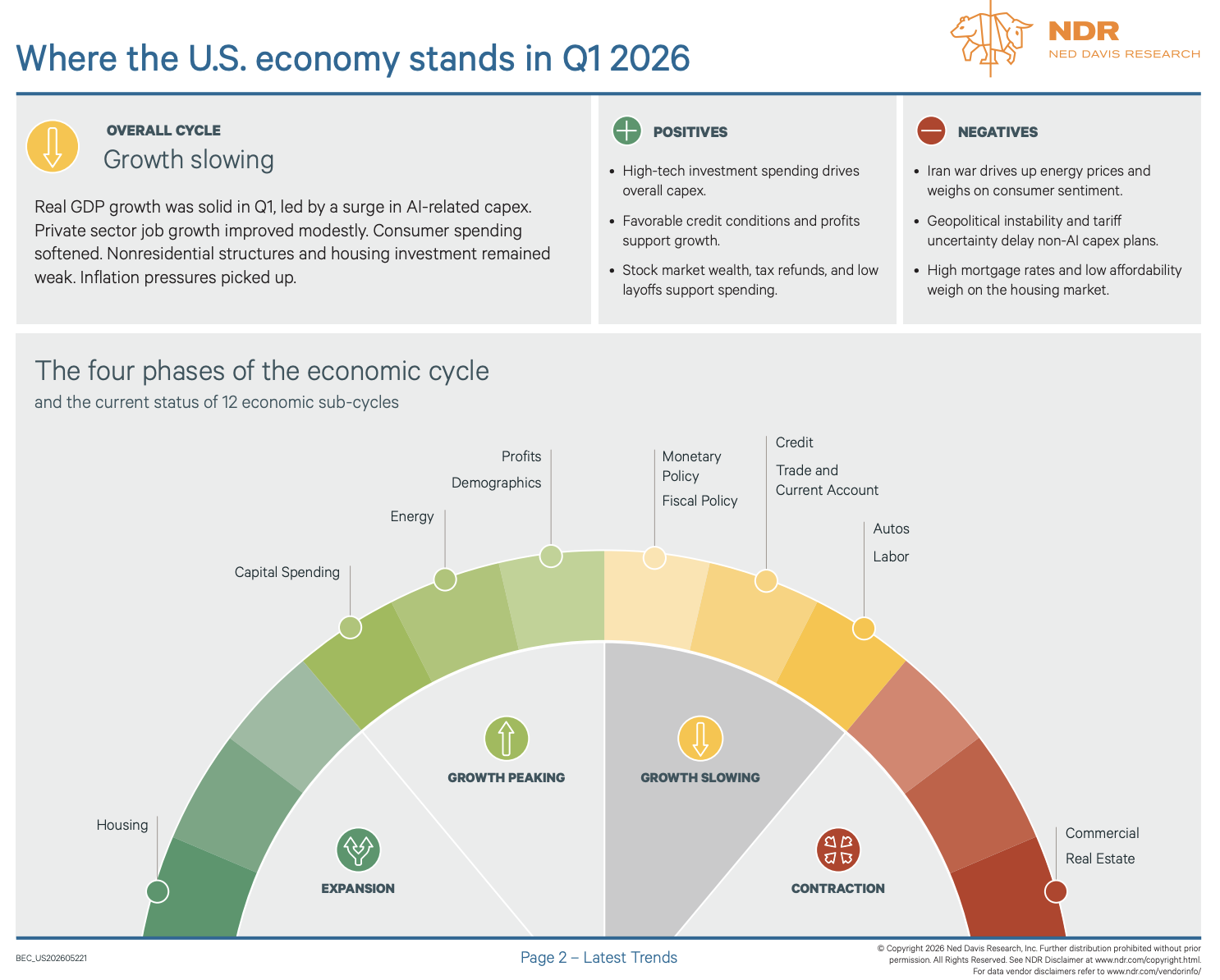

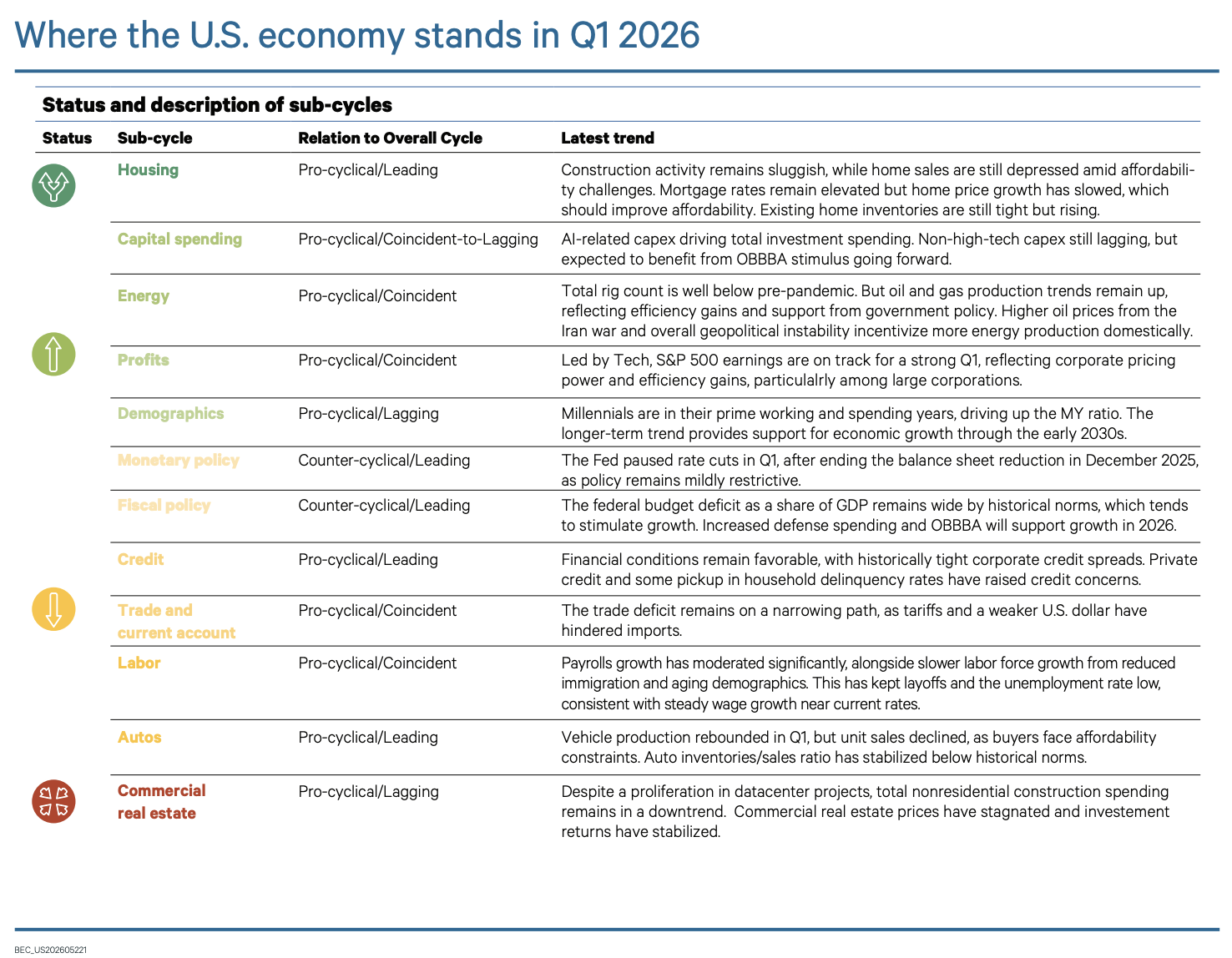

U.S. Economy Q1 Review

Highlights from our friends at Ned Davis Research:

Real GDP growth was solid in Q1. AI-related capex spending leads the way. However, consumer spending softened, and the housing market remained weak. Inflation pressures picked up.

The majority of sub-cycles still reflect slowing economic growth

U.S. consumer sentiment falls to a fresh record low, as inflation expectations rise, a downside risk to near-term consumer spending

U.S. Leading economic index up slightly, still pointing to a fragile growth outlook ahead, but no recession.

Source: NDR

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Jim Bianco - SIC2026

“If the Fed doesn't give a damn about inflation, I don't give a damn about their bond market.”

— Jim Bianco, Bianco Research

What follows is a dense, data-rich summary of Bianco’s 50-minute presentation - Jim is one of the best in the business. First the conclusion, then the content:

Inflation is structural,

Oil is the accelerant,

The bond market is the judge, and

The new Fed chairman has a very difficult road ahead.

My bullet point summary of Jim Bianco's key points:

Jim Bianco – SIC2026

Jim Bianco of Bianco Research presented at the Mauldin Economics Strategic Investment Conference. Jim is one of the sharpest minds I know on bonds, inflation, and macro. Here's what stood out.

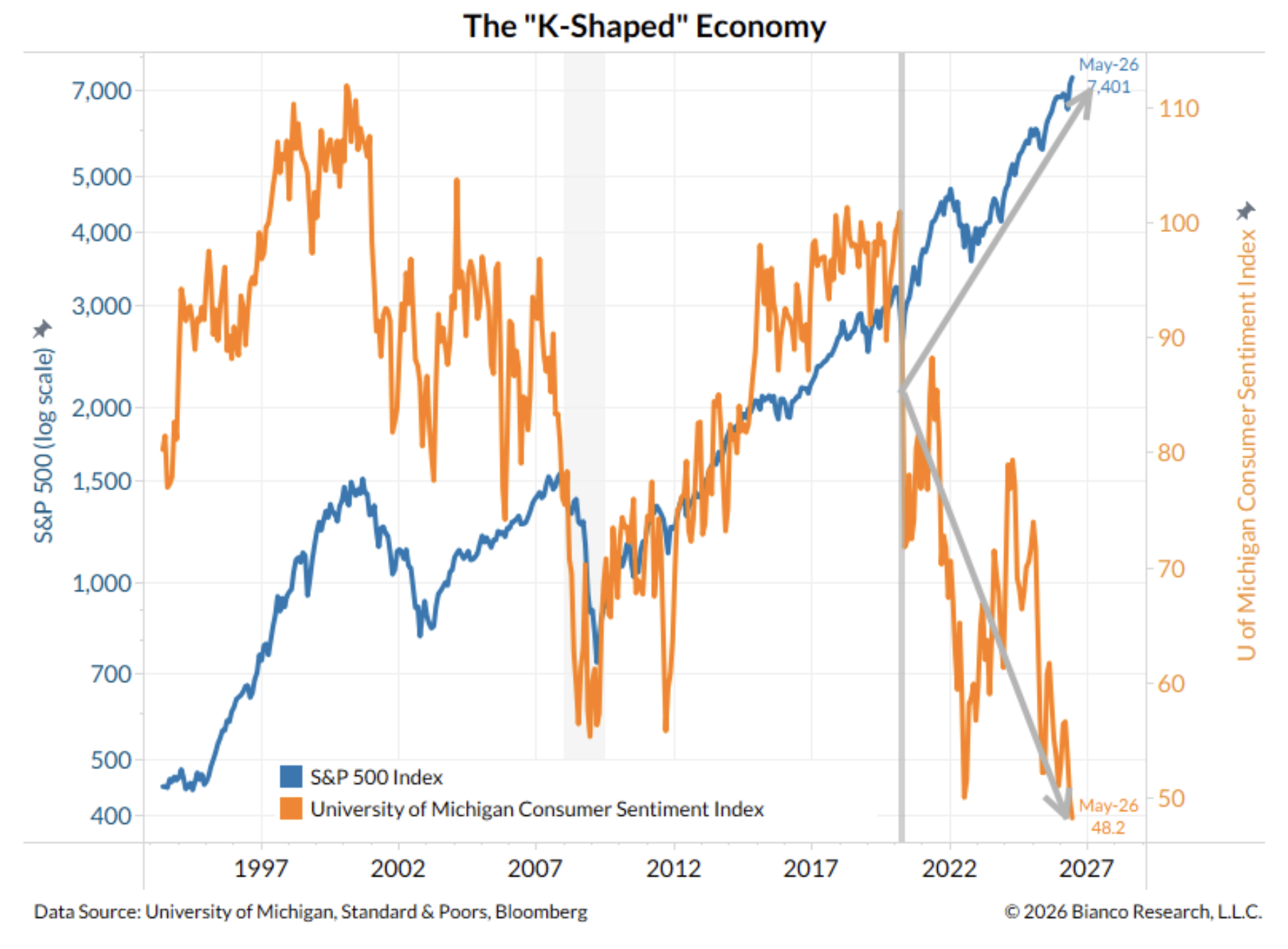

The K-Shaped Economy

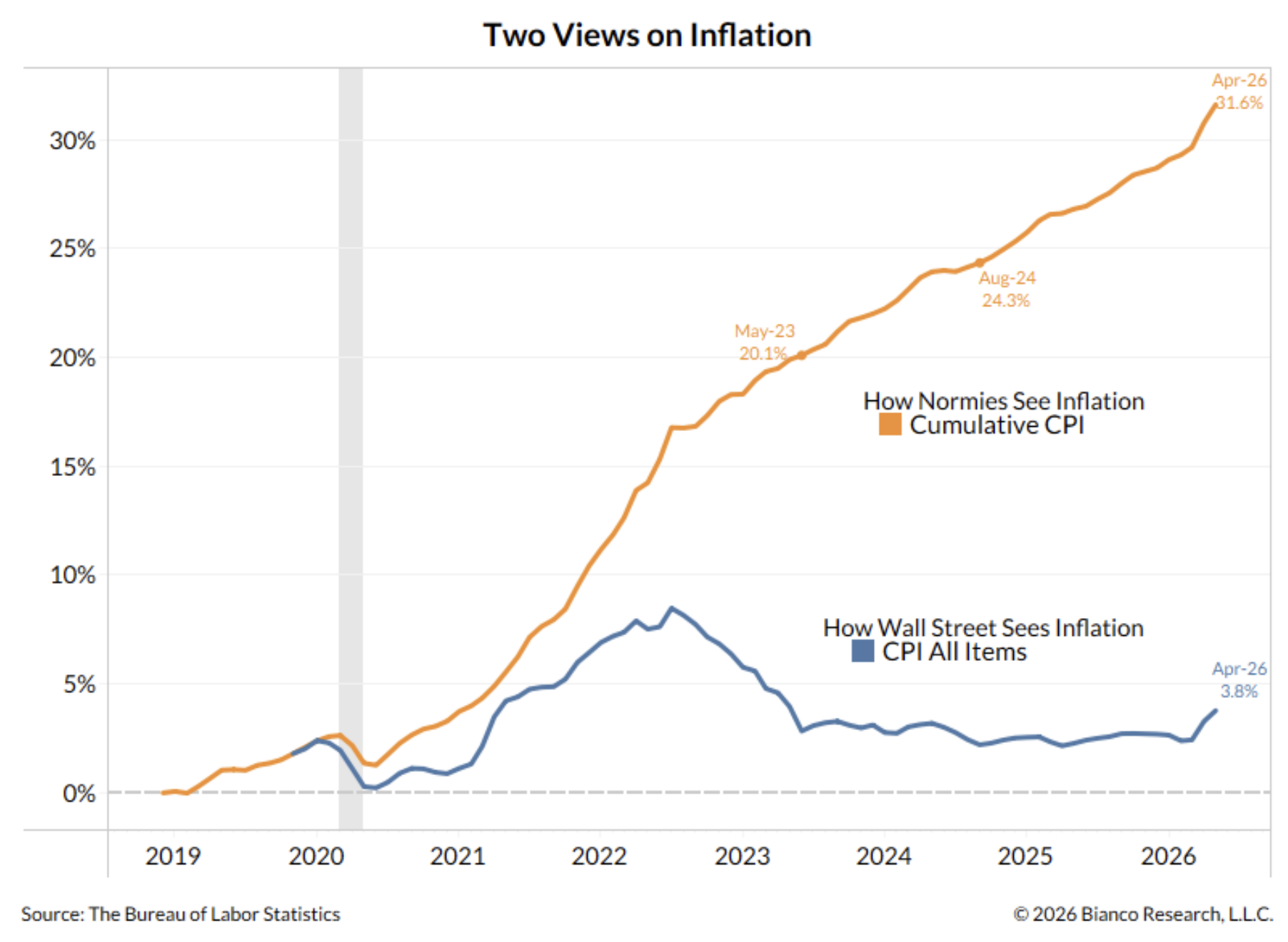

Consumer sentiment hit 48.2 in May, an all-time low going back to 1952. Lower than COVID. Lower than the financial crisis. Lower than 9/11. The stock market is near all-time highs. These two things have never been more disconnected.

The reason: cumulative inflation. Since April 2020, prices are up ~30%. Wages are up ~25%. The average American paycheck has not kept pace with the average rise in prices for six straight years. That gap is the story.

Real wages just went negative again. CPI at 3.8%, wages growing at 3.6%. The last time that happened was three years ago. Every time real wages go negative, consumer sentiment collapses. We're starting from a 74-year low and now adding this.

About half the country doesn't have $1,000 sitting in a checking account. Roughly 40% rent. They can't "pay it and move on." They have to make hard choices. That's the bottom of the K.

Source: SIC2026, Jim Bianco

Inflation Is Structural, Not Transitory

The post-COVID inflation average is 4%. That would have been one of the highest readings of the prior cycle. We are in a different regime.

The old argument, "AI and technology will bring inflation down," has been wrong for six years. De-globalization, remote work, geopolitical instability, and shifting consumer preferences have collectively raised the inflation floor.

AI helps. Without it, we'd be in an even higher inflation world. But it is not going to get us back to the 1.69% average of the post-financial-crisis era. Not without a serious recession first.

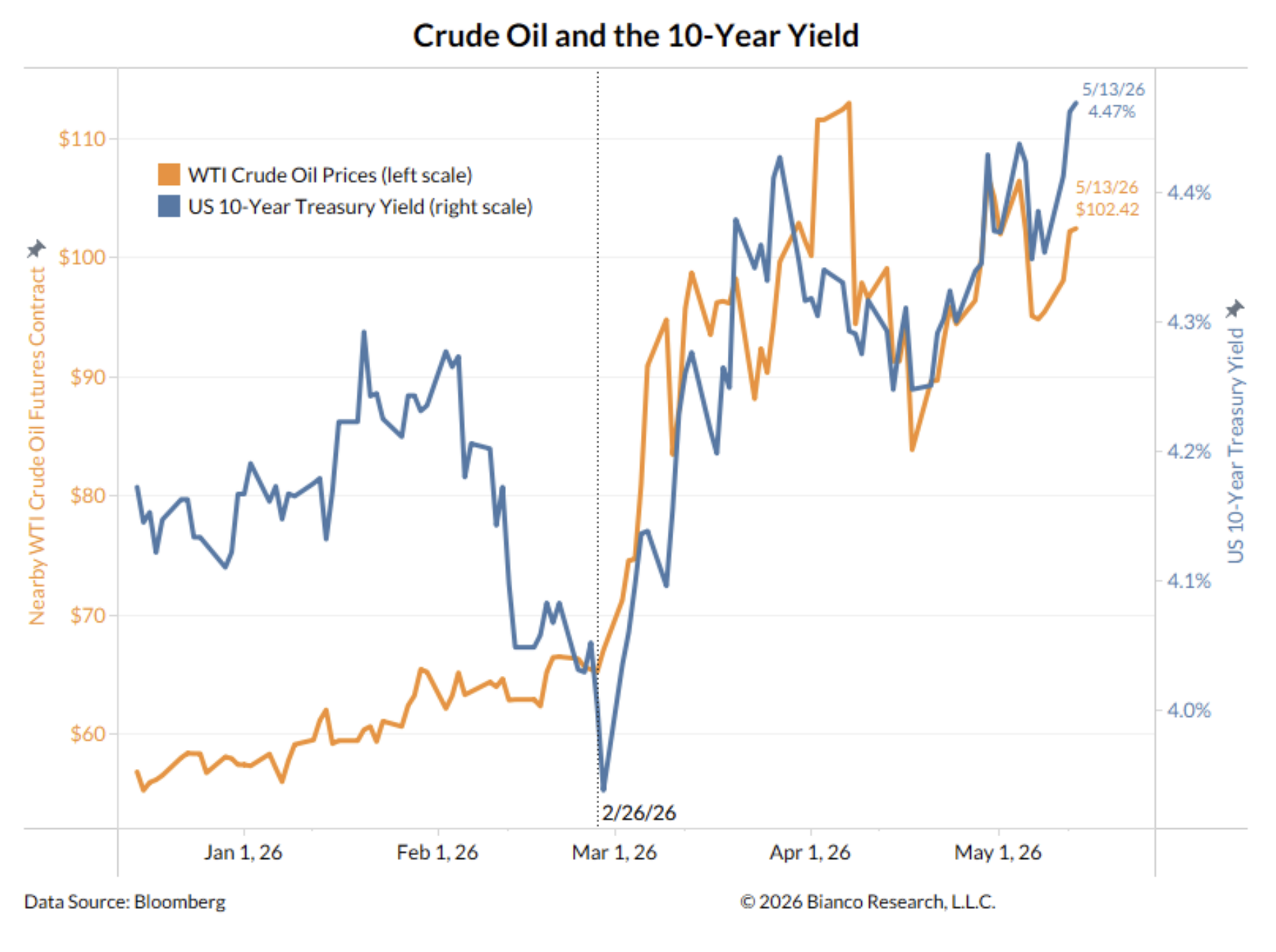

Oil Is the Match That Lights the Fuse

National average gas prices rose 53% in 68 days from the start of the war, from just under $3.00 to $4.55.

Here's the number most people miss: deferred oil futures contracts matter more than spot prices. The December 2026 Brent contract was within 20 cents of its all-time high. The June 2027 contract hit a new all-time high during the presentation. The market is pricing oil above $90 by year-end and above $80 a year from now. The market is not pricing in a quick resolution.

According to JPMorgan Commodity Research, global oil inventories have been drawn down by roughly 1 billion barrels since the disruption in the Strait of Hormuz began, roughly equal to the supply that's been cut off. That's why spot prices aren't at $200.

We've been burning the buffer. JP Morgan estimates we hit "stress level" inventories in June and hit the floor by September. After that, shortages start showing up in earnest.

The 10-year Treasury yield and the price of crude oil have been moving in lockstep since the war started. Bond traders are now energy traders, and vice versa. If you don't own energy, and you still own bonds, and energy is repricing them.

Source: Mauldin Economics, Bianco Research

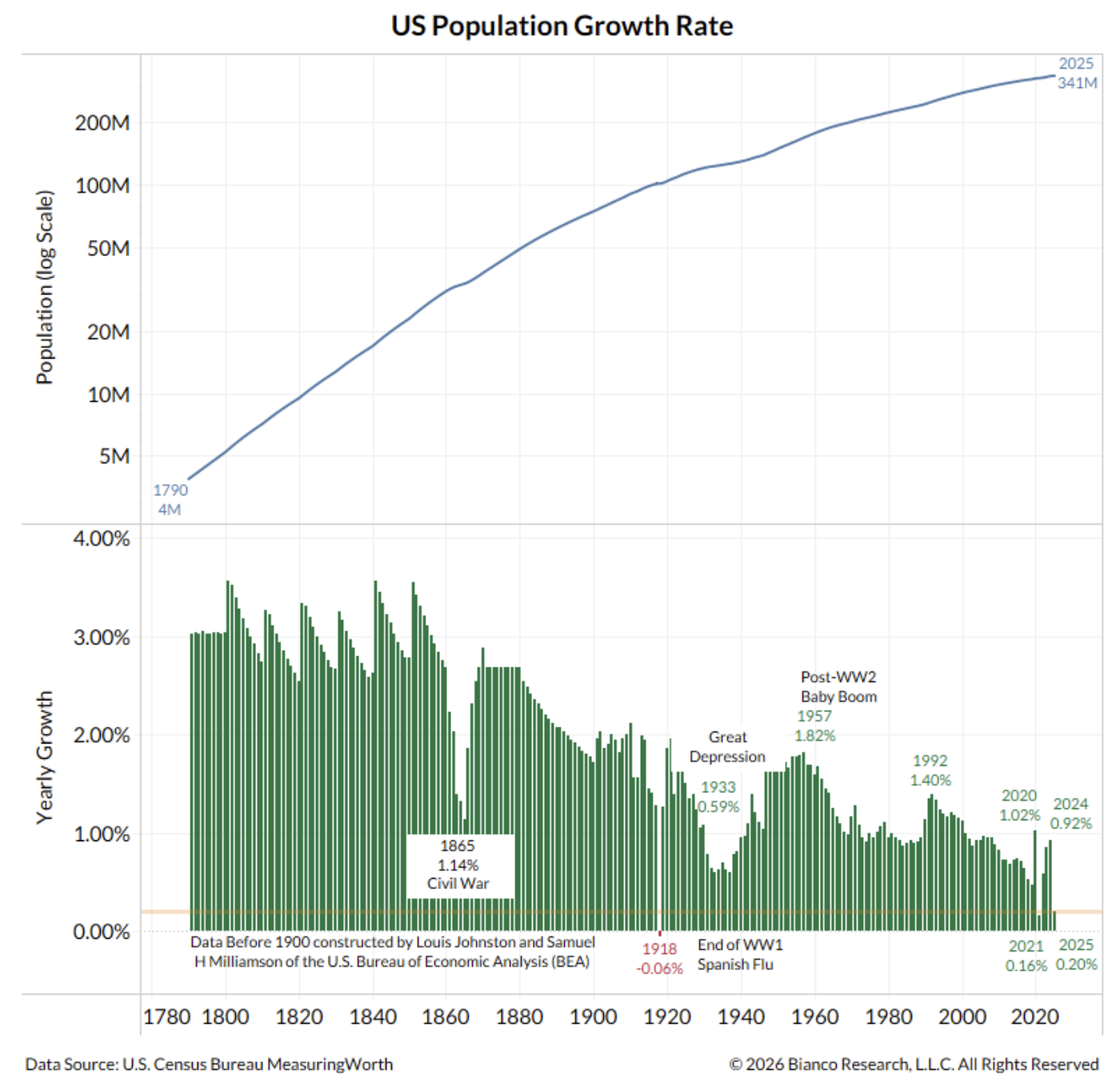

The Labor Market

Monthly job creation has collapsed from an average of 151,000/month in mid-2024 to roughly 20,000 now. January's print was negative 92,000. Yet unemployment hasn't risen. GDP is holding around 2.5–3%.

The reason: the labor breakeven rate, the number of jobs the U.S. economy needs to create, is essentially zero. The U.S. fertility rate is 1.62, an all-time low over the past 200 years, well below the 2.1 replacement rate. The working-age population (ages 15–64) is growing at a rate of 0.

Immigration was the historical offset. It's no longer that. Net immigration has gone negative since Trump took office. The U.S. population growth rate in 2025 was 0.2% — the third-lowest in American history.

There is a reasonable chance that 2026 will see an outright population contraction, which would be only the second time in history (after the 1918 Spanish flu).

Bottom line: we don't need jobs because we're not creating people. Any positive payroll number is fine.

Zero is the new normal, and the Fed knows it.

Interest Rates: Higher for Longer Is Not a Catchphrase, It's Math

Nominal growth = real growth + inflation.

Inflation is up. Real growth is not falling. Therefore, nominal growth is rising. And interest rates should follow nominal growth higher. Jim says, " That's not an opinion, that's arithmetic.”

The 10-year yield went from 3.94% the day before the war started to 4.50% at the time of his presentation. Up 54 basis points, the highest in nearly a year.

On March 1st (the day the war started), markets were pricing in 2.5 rate cuts for 2026. Today, markets are pricing in a 40% chance of a rate hike before year-end. Cuts are gone. Hikes are now in the equation.

Kevin Warsh’s Challenge

Kevin Warsh was confirmed as Fed Chair on the day of this presentation. Jim says, "He got the job, telling Trump that AI would drive productivity, bring down inflation, and that rates could be cut aggressively.” He added,

The market disagrees. With 3.8% inflation and rising nominal growth, cutting rates now could send the 10-year to 5.5% — fast. Bond investors will walk if the Fed ignores inflation.

Speaking to every bond investor’s mindset, Jim's quote that stuck with me: "If the Fed doesn't give a damn about inflation, I don't give a damn about their bond market." That's about as direct as it gets.

An additional wrinkle: the FOMC voted 8-4 at its last meeting just to hold steady. Warsh may need 6 other members to vote with him to cut. There's a real argument that those votes aren't there. We could see, for the first time since 1939, a Fed chair on the losing side of a policy vote.

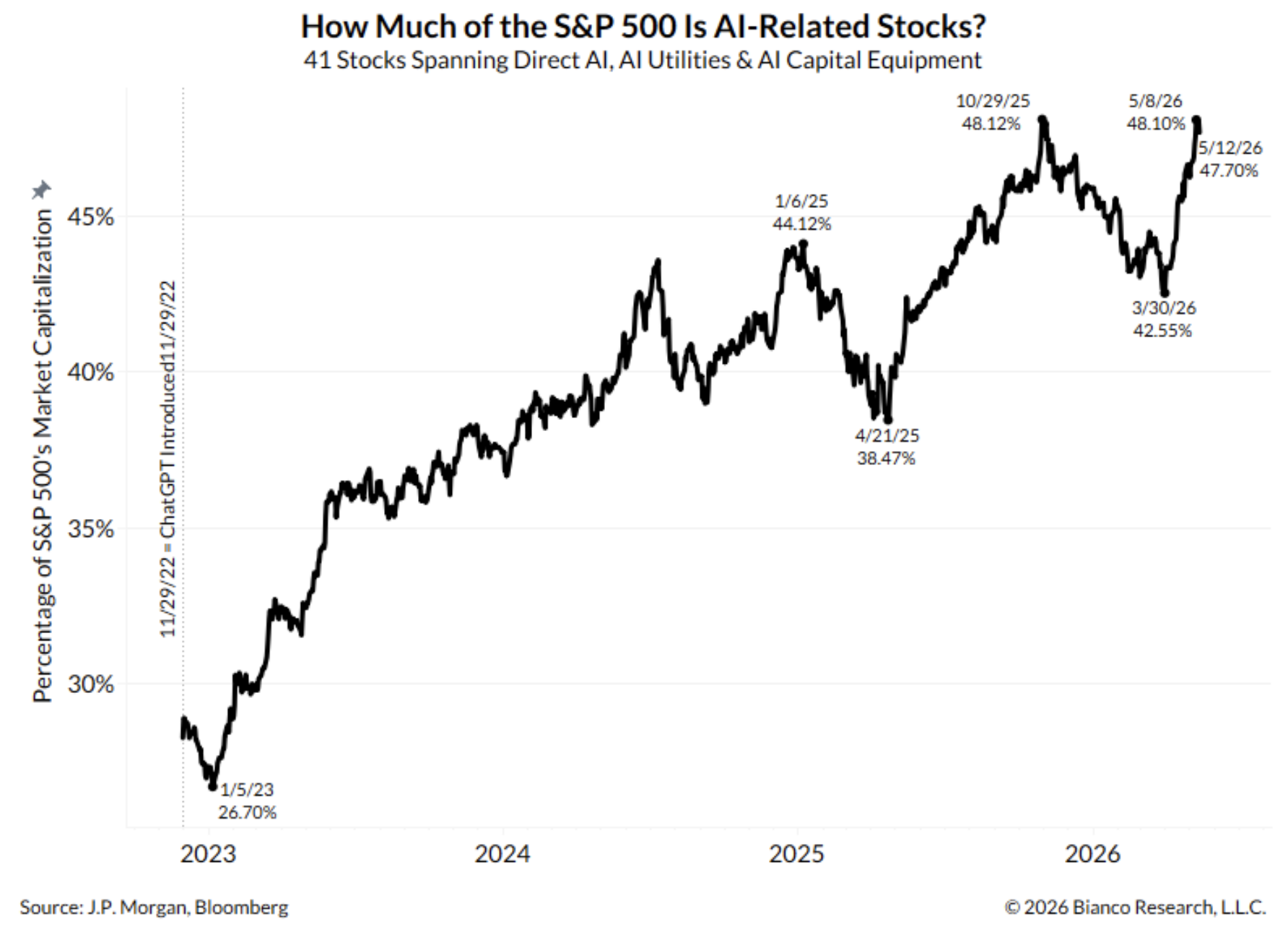

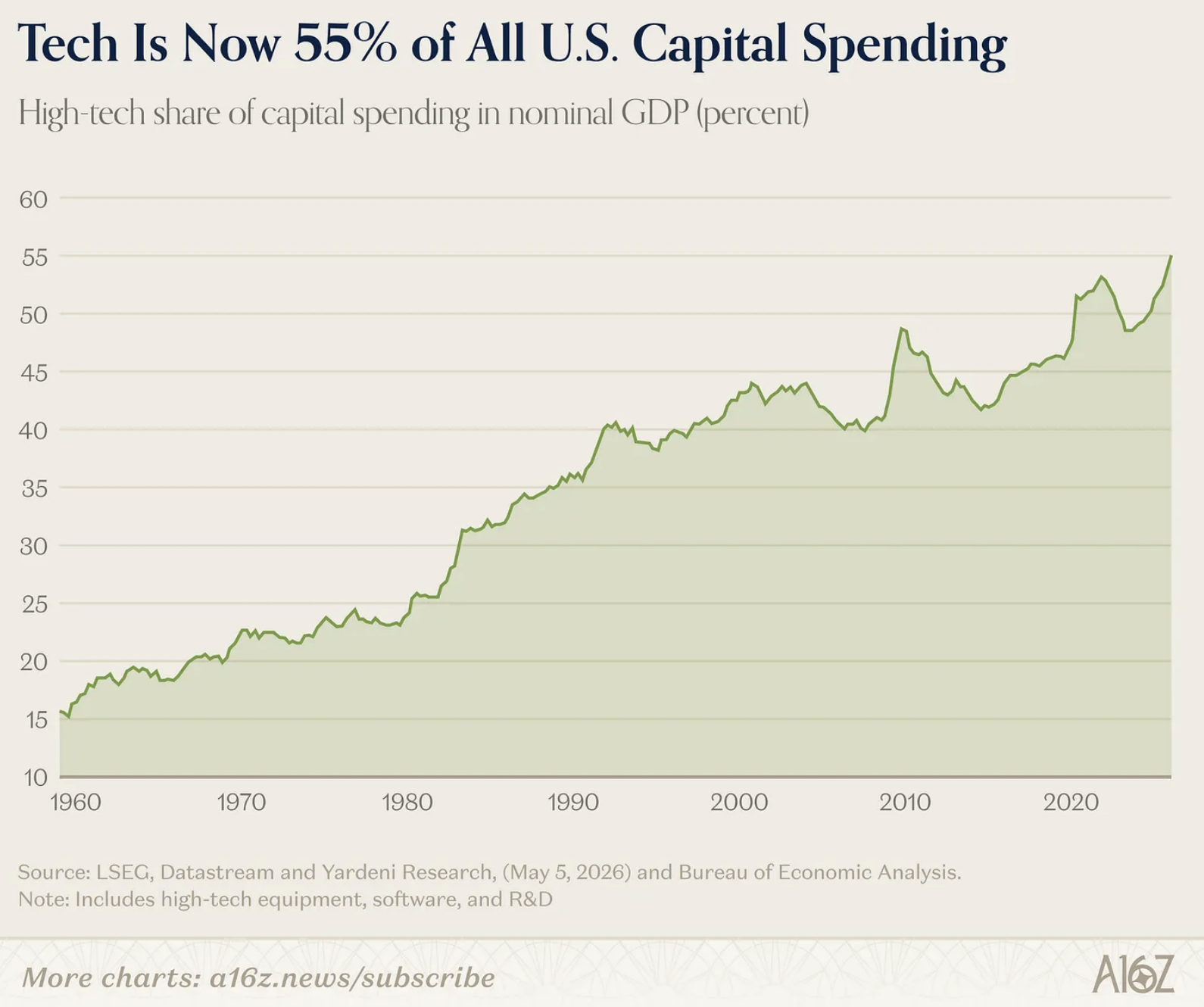

The Stock Market's Dirty Earnings Secret

S&P 500 earnings are up 27% year-over-year. That sounds fantastic. But Goldman Sachs estimates that if you remove Anthropic, the number drops to 16%.

Here's how it works: Amazon, Microsoft, and others own stakes in Anthropic. Anthropic's valuation went from roughly $60 billion to $380 billion in Q1 2026. That revaluation flows through to "other income" on corporate income statements and gets counted in S&P earnings.

Anthropic is now reportedly seeking a $900 billion valuation. Another massive "other income" boost could be coming in Q2.

This is a one-time, mark-to-market accounting phenomenon dressed up as operating earnings.

Roughly 40% of S&P earnings growth this year is attributable to Anthropic's private market revaluation. SB here - Worth knowing!!!

Source: Mauldin SIC2026, Bianco Research, A16Z

On U.S. Debt and Default

The U.S. will not default. Ever. It can print. The real risk isn't default, it's that we eventually print into massive inflation. Jim's Hemingway reference: "How does one go bankrupt? Slowly, then suddenly." We've been in the “slowly” phase for 40 years.

On AI and Wages

Companies are paralyzed. They're not extracting productivity from AI yet, but they're also not hiring, because they don't know what the next 6–12 months look like.

AI will automate tasks, not entire jobs. The productivity is still mostly promise, not reality.

Source: Bloomberg, Bianco Research

Source: a16z, Bianco Research

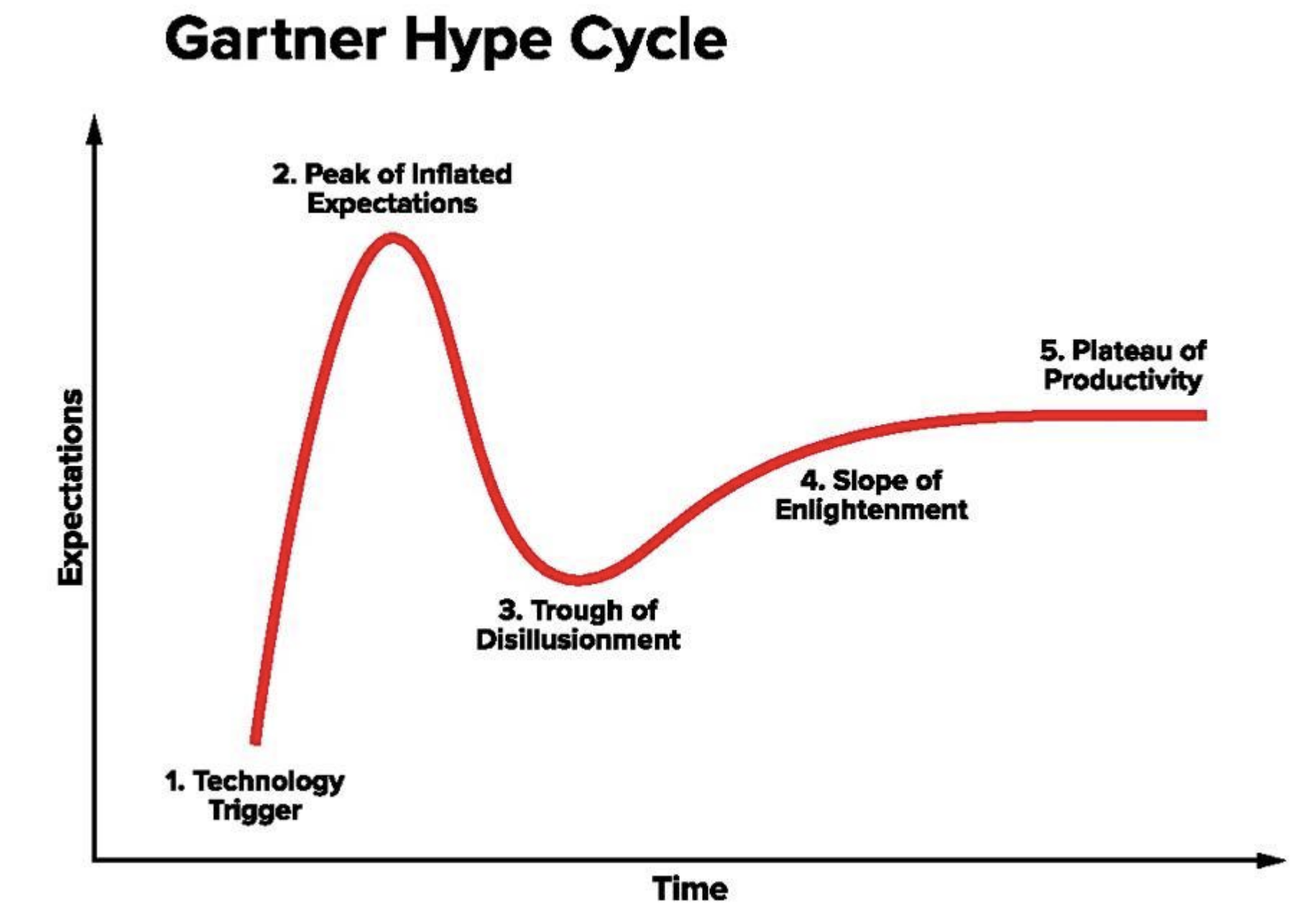

Are we near “Peak of Inflated Expectations?” Maybe. Spend a moment on this next chart:

Source: Bianco Research

Jim’s presentation was a dense, data-rich 50-minutes. You can follow him as he speaks frequently and posts regularly on X. He is one of the best in the business.

The key takeaways are this: inflation is structural, oil is the accelerant, the bond market is the judge, and the new Fed chairman has a very difficult road ahead.

A big hat tip to Ed D’Agostino for MC’ing the conference and, of course, to my good friend John Mauldin.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: May 28, 2026 Update

Market Commentary

Here’s the weekly recap through Thursday:

Subscribers - link below.

The Dashboard of Indicators follows next.

Trade Signals - subscribers only

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: The Beautiful Game

“Football is a universal language. It brings people together, irrespective of their nationalities, cultures or beliefs.”

- George Weah, Former Player and Current President of Liberia

George Weah is one of Africa's greatest football legends. He played professionally at the highest level from the late 1980s through the early 2000s, starring for Paris Saint-Germain, AC Milan, and Chelsea, among others. He won the Ballon d'Or in 1995 (MVP), becoming the first and still only African player to win it, and was named the FIFA World Player of the Year that same year.

There are weeks when writing about nuclear deterrence, trade wars, and geopolitical Rubik's Cubes feels heavy. This is one of those weeks. So let me end somewhere lighter.

In two weeks, the FIFA World Cup comes to Philadelphia’s “Philadelphia Stadium” (Lincoln Financial Field to Eagles fans), which will host six matches, including a Round of 16 game on July 4th. I'll be at that game and hopefully the Brazil - Haiti game in June. There are 16 host cities across the US, Mexico, and Canada. The opening game is in Mexico City on June 11.

Here is what I love about the World Cup: for 90 minutes, none of the macro analysis above matters. A kid from Brazil, a defender from Haiti, a goalkeeper from Ghana - they share the same pitch, the same rules, the same dream. As Mia Hamm put it recently, soccer allows us to understand that "we are more alike than we are different." She's right. It is the one universal language.

This year's tournament is historic. There are 48 teams, 104 matches, the most in World Cup history, and Philadelphia is right in the middle of it on the country’s 250th anniversary. Brazil plays Haiti on June 19th. France plays Iraq on June 22nd. Croatia, a legitimate contender, plays Ghana on June 27th. And then, on the 250th birthday of the United States, a Round of 16 match at the Linc.

There is something quietly poetic about that last one. On the day we celebrate American independence, the world gathers in Philadelphia — the very city where that independence was declared — to play the world's game together.

Spain is the current favorite at around +430, just edging out France at +500. England (+650) rounds out the top three, while Brazil (+800) is the biggest contender outside Europe. Argentina, the defending champion, is also in the mix. Source: CBSSports

This week, I've been writing about superpowers competing for position, trading spheres of influence, and managing the risk of catastrophic conflict. And then I think about 60,000 people packed into Lincoln Financial Field on the Fourth of July, waving flags from a dozen countries, sharing the same moment.

Maybe Pippa's right. Maybe we really are more alike than we are different.

Hope to see you at the Linc.

Wishing you and your family a wonderful weekend!

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.