On My Radar: Bravo Kevin Warsh

June 19, 2026

By Steve Blumenthal

“The US economy is right now running on a sugar high. The real skunk at the garden party is going to be inflation, which is going to creep back up. The gravity of interest rates hasn't gone anywhere.”

- Jamie Dimon, CEO, JP Morgan

A short post this week. You’ll find six good charts and a fun video post of Barry Habib and his team reflecting on our new Fed Chairman, Kevin Warsh’s first Fed meeting. I’m not sure how he can navigate his way out of the deficit and debt mess without printing money. Can he tap into the late great Fed Chairman, Paul Volcker? Warsh has his hands full. He’s talking tough. I hope he can stay tough.

It’s been a full week, and the USA plays Australia at 3 pm ET. I’m racing to hit the send button and position myself in front of the TV next to Coach Sue. To say we are excited is an understatement.

Quick aside, I am hosting a dinner in Atlanta next Thursday for clients and OMR readers. Space is limited. If you’d like to meet, enjoy some wine, and talk macro together, see the link in the personal section.

Grab that coffee and find your favorite chair. You’ll find a short summary from Barry Habib on Kevin Warsh, along with six charts worth your quick review.

On My Radar: Bravo Kevin Warsh

Personal Note: Happy Father’s Day!

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

Kevin Warsh’s First Meeting

Following is my summary of Barry Habib's MBS Highway post-Fed video update on Kevin Warsh's debut as Fed Chair. You can view the full replay [here].

Warsh's first meeting drew praise from both sides of the aisle. He commanded the room, and it's clear he's already reshaping how the Fed communicates.

The Fed held rates unchanged at 3.625%, with a unanimous vote, no small feat given how many Fed members had been publicly floating hikes beforehand

The statement itself was short and to the point, a sharp departure from the multi-page statements of the Powell era

Warsh gave zero forward guidance, and when reporters pushed him to characterize future moves, he was direct: he wasn't going to play that game

He even declined to submit his own dot in this meeting's dot plot, telling the room the Fed brought "a pencil with an eraser," a pointed signal that he sees the dot plot as a flawed exercise likely to change going forward

Still, this week's dot plot showed roughly half of Fed members penciling in a hike by year-end, so the committee is leaning hawkish even as its new chair distances himself from the tool that shows it

On substance, Warsh laid out an ambitious reform agenda:

He's forming task forces across five areas, including Fed communications, balance sheet policy, and the Fed's own data sources

On press conferences: he hinted he may not hold one after every meeting, saying a press conference is warranted only "when you have something important to say"

On the balance sheet: Warsh is no fan of its current size, and a smaller balance sheet has real disinflationary implications. He noted that money supply growth in excess of output is inflationary, a direct nod to the Fed's December 2025 QE expansion, which Barry has flagged before as an inflationary impulse

On market signaling: Warsh argued that less forward guidance lets markets react to actual data rather than to Fed messaging about future Fed reaction, which is how price discovery should work

On data quality: he's pushing the Fed toward real-time, private-sector data sources rather than lagging, frequently-revised government releases, an explicit reference to the jobs report's history of large revisions

On inflation: Warsh reaffirmed the 2% target, while leaving room for the Fed's broader policy framework to evolve as these task forces report back, likely before year-end

Barry's bottom line, and mine: this is the first Fed chair in a long time who seems to genuinely understand the mechanics of money supply, data quality, and Fed communication, and who's willing to act on it. Worth watching how quickly these task forces produce real change.

Click on the image - we start at the 2 minute 43 second mark.

Source: MBS Highway June 18 2024

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

If you like what you are reading, click on the link and share it with a friend (it’s free).

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not intended to recommend buying or selling any security and is for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Six Good Charts

I do find myself on social media more than I’d like to admit. When I come across a post I find meaningful, I bookmark it to share with you later. The following are a few that are notable from this past week:

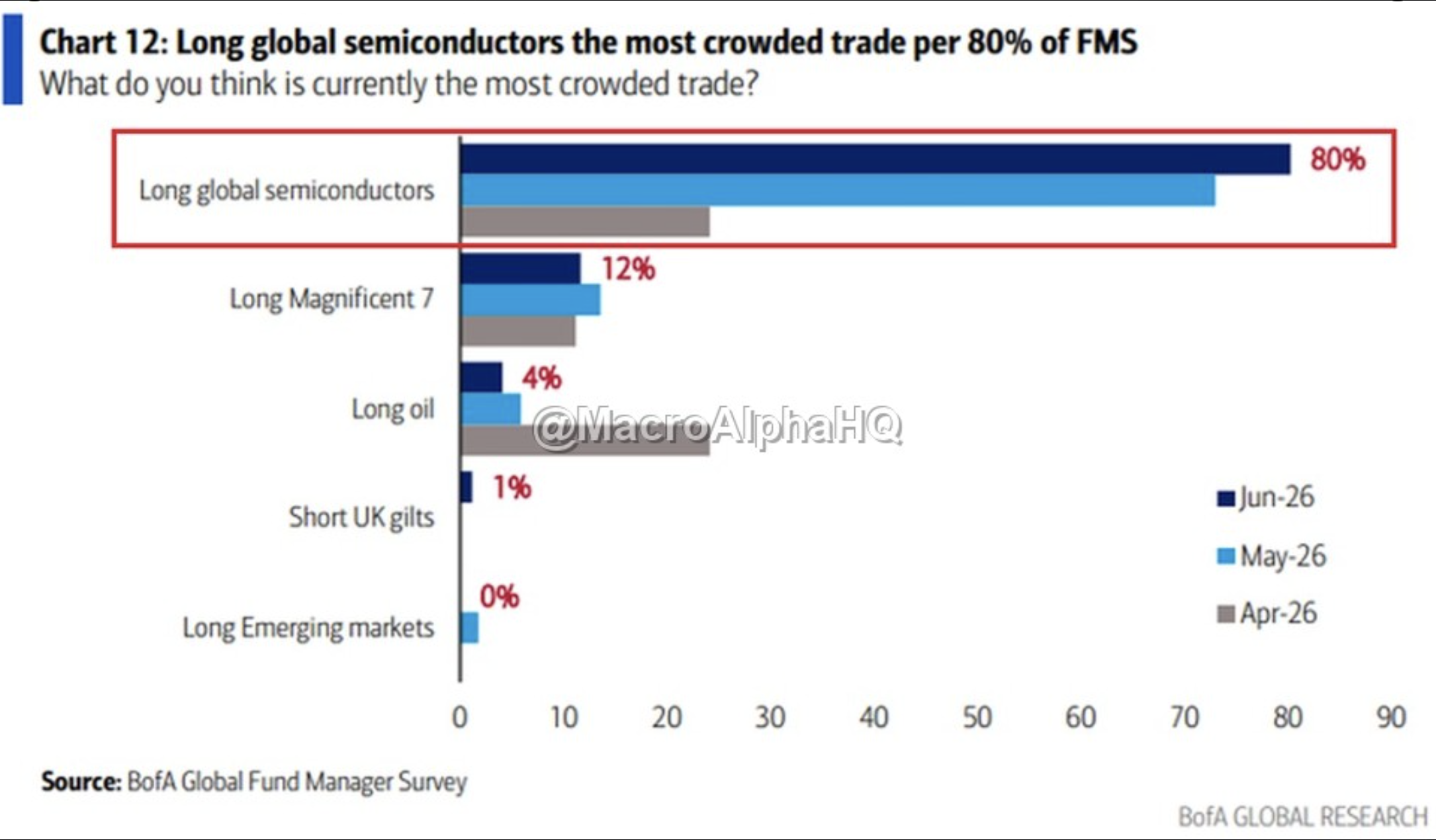

1) From @MacroAlphaHQ:

“The latest BofA survey is essentially a signed death certificate for the semiconductor trade. 80% of global fund managers are now consensus long. Let that absolute absurdity sink in for a second. That is the highest crowding metric since the peak of the zero-interest rate tech bubble in October 2020. The AI reply-guys genuinely believe this is a permanent structural paradigm shift. In reality, it is nothing but a historic concentration of passive flows waiting for a singular LIQUIDITY shock. When every single participant is crammed into the exact same side of the boat, there is absolutely zero marginal buying power left. Primes are already quietly adjusting their margin haircuts on $SMH behind closed doors. The fact that Mag 7 crowding collapsed to 12% tells you exactly how violently capital has been herded into this one hyper-specific sub-sector. Institutions are weaponizing your euphoria to systematically distribute their bags at the absolute top of the cycle. You are not front-running the future of global compute. You are providing premium exit liquidity for the most obvious cyclical top in a decade.”

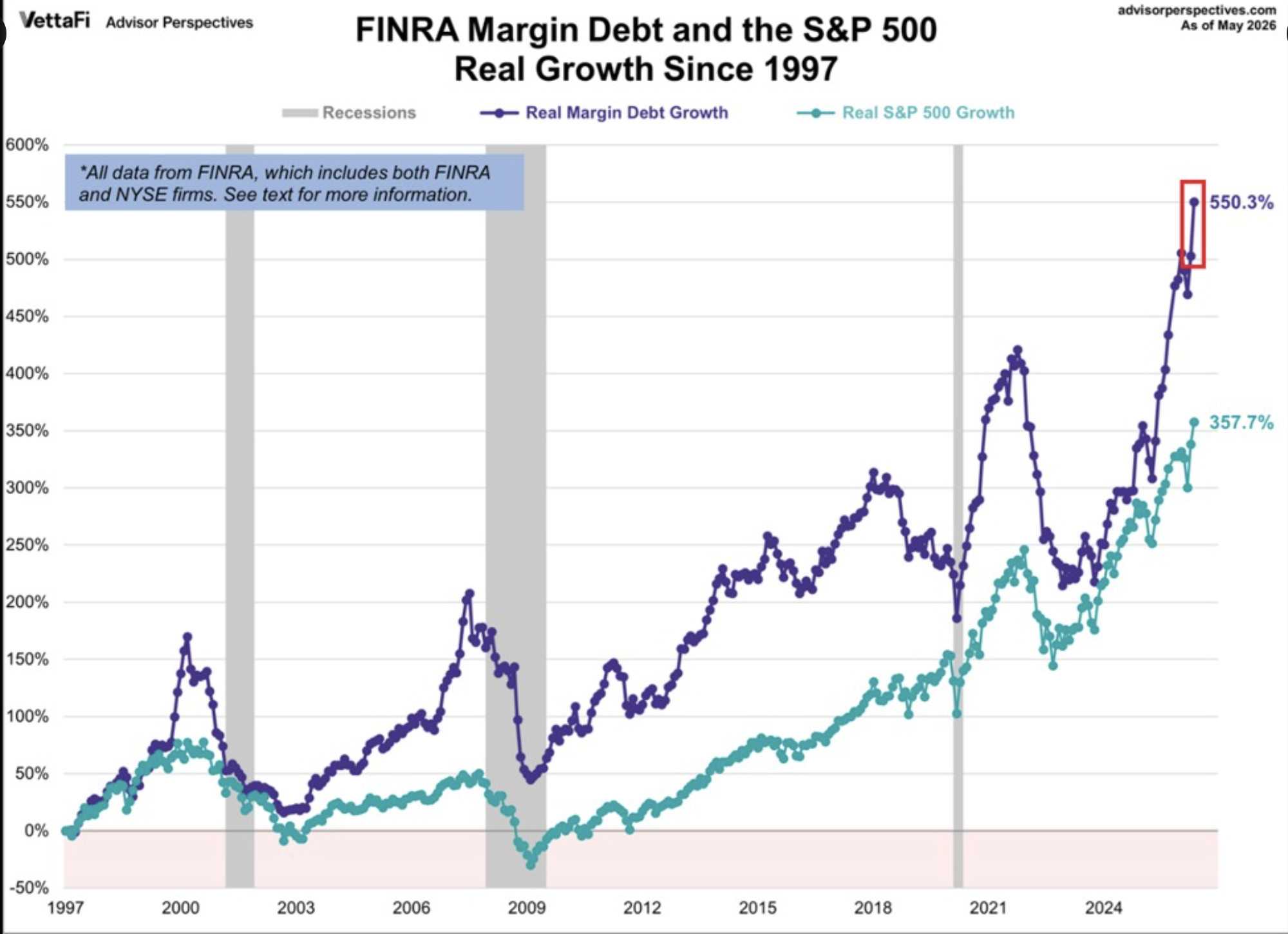

2) From @KobeissiLetter:

BREAKING: US margin debt jumped by +$112 billion in May, to a record $1.42 trillion. This marks the 2nd consecutive monthly increase, totaling +$195 billion. Margin debt has surged +$495 billion, or +54%, over the last 12 months. Adjusted for inflation, this metric rose +7.9% MoM and +47.4% YoY. Real margin debt has now grown +550% since 1997, far outpacing the S&P 500’s real gain of +357.7% over the same period. Market leverage continues to rise at a historic rate.

Source: VettaFi, Advisor Perspectives via @KobeissiLetter

3) From @ludoonchart - Jamie Dimon

Jamie Dimon just spoke at the Council on Foreign Relations and absolutely destroyed the toxic complacency currently infecting Wall Street. Instead of delivering the usual corporate optimism, he dropped a brutal reality check on the illusions driving the current market: "The US economy is right now running on a sugar high. the real skunk at the garden party is going to be inflation, which is going to creep back up. the gravity of interest rates hasn't gone anywhere.” "You sit in these endless executive meetings, and the first thing management does when they can't drive organic growth is start pitching m&a. i don't want to hear that bullshit.” “Massive government deficits and booming private credit markets have created an environment where players have completely lost touch with reality. A market that hasn't seen a real credit cycle in forever breeds a complacency that never ends well."

Worth the time - click on the photo:

Source: Council on Foreign Relations, @ludoonchart

I’ll watch it in full this weekend and share my summary notes with you next week.

4) From @PeterMallouk on Earnings and the S&P 500 Index

Before you view the next chart, keep in mind that I’m in full agreement - if your investment time horizon is 30 years. If you are 65, like me, can you afford for your $1 million S&P 500 Index investment to be worth $1 million ten years from now? Similar to the 2000-2010 period. No gain, and a likely large loss of value to inflation. I totally agree with the correlation, I just don’t believe most investors can stay the course. Especially if you are more senior in life and need your investments to provide for you.

“126 years of market history tell a simple story... Stocks and earnings move together with a 98% correlation. The short run is all about noise. The long run is all about profits. Speculators chase noise. Investors follow profits.”

Source: @PeterMallouk, Creative Planning

5) Ray Dalio

SB note - good luck, Kevin Warsh

Source: X, @RayDalio

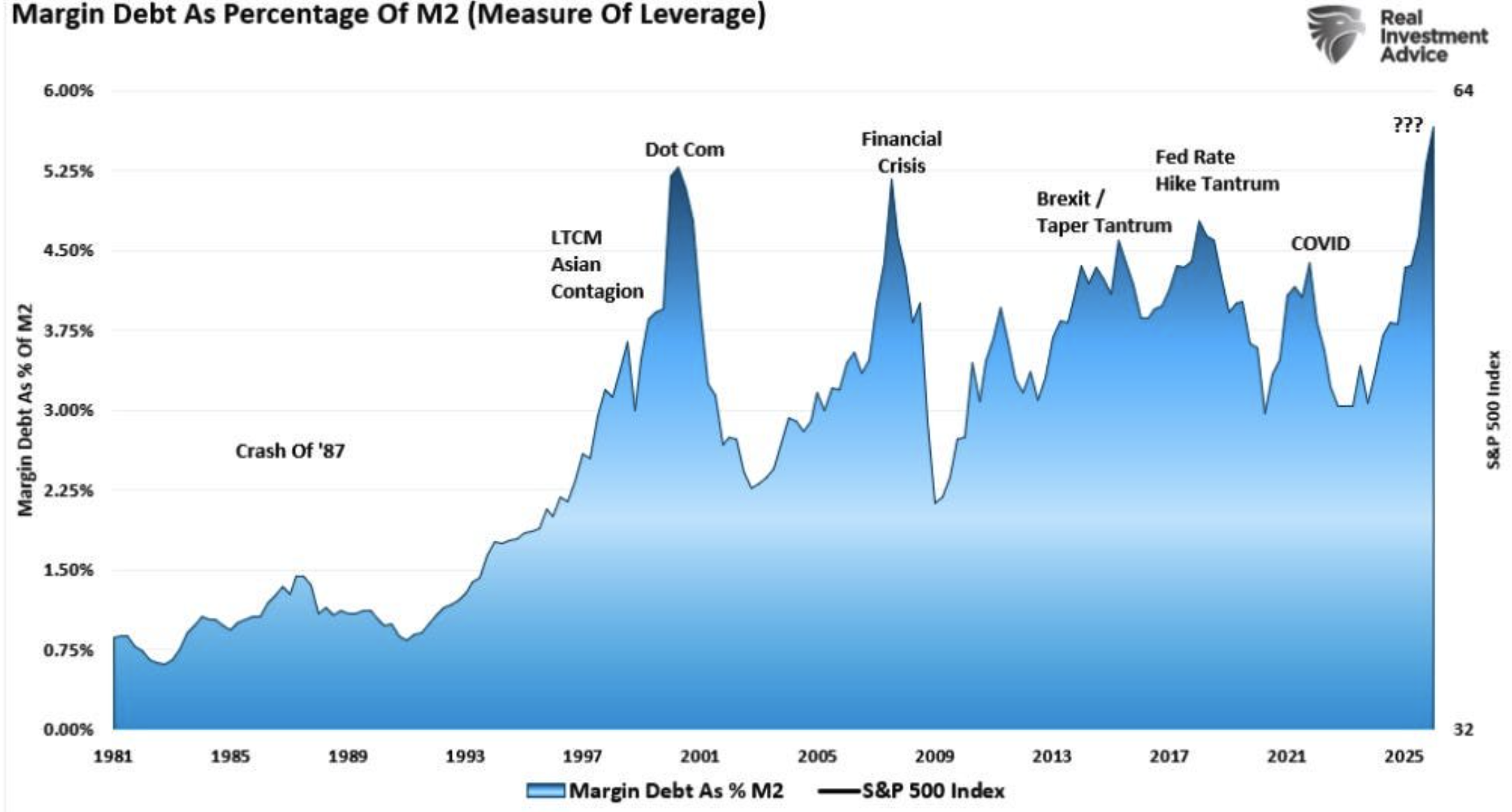

6) Margin Debt As a Percentage of M2 (a measure of leverage):

From @RonStoeferle - “Nice one by @LanceRoberts on margin debt: “Measured against M2, it’s back near the peaks that preceded the 2000 and 2007 tops. Borrowed money cuts both ways. It is an accelerant, not a cushion."

Source: @RonStoeferle, @LanceRoberts, Real Investment Advice

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: June 18, 2026 Update

Market Commentary

A chart worth watching closely:

Focus on the diagonal arrow at the bottom right of the chart.

The bottom section plots the Monthly MACD trend signal. The monthly signals tend to indicate the dominant trend.

The current signal is nearing a rising-interest-rate signal.

You can see that prior signals have tended to last several years.

A break higher is bearish for bonds, concerning for inflation and the economy in general.

Keep a close eye on this one!

Source: StockCharts.com, CMG notations

Subscribers - link below.

The Dashboard of Indicators follows next.

Trade Signals - subscribers only

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: Happy Father’s Day

Racing to get this post to the edit team with plans to be in front of the television next to Susan to watch the US vs Australia game, which kicks off at 3 pm ET. We are thoroughly enjoying the World Cup.

Both teams won their opening game. Each bracket has four teams. Each team plays each other once, and the top two teams from each bracket advance to the elimination round. The winner of this game will advance to the next round, but a loss doesn’t kill either team’s chances. Let’s go USA!

I’ll be hosting a casual dinner in Atlanta for clients and OMR readers on Thursday evening, June 25. Please join me if you can. Space is limited. If you are interested in joining, please email Amy@cmgwealth.com.

Happy Father’s Day! I am so grateful to be a father. I’ll be golfing with my daughter Brianna, who is home for the weekend. And watching the US Open. Maybe some wine, too!

On the bookshelf in my office is my old man’s Phillies hat. Dad graduated in 2011. Miss him dearly. Also shown is CMG’s second dad, Len Siegel. We’d have lunch with Len about once a quarter. Also, another wonderful man we think of often. Happy Father’s Day, men! Grateful!!!

Glasses, high-here’s to a wonderful Father’s Day!

With kind regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.