On My Radar: Zulauf - Gundlach

June 26, 2026

By Steve Blumenthal

“The only permanent truth in finance is that people will get bullish at the top and bearish at the bottom.”

- James Grant

This week, I had the opportunity to listen to Felix Zulauf and Jeffrey Gundlach share their views on the markets, inflation, interest rates, the AI boom, and gold and commodities. Their discussion was thoughtful and, in my view, well worth the time. Below is a summary of my key takeaways, along with a link to the replay. I hope you find it helpful.

It was a difficult week for technology stocks, while the broader market showed surprising resilience. Monday's weakness accelerated into Tuesday's semiconductor-led selloff. At the time of this writing (Friday, 2:00 p.m. ET), the tech-heavy Nasdaq is down 3.4% for the week, with the Magnificent Seven bearing the brunt of the decline.

In contrast, the Dow held up relatively well, and small-cap stocks continued to outperform. The Russell 2000 closed at a record high, adding to the evidence that investors may be beginning to rotate away from the mega-cap technology leaders.

Overseas, Asian markets came under heavy pressure overnight. South Korea's Kospi briefly triggered a circuit breaker after falling more than 8%.

The bond market was a bit more constructive. The 10-year Treasury yield slipped back below 4.40%, oil prices moved lower, and inflation expectations eased. Thursday's PCE inflation report came in largely as expected, providing markets with modest relief.

Brent crude fell more than 4% this week and is trading near $72 per barrel as progress in U.S.-Iran negotiations eased immediate concerns about a disruption in the Strait of Hormuz. Oil has now retraced nearly all of its geopolitical risk premium.

That said, remain alert. The U.S. reported today that Iran violated the ceasefire by launching a drone strike against a cargo ship. Interestingly, the oil market barely reacted. For now, traders appear willing to look past the headlines—but that could change quickly if tensions escalate. Source: CNBC

Here is a quick look:

Source: StockCharts.com

The U.S. Dollar Index (DXY) climbed above 101.7 mid-week, its highest level since March 2025 and now up roughly 3.5% year-to-date. The move continues to reflect expectations that the Federal Reserve will keep interest rates higher for longer.

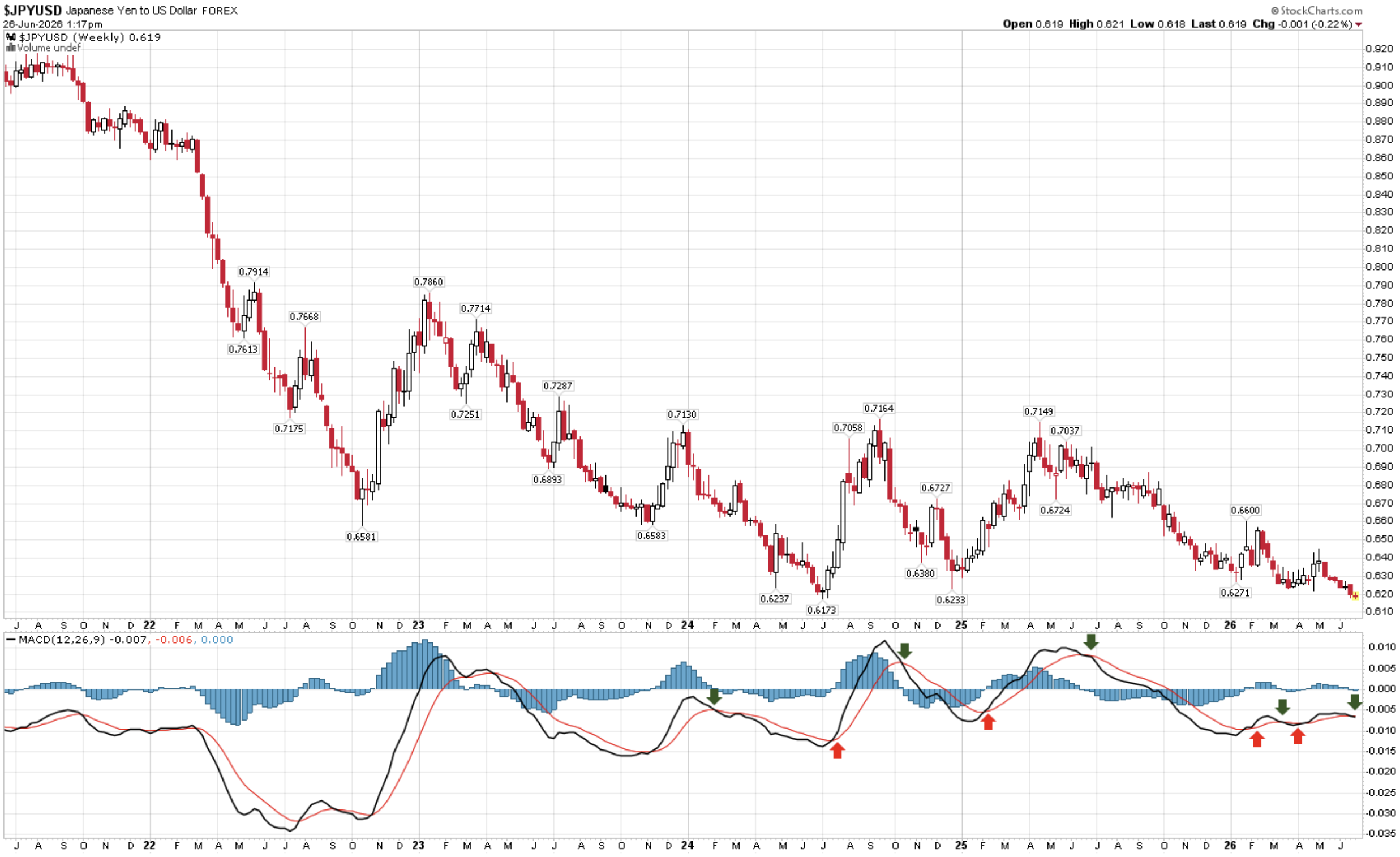

One market I continue to watch closely is the Japanese yen. The leveraged Yen Carry Trade remains an important source of global liquidity. A stronger dollar and weaker yen generally support that trade, helping to provide liquidity to global financial markets. The downside is felt in Japan, where a weaker currency makes imports—especially energy—more expensive. Because Japan imports most of its oil, a weaker yen means it takes more yen to buy the same barrel of crude. That is part of the inflationary challenge Japan continues to face.

The following chart is one I've shared in prior On My Radar letters. The yen remains near its weakest level since 1986 despite repeated warnings from Japan's Ministry of Finance and last spring's record currency intervention. While the Bank of Japan continues to signal gradual interest rate hikes, the wide yield gap between Japan and the United States continues to keep pressure on the currency.

We'll continue to watch the yen closely. I believe it remains one of the most important—and underappreciated—drivers of global liquidity and financial market risk. Source

Gold is on pace to lose roughly 5% this week, slipping back toward the $4,000 level as a more hawkish Federal Reserve and a stronger U.S. dollar weighed on prices. Even with this week's decline, gold remains well above where it began the year. Thursday's PCE inflation report, which came in largely as expected, helped gold recover modestly as fears of an even more aggressive Fed eased. Broader commodity markets also weakened alongside oil as geopolitical concerns surrounding the Strait of Hormuz continued to fade.

Bottom line: Markets are adjusting to a more hawkish Federal Reserve. Interest rate expectations have moved higher, the dollar has strengthened, and both gold and technology stocks are taking a well-deserved breather following exceptionally strong advances.

My longer-term view remains unchanged. I continue to believe gold, commodities, and other hard assets are likely to benefit from the structural forces that lie ahead. Excessive debt, persistent fiscal deficits, and mounting entitlement obligations point toward a period of fiscal restructuring and policies that, over time, should favor real assets over richly valued financial assets.

We'll take a fresh look at the mid-year valuation picture next week. My conclusion remains the same: valuations matter. As Jeremy Grantham writes in the excerpt below, we're in "the most expensive market in American history." Whether or not you agree with that assessment, today's valuations suggest investors should temper their expectations for long-term returns from the cap-weighted S&P 500.

Grab that coffee and find your favorite chair.

On My Radar: Zulauf - Gundlach

Personal Note: World Cup Update - More Than a Game

OMR is for informational and educational purposes only. No consideration is given to your specific investment needs, objectives, or tolerances.

Please see the Important Disclosures at the bottom of this page. Reminder: This is not a recommendation to buy or sell any security. My views may change at any time. The information is for discussion and educational purposes only.

If you like what you are reading, you can subscribe for free.

Felix Zulauf - Jeffrey Gundlach

You can find the replay by clicking on the image. My bullet point summary notes immediately follow.

Source: DoubleLine, Zulauf, YouTube

Grant Williams welcomed viewers and asked both Felix Zulauf and Jeff Gundlach to give an overview of how you see the world today, what concerns them, and where they see opportunities.

I’ve organized my notes in bullet point format to get you right to the major discussion points. You’ll find the following topic categories: Macro Outlook, The Dollar, Bonds, and Emerging Markets, Gold, Entitlements, Debt and Social Stability, Government Repression, AI Bubble, Private Credit, Japan, and the Bottom Line Summary (Main Views).

Macro Outlook

Feliz Zulauf (FZ):

We are witnessing two major developments.

First, the geopolitical order is changing. The world is moving from a unipolar system toward a multipolar one. The United States is attempting to maintain its dominant position, but cannot fully do so. This transition creates conflict, wars, sanctions, and geopolitical instability. Wars and sanctions are inflationary.

Second, economically:

Europe is in structural decline.

China remains in a long-term rise but is trapped in a deflationary cycle.

The U.S. economy has benefited from years of easy money and is now dominated by an AI-driven capex boom.

The combination of easy money and transformative technology is extremely powerful for financial markets. However, I believe we are in the late stage of this cycle.

I cannot say exactly when the bubble will burst, but I expect:

Equity markets may peak sometime between late 2026 and early 2027.

A classic bear market follows.

The decline could be 30%-50%, not merely 20%.

The downturn will be driven by both recession and valuation contraction.

The next recession will expose the enormous debt burdens accumulated globally and create systemic stress.

Jeffrey Gundlach (JG):

I largely agree with Felix. For about seven years I've believed we reached the end of the secular decline in U.S. Treasury yields. Everything investors learned over the last 40 years was shaped by falling interest rates.

The question is: what happens when rates trend upward instead?

JG’s conclusion:

U.S. debt levels make sustained declines in long-term rates difficult.

Interest expense on the U.S. government debt has exploded from roughly $300 billion annually to about $1.4 trillion.

Budget deficits continue to expand.

Even if a recession arrives, long-term Treasury yields may rise rather than fall. That would be historically unusual.

Potential outcomes include:

Yield Curve Control (government caps long-term rates).

Treasury debt restructuring (extending maturities and reducing coupons).

Neither option would be positive for bondholders.

The Dollar, Bonds, and Emerging Markets

JG: During previous stock market corrections:

The U.S. dollar typically strengthened.

In 2025's tariff-related correction:

The dollar weakened instead.

This is evidence that the old playbook is breaking down. He expects:

A weaker dollar.

Better relative performance from emerging markets.

Stronger returns from non-U.S. assets.

Investors should diversify away from U.S.-only portfolios.

FZ: I agree on the long-term bearish outlook for the dollar. However, I am less optimistic about emerging markets during a global recession.

Many emerging economies depend on exports. A recession would reduce demand and create difficulties for them.

He believes:

The dollar may strengthen temporarily.

Longer-term, the dollar enters a secular decline.

One important difference this cycle:

Foreign investors increasingly bought U.S. AI stocks rather than Treasuries. When those investors eventually sell:

They will sell both stocks and dollars.

That could accelerate dollar weakness.

Gold

JG: Traditional indicators no longer work. Examples:

Copper/gold ratio no longer predicts Treasury yields.

Consumer sentiment models have broken down.

Gold has become increasingly important as a monetary asset.

Central banks continue accumulating it.

FZ: Gold behaved differently than historical relationships would suggest. Normally:

Gold rises when inflation rises.

This cycle:

Gold rose while inflation fell.

The key driver has been Chinese buying. The larger story is trust.

Countries no longer trust storing reserves in another country's currency.

Gold solves that problem because:

It can be held domestically.

It is not dependent on another government's policies.

He believes the secular gold bull market remains intact.

Entitlements, Debt, and Social Stability

JG: Social Security's funding situation is deteriorating rapidly. The projected exhaustion date keeps moving closer. What once seemed like a problem for future generations is becoming an immediate issue.

The government may eventually need to:

Reduce benefits.

Restrict eligibility.

These decisions will be politically difficult to make.

FZ: This is not only a financial issue. It is becoming a social issue.

Across Europe:

Protest parties are gaining support.

Traditional parties are losing influence.

People are increasingly frustrated by declining living standards and government priorities.

The next recession will amplify these social tensions.

Government Repression

FZ: Financial repression will intensify. Governments will increasingly change the rules.

Examples might include:

Requiring banks to hold more government bonds.

Requiring pension funds and insurers to hold more government debt.

Central banks ultimately absorbing large quantities of government debt.

Policymakers are no longer pursuing optimal solutions

They are merely trying to keep the system functioning.

JG: I agree. At some point, governments may become much more aggressive in managing debt burdens. What seems impossible today often becomes inevitable when circumstances worsen. (SB here: signs to look for in terms of the grand restructuring ahead)

AI Bubble

GW: How do you see the AI boom developing?

FZ: The hyperscaler’s have dramatically increased capex (capital expenditures). Capex has risen from roughly:

10% of sales, to

30% of sales.

Semiconductor shortages have pushed costs sharply higher.

The key issue: The largest AI investors are approaching the point where:

Free cash flow is deteriorating.

Additional financing becomes necessary.

Eventually, management teams will decide the spending is unsustainable.

When that happens:

AI spending growth slows.

Momentum turns.

Historically, the leading stocks often double in the final six months before a bubble peaks.

Semiconductor stocks are particularly important indicators.

JG: I agree. The most dangerous phase is when:

Fundamentals deteriorate,

But stock momentum remains strong.

That's where we are now. The AI buildout is creating real-world constraints:

Electricity shortages.

Water shortages.

Community opposition.

The problem isn't just capital. It's also physical resources.

Private Credit

JG: I've become increasingly concerned about private credit. The first warning sign was hearing industry participants discussing:

Liquidity pressures.

Difficulty exiting investments.

Then I learned about identical loans being valued dramatically differently by different managers.

Examples included:

One manager marking a position at 95.

Another marking the same position at 8.

Additional concerns:

Questionable ratings practices.

Weak transparency.

Illusions of liquidity.

Ties between private credit, private equity, insurers, and offshore reinsurance structures.

This reminds me of 2005-2006 before the Global Financial Crisis.

Cracks are already appearing.

Defaults are rising.

Funds are being marked down.

He believes the risks are larger than many investors appreciate.

FZ: Private credit itself won't disappear. But some private credit firms will. I monitor the industry closely.

One advantage is that financing requests reveal which industries are experiencing stress.

Collateral quality remains crucial.

The industry will survive, but not every participant will.

Japan

JG: Japan's rising yields remain a concern.

The country's currency pressures suggest underlying instability.

This isn't positive for the global economy.

FZ: Japan's debt problem is somewhat manageable because most debt is domestically owned. However:

Demographics are deteriorating.

Japan is caught between China and the United States geopolitically.

I expect:

Further efforts to strengthen the yen.

Potential rate hikes.

The key issue will be whether Japanese investors begin repatriating overseas capital.·

That could have major consequences globally.

Bottom Line Summary (Main Views)

Felix Zulauf Core Thesis

The world is transitioning from a U.S.-led order to a multipolar order.

Geopolitical conflict is inherently inflationary.

The AI-driven bull market is in its late stages.

Equities likely peak between late 2026 and early 2027.

A 30%-50% bear market is possible.

Recession and debt stress will create systemic problems.

Gold remains in a secular bull market.

The U.S. dollar enters a secular decline after a final period of strength.

Financial repression will intensify.

Social unrest and political fragmentation will increase.

Jeff Gundlach Core Thesis

The 40-year bond bull market is over.

Rising debt levels make lower long-term yields difficult.

Future recessions may coincide with rising bond yields.

Yield curve control or debt restructuring become possible policy responses.

The dollar's historical safe-haven status is weakening.

Investors should diversify away from U.S.-centric portfolios.

Gold becomes increasingly important as real money.

AI remains a bubble-like environment with resource constraints.

Private credit resembles pre-2008 conditions.

Entitlement systems face serious funding stress.

The global financial system is entering a new regime unlike anything investors experienced over the last four decades.

Both Agree:

The debt burden is unsustainable.

Financial repression is coming.

The dollar weakens over the long term.

Gold benefits from declining trust in fiat systems.

The AI boom is in its late stages.

A major recession and bear market are likely within the next 1-2 years.

The next downturn will be more severe than a normal cyclical recession because of debt, politics, and social tensions occurring simultaneously.

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

If you like what you are reading, click on the link and share it with a friend (it’s free).

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

Not a recommendation to buy or sell any security. Please note that the information provided is not intended to recommend buying or selling any security and is for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Rosenberg and Grantham

Last night, I hosted a dinner in Atlanta for clients and OMR readers. A smart group, and the discussion was engaging.

We were talking about Warsh, the challenges he faces tied to inflation, debt and entitlement issues (social security running out of money in 2032). Grant J., who runs a family office, shared a nice quote from a Wednesday David Rosenberg letter. In short, there remains a put below the market. That’s the point at which the Fed comes to the rescue. However, that protection point is likely much lower than Jerome Powell’s put (remember the Powell Pivot?).

Rosenberg points to a WSJ article that writes, “The return of inflation after the pandemic has left a question mark over whether the Put still exists—and plenty of debate about whether it is a good thing.”

From Rosie,

“The Fed Put Will Be Repriced Under Warsh: The best read of the morning goes to page B1 of the Wall Street Journal: Can the Market Still Bet on the ‘Greenspan Put’?

It may be early days, but it does seem as though the Kevin Warsh appointment to lead the Fed will prove to be as transformational as Volcker replacing Miller in 1979.

This by no means suggests that a market meltdown or a freeze-up in credit conditions would fail to elicit a policy response, but it is to say that this new Fed Chairman likely has his strike price for intervention at a far lower level than we have become accustomed to seeing.”

I believe Warsh will allow markets to experience more pain. How much remains a large question mark.

Regardless, I believe a grand restructuring of the debt and currency markets remains ahead. It will likely take great pain to get the job done. Inflation and higher interest rates are the likely trigger.

Jeremy Grantham

“Veteran investor Jeremy Grantham thinks the artificial intelligence boom has pushed the U.S. stock market to its most expensive level ever and could eventually lead to a historic decline.

“Based on the value of the stock market compared to GDP, with modifications, this is the most expensive market in American history,” Grantham told CNBC’s “Squawk Box.”

While the GMO co-founder said he wasn’t sure there was a comparable period, the tech bubble of 2000 is the closest analogy. He also highlighted the so-called Buffet indicator, which compares the total value of the U.S. stock market valuation with the size of the economy in terms of GDP.

The market capitalization to GDP ratio referenced by Grantham is estimated to be at 235%, according to Longtermtrends.com. It means that the value of the total stock market is more than two times the size of the U.S. economy.

Legendary investor Warren Buffett used this indicator, saying years ago that when it “approaches 200% — as it did in 1999 and a part of 2000 — you are playing with fire.”

Graham said that, while the timing was terribly uncertain, markets could potentially peak.”

On SpaceX, he said, “He said historians may eventually view the company’s public-market debut as “one of the defining peaks of all time.” And added, “It’s the thing you see around the top.” Source: CNBC

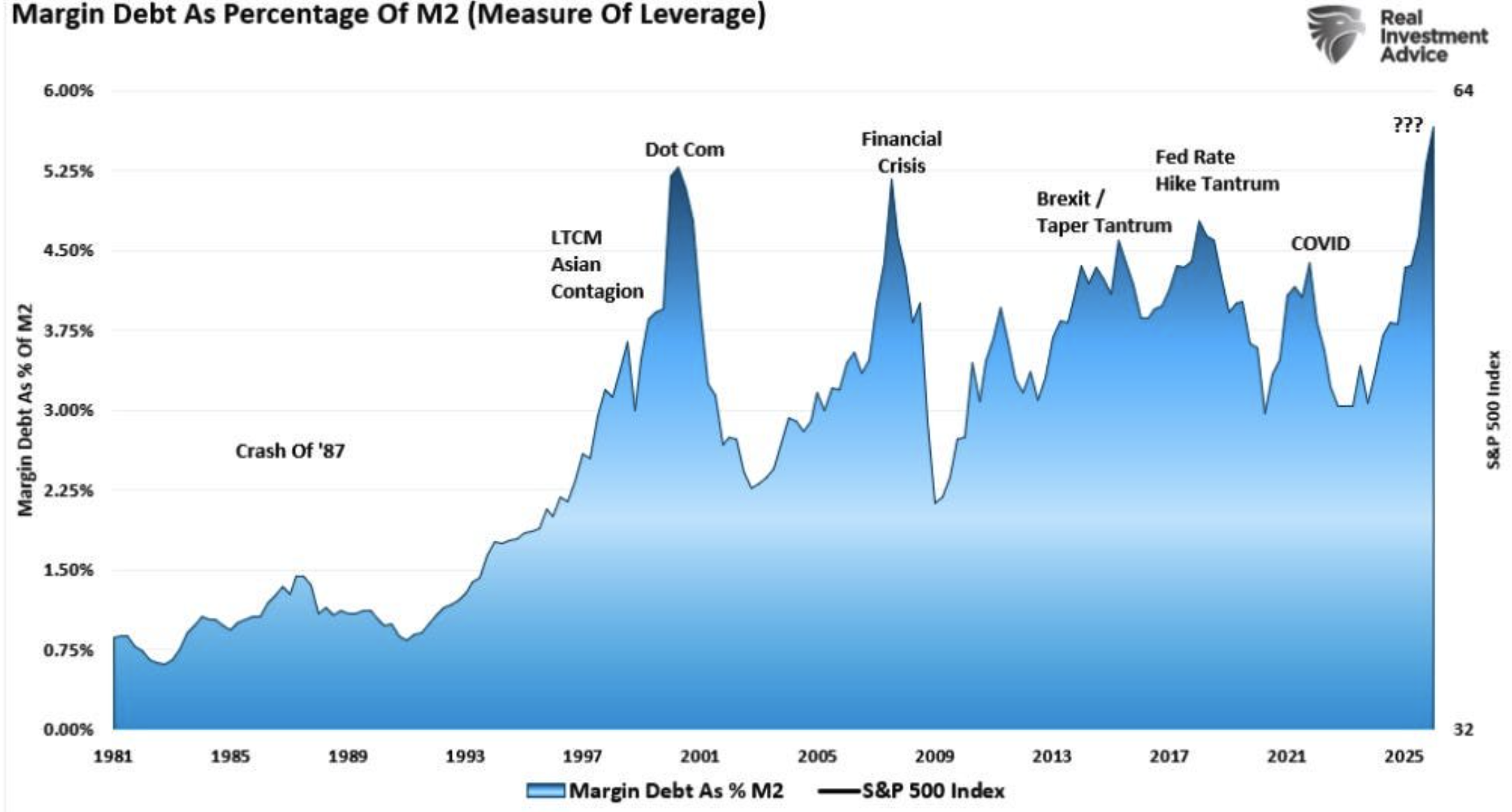

Margin Debt

Resharing this chart that I posted last week. Simply because it matters!

Source: @RonStoeferle, @LanceRoberts, Real Investment Advice

Opinions are subject to change. Not a recommendation to buy or sell any security. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Trade Signals: June 25, 2026 Update

Market Commentary

Subscribers - link below.

The Dashboard of Indicators follows next.

Trade Signals - subscribers only

The Indicators Dashboard - Stocks, Investor Sentiment, Bonds, Commodities, Currencies, and Gold

Valuations and Subsequent 10-year Returns

Supporting Charts with Explanations

About Trade Signals - Trade Signals is a paid subscription service that posts the daily, weekly, and monthly trends in the markets (and more). Free for CMG clients. Not a recommendation to buy or sell any security. For discussion purposes only.

“Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it’s that simple.” – Charlie Munger

TRADE SIGNALS SUBSCRIPTION ACKNOWLEDGEMENT / IMPORTANT DISCLOSURES

The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice. Not a recommendation to buy or sell any security.

Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only. Current viewpoints are subject to change. Please note that the information provided is not recommended for buying or selling any security and is provided for discussion purposes only.

Personal Note: World Cup Update – More Than a Game

I spent several days in Atlanta this week. The trip combined business and pleasure—conducting due diligence on a real estate opportunity, hosting a wonderful dinner with clients and On My Radar readers, and attending one of the biggest sporting events on the planet: the FIFA World Cup.

The match featured Haiti and Morocco. Morocco needed a result to advance to the knockout stage. Haiti knew its World Cup journey would end that evening regardless of the outcome.

If you've never experienced a World Cup match in person, it's difficult to appreciate what it means to the fans. Americans love sports—I certainly do—but the World Cup is something altogether different. For much of the world, it's more than a game. It's country, culture, family, pride, and hope wrapped into ninety unforgettable minutes.

I found myself cheering for Haiti.

They stunned the crowd with an early goal to take a 1-0 lead. Morocco answered to tie it 1-1. Then Haiti scored an absolute banger—a goal that brought their supporters to their feet. Strangers embraced. Flags waved. The joy was contagious. For a few magical minutes, nothing else mattered.

Morocco's depth and experience eventually showed as they rallied late to advance to the Round of 32 alongside Brazil from Group C. Haiti's World Cup came to an end, but they left the field having earned the respect of everyone in the stadium.

The knockout stage begins this weekend and runs through next week. Every match is now win or go home. I'm especially looking forward to Brazil vs. Japan, the Netherlands vs. Morocco, and seeing whether the United States can continue its impressive run. From this point forward, every game has the intensity of a championship final.

What I'll remember most wasn't the score.

It was the emotion.

I jumped out of my seat celebrating Haiti's second goal. The woman sitting next to me had tears streaming down her face. I don't know her story, but in that moment I didn't need to.

And when the final whistle blew, something beautiful happened.

There were no taunts. No angry confrontations. No sore winners or bitter losers. I watched Haitian supporters congratulate Moroccan fans. Moroccan fans responded with hugs, smiles, and genuine respect. For a brief moment, nationality took a back seat to our shared love of the game.

Sport, at its very best, reminds us of something we too easily forget: we have far more in common than what divides us.

The scoreboard will eventually be forgotten.

The feeling inside that stadium won't.

Ever forward.

Metric-Financial’s, Jack Grella, handing out a yellow card. He was the hit of our section.

Have a wonderful weekend, everyone.

Ever forward.

With kind regards,

Steve

CLICK HERE TO SUBSCRIBE TO ON MY RADAR - IT’S FREE

You can share this letter on X by clicking here.

You can share this letter on LinkedIn by clicking here.

Subscribe to OMR for free by clicking the photo.

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

75 Valley Stream Parkway, Suite 201,

Malvern, PA 19355

CMG Customer Relationship Summary (Form CRS)

Metric-Financial, LLC Customer Relationship Summary (Form CRS)

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management. Author of Forbes Book: On My Radar, Navigating Stock Market Cycles.

Follow Steve on X @SBlumenthalCMG and LinkedIn.

IMPORTANT DISCLOSURE INFORMATION

This document is prepared by CMG Capital Management Group, Inc. (“CMG”) and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, CMG’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing, and transaction costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. The views expressed herein are solely those of Steve Blumenthal as of the date of this report and are subject to change without notice.

Investing involves risk.

This letter may contain forward-looking statements relating to the objectives, opportunities, and future performance of the various investment markets, indices, and investments. Forward-looking statements may be identified by the use of such words as; “believe,” anticipate,” “planned,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular market, index, investment, or investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, Federal Reserve policy, and other economic, competitive, governmental, regulatory, and technological factors affecting markets, indices, investments, investment strategy and portfolio positioning that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Investors are cautioned not to place undue reliance on any forward-looking statements or examples. All statements made herein speak only as of the date that they were made. Investing is inherently risky and all investing involves the potential risk of loss.

Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CMG), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CMG. Please remember to contact CMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CMG is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice.

No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, has not been independently verified, and does not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. See in links provided citing limitations of hypothetical back-tested information. Past performance cannot predict or guarantee future performance. Not a recommendation to buy or sell. Please talk to your advisor.

Information herein has been obtained from sources believed to be reliable, but we do not warrant its accuracy. This document is general communication and is provided for informational and/or educational purposes only. None of the content should be viewed as a suggestion that you take or refrain from taking any action nor as a recommendation for any specific investment product, strategy, or other such purposes.

In a rising interest rate environment, the value of fixed-income securities generally declines, and conversely, in a falling interest rate environment, the value of fixed-income securities generally increases. High-yield securities may be subject to heightened market, interest rate, or credit risk and should not be purchased solely because of the stated yield. Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment-grade investments are those rated from highest down to BBB- or Baa3.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in Malvern, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy, or exclusively determines any internal strategy employed by CMG. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures. CMG is committed to protecting your personal information. Click here to review CMG’s privacy policies.

See CMG Disclosures at the bottom of this page.

For more information about NDR, please visit at www.ndr.com.

NDR, Inc. (NDR), d.b.a. Ned Davis Research Group (NDRG), any NDRG affiliates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDRG publication. The data and analysis contained herein are provided "as is." NDRG disclaims any and all express or implied warranties, including, but not limited to, any warranties of merchantability, suitability or fitness for a particular purpose or use. NDRG's past recommendations and model results are not a guarantee of future results. This communication reflects our analysts' opinions as of the date of this communication and will not necessarily be updated as views or information change. All opinions expressed herein are subject to change without notice. NDRG or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. For NDRG's important additional disclaimers, refer to www.ndr.com/invest/public/copyright.html. Further distribution prohibited without prior permission. Copyright 2025 © NDR, Inc. All rights reserved.